Permanent mortgage rate buydowns are the tool of choice for most homebuyers to combat unaffordability, with relatively few turning to the temporary offerings that are now in vogue, Black Knight said.

In the third week of January, 57% of home buyers that locked in that week paid at least 0.5 points or more to reduce their mortgage rate; a mere 3% used a temporary buydown program, Black Knight’s latest Mortgage Monitor reported.

Of those that took a permanent buydown, 44% paid a full point and nearly one-quarter paid two or more points.

Purchases made up 81% of rate locks during that week with an average payment for a rate lock buydown of 1.16 points. At the same time, cash-out refinance borrowers paid an average of 2.06 points.

“If that seems high, consider that back in September and October of last year, as many as 71% borrowers paid points with 43% paying two or more points,” said Ben Graboske, Black Knight data & analytics president in a press release. “Prior to the pandemic-era housing boom, borrowers in 2018-2020 paid 0.5 points with a corresponding cost of around $1,500 — as compared to $4,300 today and as high as $6,900 last fall.”

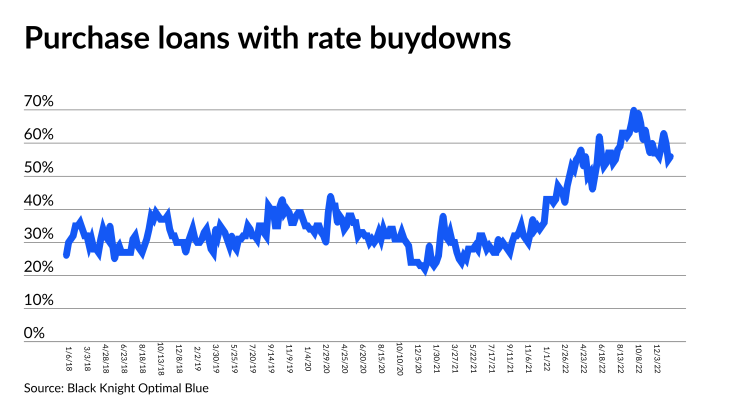

The uptick in the use of permanent buydowns mirrors activity in 2018 and 2019, another time when affordability was challenged, but that was a blip compared with their use today, said Andy Walden, Black Knight’s vice president of enterprise research.

“The simple reason is the magnitude of the impact of rising home prices and interest rates in 2022, which pushed affordability to a more than 35-year low,” Walden said. “Permanent buydown activity has eased modestly alongside rates and home prices in recent months but remains a popular option in today’s market.”

While temporary buydowns have been used in the past, recently they were all but nonexistent until the second half of last year, Walden added.

As mortgage rates topped 7% in November, more lenders publicized temporary buydown offerings to bring in customers, including United Wholesale Mortgage and Rocket, or other programs that lowered interest rates for a short period of time, such as Newfi’s graduated payment non-qualified mortgage product.

More recently, UWM brought out a promotion that allows the mortgage broker at its discretion to drop the interest rate by up to 40 basis points on an individual loan. The broker has the capability to use that tool up to a total of 125 basis points across their entire UWM pipeline.

“Such products may offer an opportunity for prospective homebuyers to temporarily sidestep today’s affordability challenges for those who anticipate increased incomes and/or easing of rates in the future, in any case,” Walden explained.

Analysts at Bank of America Securities also looked at the Black Knight Optimal Blue lock data and found that on Jan. 31, a wide range existed for the rate borrowers received, ranging from a low of 4.5% to a high of 7.75%, with a median of 6%. That is slightly below the latest Freddie Mac Primary Mortgage Market Survey 30-year fixed rate average of 6.09%.

“We continue to believe peak mortgage rates are behind us and survey rate will drop to at least 5.25% by year-end 2023; risk is drop occurs sooner and deeper, down to 4.5%-5.0% range, in 2023,” the B of A Securities report by Chris Flanagan and Henry Navarrete Brooks said.

That means affordability for those getting a rate below 6% is better than the National Association of Realtors index.

“Borrowers with a combination of higher than median income and lower than median rate are doubly advantaged relative to the broad affordability metric, making them more likely to transact than the median borrower,” Flanagan and Brooks said. “Key takeaway: due to distribution effects on mortgage rates, income, and wealth, housing activity has potential to surprise to the upside.”

They currently predict 0% home price appreciation for 2023, but with mortgage rates falling, the risk to that outlook is to the upside.

While the 10-year Treasury initially dropped in reaction to the 25 basis point increase in the Fed Funds rate, the yields have risen back above 3.6% as of Monday morning due to the stronger-than-expected jobs report.

Zillow’s rate tracker put the 30-year fixed at 5.99% as of Monday morning, up 5 basis points from Friday and 29 basis points from Thursday morning.

Purchase rate lock activity increased 64% in the fourth week of January from the first week, Graboske pointed out. “On the surface, it may seem the market has been stirred by a full point decline in interest rates and home prices coming off their peaks — but it’s not that simple.”

Home prices are down 5.3% from their June 2022 peak.

“But affordability still has a stranglehold on much of the market, with the monthly mortgage payment on the average-priced home more than 40% higher than it was this time last year,” said Graboske. “While up, purchase locks were still running roughly 13% below pre-pandemic levels for the last full week of the month.”