While Mr. Cooper had a strong earnings performance in the first quarter, going forward, at least in the near term, will be a little tougher, executives said. The company already joined several competitors in making staff reductions.

Driven primarily by a $552 million mark-to-market on its mortgage servicing rights and a $223 million gain from its servicing technology transaction with Sagent, Dallas-based Mr. Cooper had net income of $658 million. This is up from $155 million in the fourth quarter and $561 million in the first quarter of 2021.

Those results are not likely to continue as the originations side of the business is shrinking because of higher interest rates.

“The next couple of quarters are a transitional environment for us,” Chairman and CEO Jay Bray said on the earnings call. “We expect our returns to trough in the second quarter, after which we’re projecting a sharp ramp in servicing profitability, driven primarily by higher interest rates, which should carry us by fourth quarter back into our target ROTCE range.”

ROTCE stands for return on tangible common equity and it is computed by dividing annualized net earnings by average monthly tangible common shareholders’ equity.

Mr. Cooper’s operating ROTCE for the first quarter was 8.2%, below its target range of 12% to 20%, Bray said.

As a consequence of the tougher originations business, Mr. Cooper will be taking a charge to earnings in the second quarter due to staff reductions. Approximately 250 positions were eliminated in the first quarter, the company said in a response sent following the call.

“Given lower volumes, rationalizing capacity is an unavoidable theme for everyone in origination and we’ve been very disciplined in managing capacity,” Vice Chairman and President Chris Marshall said.

“Having made that point, we’re at the same time continuing to invest in our originations platform. For example, as you heard last quarter we’re making extremely good progress with Project Flash, which further automates our middle office processes and continues to reduce our cost to originate,” Marshall continued.

In addition, the strong net income resulted in Mr. Cooper utilizing $197 million of its deferred tax asset, bringing the balance down to $794 million.

“The DTA is still an important asset to us and to drive sustainable cash flow by limiting our federal tax payments and it will continue to do so for some years to come,” said Jaime Gow, Mr. Cooper’s chief financial officer. “But it is no longer a material component of our equity base, which is a positive for our valuation.”

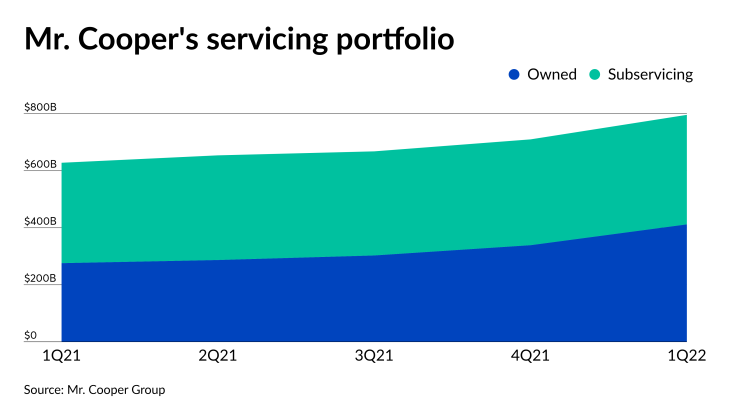

Meanwhile, Mr. Cooper took advantage of the marketplace dynamics to grow its MSR portfolio, to $796 billion total (of which $412 billion are rights it owns), up from $710 billion at year-end 2021 and $629 billion on March 31, 2021.

“I think it was about a year ago that we shared a thesis with you that higher rates will force originators back into the market, selling the MSRs which they had been accumulating since the pandemic started,” Marshall said. “With the sharp rise in rates this year, we saw a deluge of products hitting the market with very attractive pricing.”

The company acquired $81 billion of MSRs in the first quarter as a result.

However, servicing rights sales market conditions are changing and as a result, Mr. Cooper is shifting its capital allocation focus to stock repurchases from MSR buys.

“Prices have exceeded where we thought they’d be at this point,” Marshall said. “And quite frankly, they’re sharply higher from where they were when we did a significant amount of purchases last quarter.”

That shift is likely to have implications for continued MSR growth at Mr. Cooper.

“All in, we expect [Mr. Cooper’s] owned MSR portfolio could decrease slightly, before considering additions of bulk or co-issue MSR,” said BTIG analyst Eric Hagen in a report. “It easily has the liquidity to capitalize the addition of more MSR, the question is how it goes about growing it, and what price it pays for the asset (particularly for bulk transactions which we expect will remain competitively bid).”

Still, Mr. Cooper’s pretax operating income for the servicing unit (which does not take into account that mark-to-market gain) was just $7 million, down from $41 million in the fourth quarter and $37 million one year ago.

As the pandemic-related moratoriums end, Xome’s auction platform is also picking up business, with its inventory of properties for sale adding 11,509 units during the fourth quarter, bringing it to an all-time high of 18,254. That gives Xome the potential to be a major contributor to Mr. Cooper’s earnings, Marshall said.

“After losing a small amount of money for the past two years due to the moratorium, we’re projecting the exchange breaking even in the second quarter,” Marshall said. “And as we exit 2022 and enter 2023, we look for a quarterly EBT run rate that would equate to full year 2023 earnings of $120 million or higher.”

The one caveat to that projection is that servicers have been cautious in moving properties into foreclosure because they are giving consumers every opportunity to enter into a modification agreement.

On the originations’ side, Mr. Cooper produced $11.6 billion in the first quarter, down from $17.2 billion in the fourth quarter and $25.1 billion for the first quarter of 2021.

The big reason for the quarter-to-quarter drop was a 54% drop in its correspondent purchase activity, to $3.8 billion from $8.2 billion in the fourth quarter.

Right now, there is extreme pricing pressure in the correspondent channel and Mr. Cooper is going to wait until margins improve before ramping activity back up, Marshall said.

Pretax operating income for the originations segment fell to $157 million in the first quarter, versus $182 million three months prior and $362 million one year ago.

However, Mr. Cooper’s margins increased on a quarter-to-quarter basis to 153 basis points from 141 bps. For the first quarter of 2021, the margin was 163 bps.