The mortgage industry is notorious for its use of acronyms and even acronyms inside acronyms (TRID, anyone?). However, there is an acronym that is highly relevant to the current rate environment: ZIRP, which stands for “Zero Interest Rate Policy.” As its definition implies, this term describes the Federal Reserve’ s current policy of holding the Fed funds rate at near 0% for the foreseeable future due to the economic challenges presented by the COVID-19 pandemic.

It may be easy for some to assume a locked-down Fed Funds rate means mortgage rates will remain at the historically ultra-low levels the industry has seen throughout the pandemic. Not only does history tells us this is not the case, but the recent uptick in interest rates due to the rise in the Treasury yield and increased economic spending provides even more current proof that rate swings are possible, if not inevitable during ZIRP. As such, lenders and their capital markets executives must be prepared for interest rate swings in either direction despite the current ZIRP.

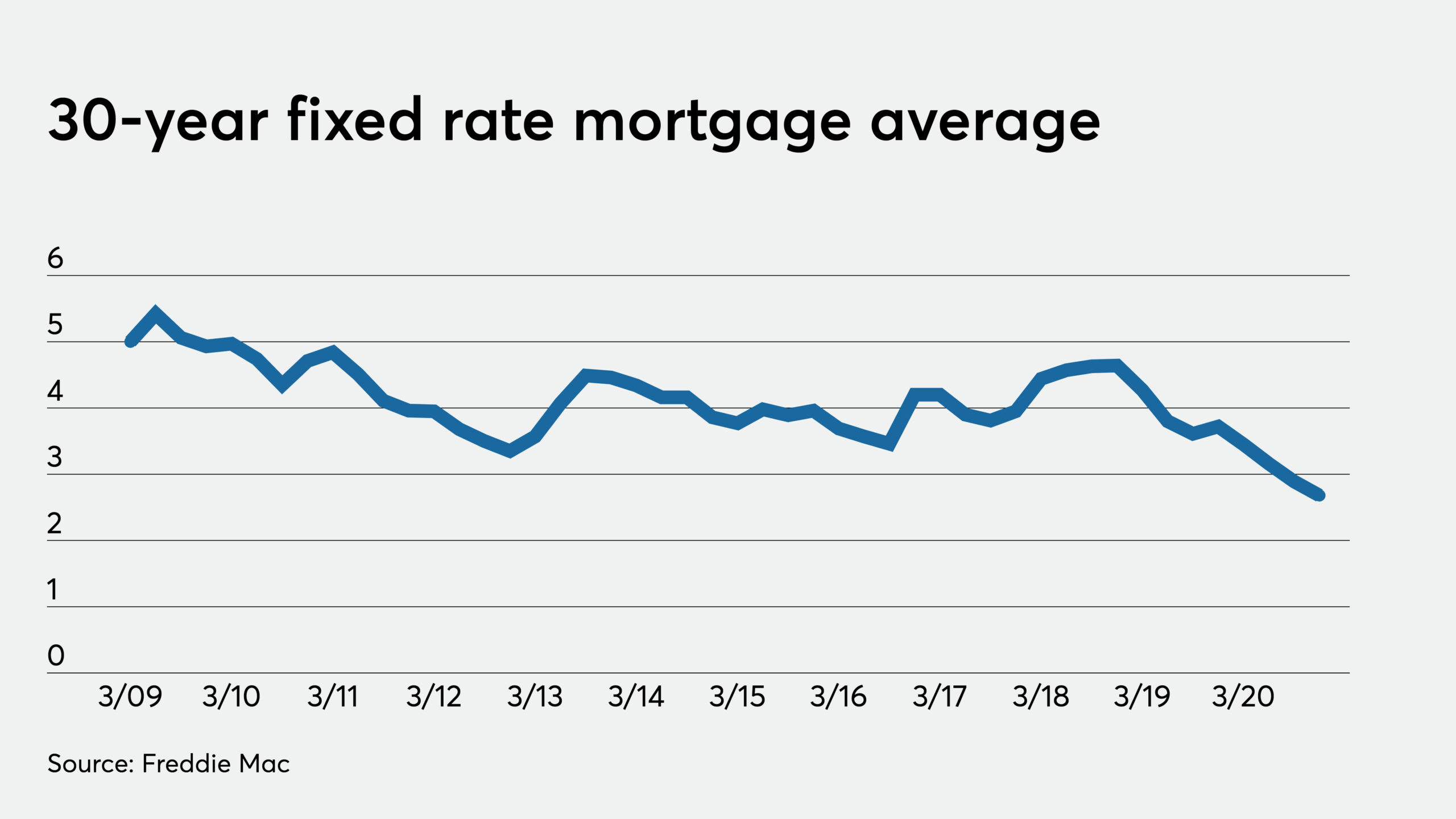

The last time the Fed instituted ZIRP was following the Global Financial Crisis, which lasted for a span of seven years, from December 2008 to December 2015. In December 2008, the average note rate for 30-year mortgages was 5.14%, when ZIRP ended in December 2015 the par note rate was 3.31%. However, that lengthy seven-year span was not a gentle expressway ramp; it was riddled with both bull and bear markets for mortgage rates despite the continued Fed pledge of “lower for longer.” Despite a Federal Open Markets Committee (FOMC) target on short-term rates of 0.00% – 0.25%, mortgage rates experienced several violent swings.

During what was known as the taper tantrum (remember hearing that talk again earlier this month?), the market was afraid the Fed was going to taper off its purchases of Treasuries and mortgage-backed securities so mortgage rates went up over 100 basis points over 3 short months. During another span of only 9 weeks prices on the lowest-coupon mortgage-backed security declined by a whopping 800 basis points, from 101 all the way down to a 93 handle. All of this activity occurred more than two years before the Fed actually instituted the very tiniest bit of liftoff in their Fed funds rate policy.

Looking at the current environment, the Fed has indicated that it will not raise the Fed funds rate until at least 2023. However, as the industry has observed before, this does not mean that mortgage rates are going to languish around the same range they’ve been in for the last 10 months. In fact, it would not be unusual to see changes of even an entire whole percentage point up, or down, for however long this current ZIRP is in place. In fact, Fannie Mae and Freddie Mac have both forecasted moderate increases in interest rates in 2021 in anticipation of this inevitability, though rates could certainly head in the opposite direction given the right market conditions.

In these past few months, I’ve heard people say things like “The market’s not going anywhere for a few years. The Fed said so, and it’s already priced in, right?” While that may be the case for the Interest on Excess Reserves and Fed Funds, which the Fed has pegged at near zero, there will not be an alarm that goes off letting lenders know to lock the doors. Just because the Fed is staying put doesn’t mean that mortgage rates, and prices of MBS, are staying put as well. As history has shown us, shocks can — and do — come when markets least expect them.