Millennial mortgage activity remained vigorous as summer came to a close, according to Ellie Mae.

Mortgage applicants between 21 and 40 locked in an average 30-year interest rate of 3.105% — a number that continues to descend to new Millennial Tracker record lows. The rate fell from 3.256% in July and 4.059% in August 2019.

“Given the historically low interest rates, lenders are handling more loans now than they ever have before,” Joe Tyrrell, president of ICE Mortgage Technology, said in a press release.

With the volume surge, the time to close increased to 47 days, up two from July and five from August 2019.

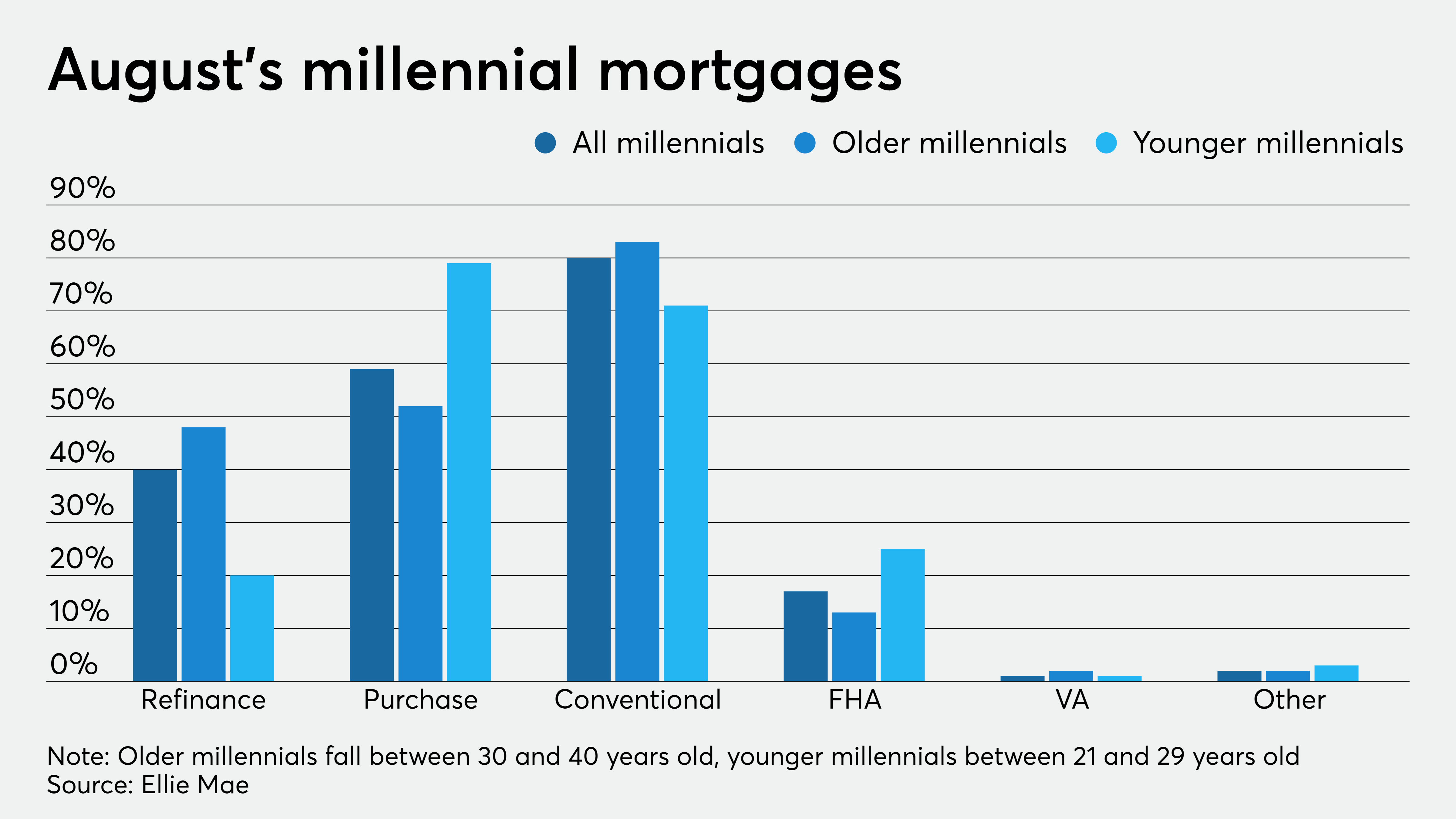

Purchase loans accounted for the lion’s share of originations, though that percentage dwindled to 59% from 61% in July and it marked a steep decline from 74% year-over-year. Refinancing made up about 40% of August’s millennial loans, inching up from 38% the month prior and jumping significantly from 25% the year earlier.

The average millennial FICO score held at 739 for the third month in a row while shooting up from 728 year-over-year as lenders tightened credit availability to a six-year low. Credit scores for approved loans will likely remain high during coronavirus-related economic unease.

The average age for millennial borrowers edged up to 31.8 years from 31.7 years in July and jumped from 30.5 years in August 2019.

The shares of conventional, Federal Housing Administration and U.S. Department of Veterans Affairs loans stayed static month-over-month at shares 80%, 17% and 1%, respectively. Other unspecified types of financing represented the remaining 2%.

Married individuals accounted for a 60% majority of loans closed compared to 59% in July and 55% the year before. Overall, about 57% of primary borrowers were male, 30% female with 13% didn’t specify. The average loan amount rose again to $213,841, climbing monthly from $211,264 and yearly $203,467.

The dynamics change when the data splits between older borrowers (between 30 and 40 years old) and younger borrowers (between 21 and 29 years old) millennials.

The elder group’s August purchase share made up 52% compared to 79% for the younger group. By loan type, conventional mortgages made up an 83% share for older millennials versus 71% for younger, while FHA loans accounted for 13% and 25%, respectively. Average FICO scores for older millennials increased to 748 while the younger set, with less time for credit accumulation, hit 727.