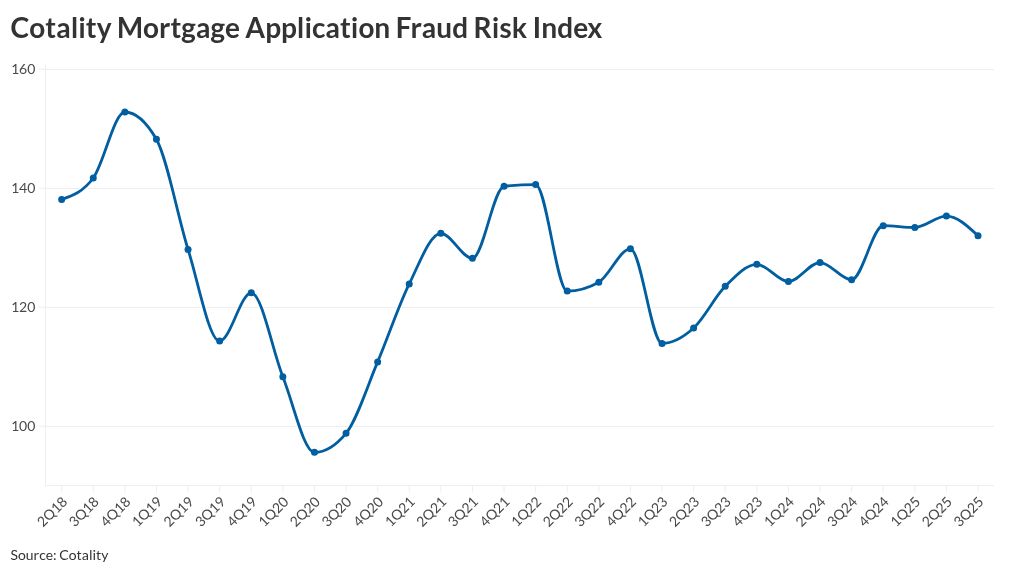

Mortgage application fraud risk increased on an annual basis during the third quarter as one in every 118 applications had indicators of potential misstatements, according to Cotality.

When compared with the third quarter of 2024, fraud risk increased by 8.2% but this dropped by 2.7% from the previous quarter, the National Mortgage Application Fraud Risk Index reported.

This quarter-to-quarter decline came as application volume increased by 8%. Purchases made up two-thirds of the third quarter’s total volume. Government-guaranteed products had a 25% share.

Why application fraud risk increased

The index measures six areas but only one category, undisclosed real estate fraud, was higher versus the previous year.

This category, up 9.1% from a year ago, includes undisclosed debt, possible occupancy misrepresentation, and/or derogatory credit events like foreclosure, notice of default, a short sale and other similar happenings being hidden from the lender.

Another report, this one from Transunion, found that credit washing and synthetic identity creation is a growing problem across all asset types.

Occupancy misrepresentation has been in the headlines because of actions taken by the federal government in recent months.

The growth in non-owner occupied properties is a contributing factor to the large rise in this fraud category, Cotality said.

“As the percentage of investors grows, more borrowers have multiple properties and mortgages,” said Matt Seguin, senior principal, Cotality Fraud Solutions, in a press release. Some of these are people who originally occupied the property, looked to sell but were unable to get their price so they kept it and became a landlord, the report noted.

“Oftentimes, those mortgages are being refinanced simultaneously, and they may be with different lenders,” and he surmised this is why a continuing uptick in this category is taking place.

For the third quarter, Cotality estimated one in 45 investment property applications and one in 26 multi-family applications have indications of fraud risk.

What underwriters need to be on the lookout for

Cotality is noticing increased alerts on occupancy risk. Those include the owner claiming they are occupying the property when a rental listing was found on the property or a primary residence that has a different tax mailing address.

Other areas of increasing risk trends include income and identity, Cotality said.

The buyer has a high income compared to the value of the property being purchased, which could be an indicator of inflated assets or misrepresentation of occupancy.

Meanwhile, indicative of the growth of synthetic identity fraud is more alerts regarding the use of a deceased borrower’s Social Security number or other names associated with a number provided.

Declining property value related alerts grew 42% from the second quarter and 400% year-over-year.

“For lenders, this is a critical signal,” Cotality warned in the report, saying in underwriting, they must take extra care to review appraisals and supporting documentation. “Exercise caution in areas experiencing negative home price growth to ensure sound lending decisions and mitigate risk.”