Mortgage rates continued to slide this week, moving in an opposite direction from the benchmark 10-year Treasury, which rose as much as 15 basis points during the past seven days, Freddie Mac reported.

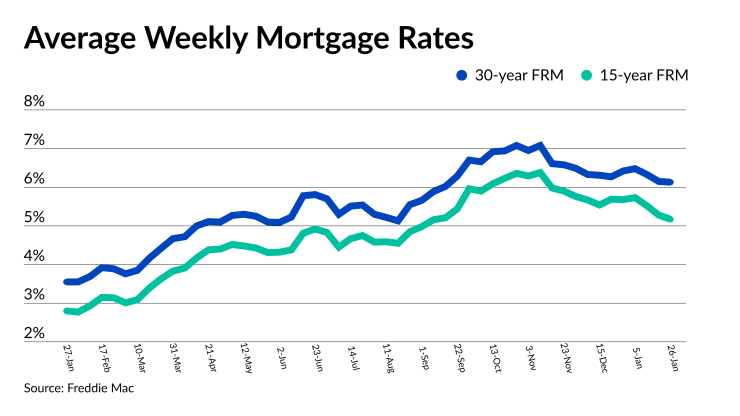

Its Primary Mortgage Market Survey for the week of Jan. 26 found the average for the 30-year fixed rate loan fell by 2 basis points to 6.13% compared with the prior period and 35 basis points from the first week of 2023. For the same week last year, the 30-year FRM was at 3.55%.

The drop in the 15-year FRM was even larger, down 11 basis points to 5.17% from 5.28% for the week of Jan. 19. A year ago, this rate was at 2.8%.

Freddie Mac changed its methodology and now uses applications submitted to Loan Product Advisor to determine its results rather than a lender survey.

Zillow, whose tracker is based on offers made through its mortgage marketplace, reported both of those rates increased 3 basis points as of Thursday morning from the prior week, to 5.9% and 4.93% respectively.

Part of the variation can be explained by the larger-than-normal spread between the 30-year FRM and the 10-year Treasury. Typically the difference between the two is 250 basis points. The 10-year Treasury opened at 3.49% on Thursday morning, a gap of 264 basis points compared with the Freddie Mac survey and 240 basis points from the Zillow tracker.

Zillow’s increase is a result of the market looking ahead to next week’s updates on monetary policy and the labor market, Orphe Divounguy, senior macroeconomist at Zillow Home Loans said in a statement issued Wednesday night.

“The end of China’s zero-COVID policy, lower inflation in Europe and in the U.S., and evidence of enduring labor market strength all suggest that the risk of a recession may be waning.”

That changed perception regarding a recession limits how far mortgage rates could fall, Divounguy continued. But the economic outlook remains cloudy.

“Indeed, data released this week from the Conference Board and the S&P Global Flash US PMI Composite Output Index suggest that a recession is still very much a possibility,” Divounguy said. “Investors will be keeping a close eye on the [personal consumption expenditures] price index, the January jobs report, and the Fed — as the FOMC meets next week — for more clarity on the state of the economy and the central bank’s plans.”

Home purchase demand is thawing as a result of lower mortgage rates, said Sam Khater, Freddie Mac chief economist in the press release. “Potential homebuyers remain sensitive to changes in mortgage rates, but ample demand remains, fueled by first-time home buyers.”

New home sales rose for the third consecutive month, which was attributed to falling rates, the federal government reported on Thursday morning. However, this report is not adjusted for canceled contracts.

“Lower mortgage rates, builder incentives, and a lack of existing-home inventory might make new homes attractive enough to entice more buyers,” First American Deputy Chief Economist Odeta Kushi said in a commentary on the new home sales report. “The latest uptick in builder confidence is a sign that builders believe lower mortgage rates may lift demand.”

On Wednesday, the Mortgage Bankers Association’s Weekly Application Survey revealed that activity increased for the third consecutive week.

“Borrower demand, thanks to lower mortgage rates, continues to rise in early 2023,” Bob Broeksmit, the MBA’s president and CEO said in a Thursday morning statement. “Purchase demand is still below year-ago levels, but lower rates and improving affordability are favorable developments for the housing market heading into the spring.”