During the confirmation hearing for the nomination of Representative Marcia Fudge, D-Ohio, to serve as Secretary of the U.S. Department of Housing and Urban Development, she was asked repeatedly about assistance to borrowers, including a Federal Housing Administration mortgage insurance premium cut. While Fudge was noncommittal on the move, cutting the MIP on 30-year loans would do little to help borrowers. Evidence from the last MIP cut in 2015 shows that any benefit from it would accrue to current homeowners or special interest groups that work for real estate commissions.

Pressure for a MIP cut is building from such groups. The National Association of Realtors states that “a reduction in FHA insurance premiums has the potential to decrease monthly mortgage payments for thousands of new low- and moderate-income borrowers,” according to Inside Mortgage Finance. Lenders such as the Community Home Lenders Association are also jumping on the bandwagon.

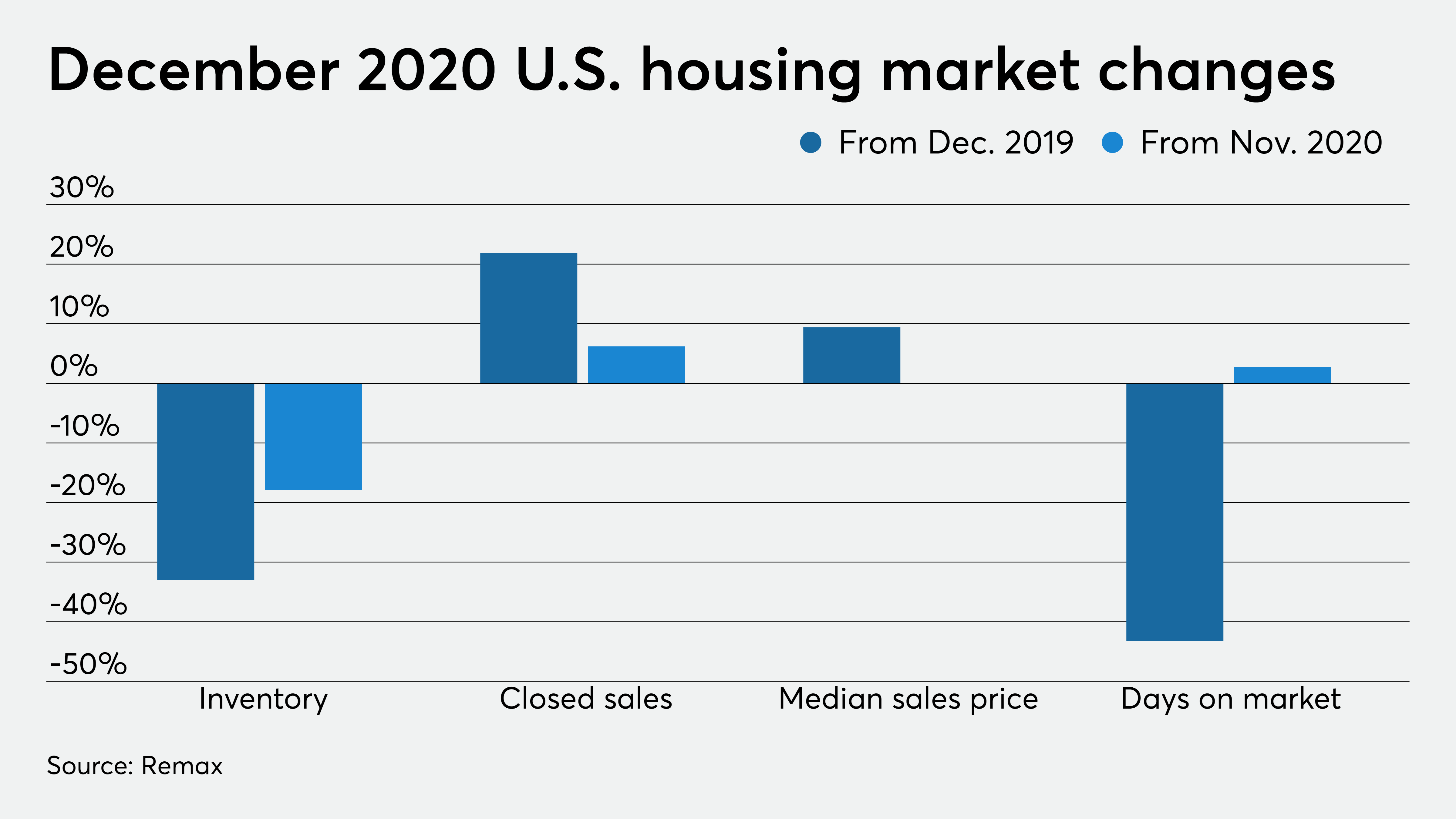

However, HUD needs to consider that since mid-2020, the housing market has been on a tear. Thanks to ultra-low mortgage rates, 2020 purchase originations will likely be 15% higher than in 2019, despite the pandemic-induced drop in activity during April and May. In addition, work from home has unshackled homeowners and renters alike to purchase a home in more affordable cities and states. At the same time, supply has been depleted and at the end of 2020 stands at just around just 2 months — a historic low. Home prices are rising at over 10% due to the increased demand and limited supply.

Given this backdrop, stimulating yet more demand through a premium cut — which works the same way as a mortgage rate cut — would lead to even faster home price appreciation, especially in areas with moderate FHA presence. It would hurt non-FHA borrowers as they would have to pay higher prices and take on greater debt. For FHA borrowers, the financial impact would be a wash as the lower MIP would be absorbed into higher prices. Crucially, it would not open the doors for new homebuyers as supply is still limited. In the end, higher prices would benefit existing homeowners, realtors, and lenders.

This outcome is entirely foreseeable, as AEI Housing Center research shows with respect to the 2015 FHA MIP cut. That 50 bps MIP cut was predicted to lead to 250,000 new first-time buyers over the next three years and save each FHA buyer $900 annually. Instead, we found that home prices rose about 2.5 ppts. faster in FHA neighborhoods and only about 17,000 new first-time buyers were brought into the market — far short of FHA’s prediction. Beneficiaries were existing homeowners, who gained from higher asset prices, and realtors, who received an estimated windfall, which since 2015 totals around $2.4 billion, due to increased commissions from higher prices.

In 2021, months’ supply is about half the level that it was in 2015 and home prices are already rising at twice their rate in 2015. If a MIP cut then did not help low- or moderate-income borrowers buy a home, it certainly won’t help them today.

Of course it is to be expected that special interest groups would again lobby for this cut during the early stages of the Biden presidency, after having struck out with the Trump administration on a similar proposal in 2017. Even though it is true that FHA’s Mortgage Insurance Fund’s capital ratio now stands at 6.1%, which is three times the statutory minimum mandated by Congress, prudent long-term fiscal planning actually requires caution since FHA delinquencies in December stand at 17.4% and serious delinquencies at 11.8%. Once the forbearance program, which is allowing borrowers to temporarily pause mortgage payments, ends, FHA will likely need much of this money to pay claims.

Instead of a straight up premium cut, a far superior solution would be for HUD focus on helping disadvantaged borrowers. This could be done by tying any premium reduction to shorter loan terms, which would reduce defaults and thus require FHA to hold less capital. This approach would not increase buying power during a tight market, thereby mitigating the inflationary price pressure while ensuring more rapid equity buildup.

HUD should withstand the lobbying by realtors and lenders for an MIP cut on 30-year loans, as such a cut would be harmful to entry-level buyers. U.S. housing policy should look out for the interests of low- and moderate-income families, rather than special interest groups.