If you’ve been paying attention, you may have noticed that mortgage rates have quietly crept back up to nearly 7%.

While it appeared that those 7% mortgage rates were a thing of the past, they seemed to return just as quickly as they disappeared.

For reference, the 30-year fixed averaged around 8% a year ago, before beginning its descent to nearly 6% in early September.

It appeared we were destined for 5% rates again, then the Fed rate cut happened. While the Fed itself didn’t “do anything,” their pivot coincided with some positive economic reports.

Combined with a “sell the news” event of the Fed cut itself, rates skyrocketed. However, now might be a good time to remind you that rates do tend to fall for a while after rate cuts begin.

Falling Rates Often Play Out Over Years, Not Months

As noted, the Fed pivoted, aka lowered its own fed funds rate, in September. They did so after increasing their rate 11 times during a period of tightening.

Hence the word “pivot,” as they switch from raising rates to lowering rates.

In short, the Fed determined monetary policy was sufficiently restrictive, and it was time to loosen things up. This tends to result in lower borrowing rates over time.

While many falsely assumed the pivot would lead to even lower mortgage rates overnight, those “in the know” knew those cuts were mostly already baked in, at least for now.

So when the Fed cut, mortgage rates actually drifted a little higher, though not by much. The real move higher post-cut came after a better-than-expected jobs report.

Lately, unemployment has taken center stage, and a strong labor report tends to point to a resilient economy, which in turn increases bond yields.

And since mortgage rates track the 10-year bond yield really well, we saw the 30-year fixed jump higher.

After nearly hitting the high-5s in early September, it completely reversed course and is now knocking on the 7% door again.

How is this possible? I thought the high rates were behind us. Well, as I wrote earlier this month, mortgage rates don’t move in a straight line up or down.

They can fall while they are rising, and climb when they are falling. For example, there were times when they moved down an entire percentage point during their ascent in 2022.

So why is it now surprising that they wouldn’t do the same thing when falling? It shouldn’t be if you zoom out a little, but most can’t stay the course and contain their emotions from dramatic moves like this.

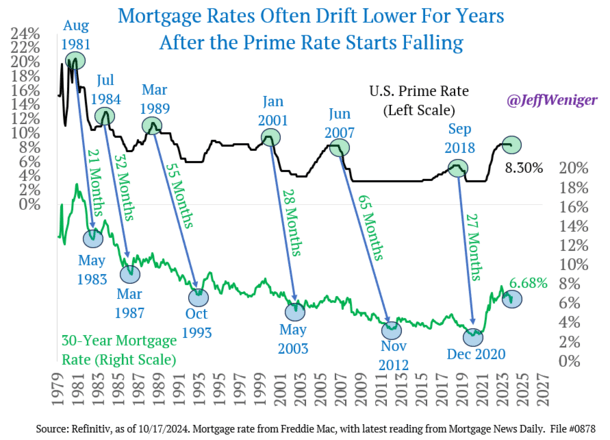

It Can Take Three Years for Mortgage Rates to Move Lower After a Fed Pivot

WisdomTree Head of Equities Jeff Weniger crafted a really interesting chart recently that looked at how long mortgage rates tend to fall after the prime rate starts falling.

He graphed six instances when rates came down from 1981 through 2020 after prime was lowered. And each time, other than in 1981, it took at least two years for rates to hit their cycle bottom.

If we combine all those falling mortgage rate periods and use the average, it took 38 months for them to move from peak to trough.

In other words, more than three years for rates to hit their lowest point after an initial Fed cut.

As it stands now, we are only a month into the prime rate falling. But it’s important to note that rates had already fallen from around 8% a year ago.

They’ve now drifted back up to around 6.875%, and it’s unclear if they’ll continue to move higher before coming down again.

But the takeaway for me, in agreeing with Weniger, is that we remain in a falling rate environment.

Even if 30-year fixed rates hit 7% again, it’s lower highs over time as rates continue to descend.

Meaning we saw 8% in October, 7.5% in April, and perhaps we’ll see 7% this month. But that’s still a .50% lower rate each time.

The next stop could be 6.5% again, then 6%, then 5.5%. However, it won’t be a straight line down.

Still, it’s important to pay attention to the longer-term trend, instead of getting caught up in the day-to-day movement.

Mortgage Lenders Take Their Time Lowering Rates!

I’ve said this before and I’ll say it again for the umpteenth time.

Mortgage lenders will always take their sweet time lowering rates, but won’t hesitate at all when raising them.

From their perspective, it makes perfect sense. Why would they stick their neck out unnecessarily? Might as well slow play the lower rates if they’re not sure where they’ll go next.

As a lender, if you’re at all fearful rates will get worse, it’s best to price it in ahead of time to avoid getting caught out.

That’s likely what is happening now. Lenders are being defensive as usual and raising their rates in an uncertain economic environment.

If and when they see softer economic data and/or higher unemployment numbers, they’ll begin lowering rates again.

But they’ll never be in any rush to do so. Conversely, even a single positive economic report, such as the jobs report that got us into this situation, will be enough for them to raise rates.

In other words, we might need multiple soft economic reports to see mortgage rates move meaningfully lower, but just one for them to bounce higher.

So if you’re waiting for lower mortgage rates, be patient. They’ll likely come, just not as quickly as you’d expect.