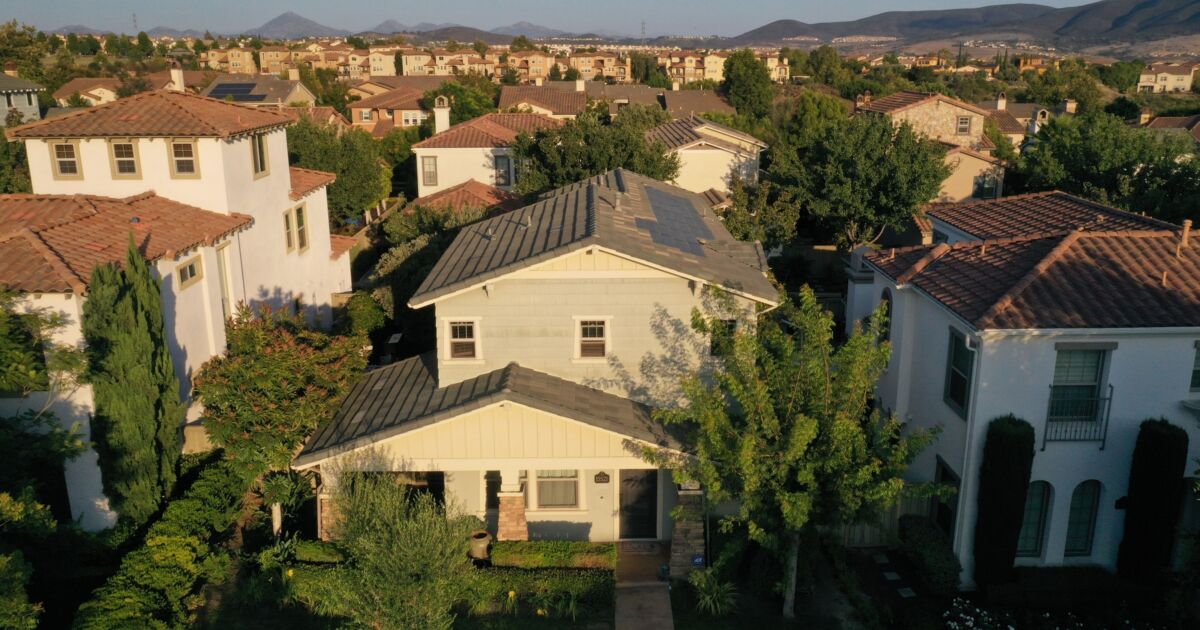

While the surge in home prices has slowed substantially from the heights of last year, home buyers’ affordability concerns are not abating.

Single-family home values increased 8.2% on an annual basis in November, according to the latest price index from the Federal Housing Finance Agency. Although the pace of rising prices was still running above the compound annual growth rate of 7.5% reported by the FHFA since January 2012, it slowed from October’s 9.8% jump and came in considerably lower than the 17.8% surge in November last year.

On a month-over-month basis, though, housing costs have remained flat, and in November, they slipped downward nationwide by 0.1% compared to October.

“U.S. house prices were largely unchanged in the last four months and remained near the peak levels reached over the summer of 2022,” said Nataliya Polkovnichenko, supervisory economist in FHFA’s division of research and statistics, in a press release.

Prices increased in all regions compared to a year ago. The increases ranged from 2.4% in the U.S. Census Bureau’s Pacific division to 12% in the South Atlantic region, with the former consisting of three West Coast states, Hawaii and Alaska, and the latter stretching from Maryland to Florida.

But between October and November, the Pacific division saw the largest falloff in price (1.1%), with the Mountain region coming in 0.8% lower. In contrast, prices grew on a monthly basis in some other regions. They rose by 0.5% in the West North Central division and 0.3% in the West South Central, East North Central and Middle Atlantic regions.

The latest FHFA numbers reflect similar trends reported this week in the S&P CoreLogic Case-Shiller price index, although the year-over-year gain in November came in slightly lower, while monthly decreases were steeper. The Case-Shiller report found housing prices that month down by 2.5% from an early summer peak.

While wide agreement exists that home prices softened in the latter half of the year, perceptions regarding affordability haven’t increased correspondingly. Much of current buyer sentiment can be laid on higher mortgage rates, which had the effect of pushing payments higher and dampening homeowner interest in selling.

“While higher mortgage rates have suppressed demand, low inventories of homes for sale have helped maintain relatively flat house prices,” Polkovnichenko said.

The sluggishness and lack of availability has been noticed by buyers, based on recent survey research from the National Association of Realtors.

Between third and fourth quarters last year, expectations that the home search would become easier fell from 37% to 24%. At the same time, a record high 87% of respondents in NAR’s survey reported they could afford less than half the homes in their markets, rising from 69% three months earlier, even though mortgage rates consistently headed downward in November and December. NAR’s research was conducted in mid December, weeks after interest rates had hit fourth-quarter peaks.

In another housing report, researchers from First American found affordability, or home buying power, plummeted 60% year over year in November. The title and closing services provider’s Real House Price Index factors in mortgage rates and household income changes to determine consumer buying power in the residential real-estate market. Even though income increased from November 2021, “it was not enough to offset the affordability loss from higher mortgage rates and still-strong nominal house price growth,” according to First American Chief Economist Mark Fleming.

Similar to FHFA’s findings, no states reported a decrease in annual “real” home prices.

But “real estate dynamics are local,” Fleming said, noting that cities where costs leaped considerably in the pandemic years of 2020 and 2021, such as San Francisco and Phoenix, are now among the markets seeing prices fall rapidly. First American deemed such cities “overvalued,” with median existing-home sale prices exceeding house-buying power.

“There are exceptions to this relationship, but generally it seems that the most overvalued markets are correcting the fastest,” he said.