Rocket Cos. reported a $481 million net loss in the third quarter, driven by a massive decline in the valuation of mortgage servicing rights.

The stark figure comes after profits of $178 million and $114.9 million in the recent second quarter and third quarter of last year, respectively. The third quarter loss comes while Rocket reports positive momentum in adjusted earnings, and its highest mortgage origination volume since the first quarter of 2022, according to executives.

Rocket’s adjusted net income of $166 million was an improvement from the $121 million mark in the second quarter, and just $7 million in the year ago period.

Company CEO Varun Krishna, opening the earnings call with a lengthy description of Rocket’s technological advantages, said he wanted to emphasize “optimism.”

“It’s always important to take the long view and put things in perspective,” he said in regard to housing market conditions.

Driving the top-line loss was an $878.3 million loss in the change of fair value of MSRs, wiping out $373.8 million in servicing income. In the second quarter, servicing income was $241.7 million, against a $112.9 million MSR valuation dip; in the year ago period, Rocket reported $356.8 million servicing income against a $12.8 million MSR valuation gain.

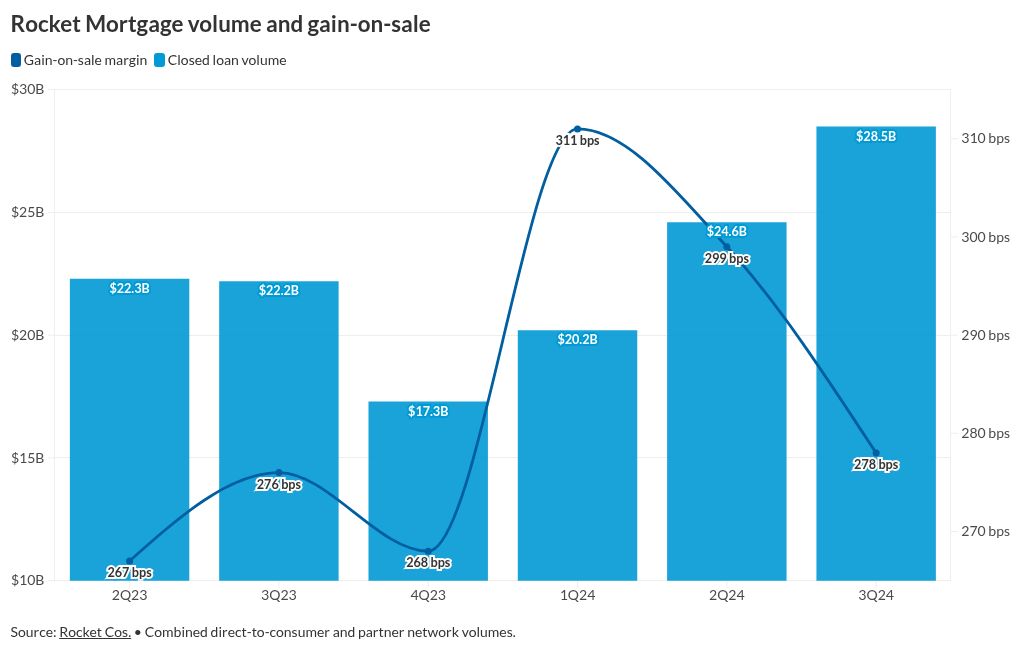

The Detroit giant recorded $28.5 billion in origination volume in the third quarter, increases of 15% and 28% from the quarter and year ago period. Production volume grew sequentially in Rocket’s direct-to-consumer channel and partner network, with an overall gain on sale margin of 278 basis points.

That overall GOS margin fell from the second quarter’s 299 basis points. The direct-to-consumer and partner network’s gain on sales of 410 basis points and 147 basis points, respectively, slipped quarterly but were up annually.

Rocket also claims its the largest originator of closed-end second liens in the nation, as its home equity volume grew 78% year-over-year.

Chief Financial Officer Brian Brown, in recapping the company’s financial performance, emphasized the company’s gains in purchase and refinance market share. Rocket over the summer also acquired MSR portfolios totalling $311 million, adding $22.4 billion in unpaid principal balance to its massive portfolio.

“Today, we have the capacity to support $150 billion in origination volume without adding a single dollar of fixed costs,” said Brown.

Through October, Rocket this year has acquired or committed to add over $70 billion in unpaid principal balance, or 220,000 new clients. The company claims an 85% recapture rate.

The lender and servicer reported GAAP revenue of $647 million in the quarter, around half of its revenues in the second quarter and prior third quarter. Following adjusted revenue of $1.3 billion in the third quarter, Rocket is projecting between $1.05 billion and $1.2 billion for the fourth quarter.

Krishna attributed the lower fourth quarter projection on the slower winter housing market and elevated interest rates. He also told analysts the guidance was 27% greater than the same time last year. Brown said the company expects a slight GOS margin improvement to end the year.

“There’s a little bit of conservatism built in there, and that’s just typically because we see some competitors do some pricing plays around the holidays,” he said.

The company said its recent Welcome Home Rate Break promotion led to a 21% increase in usage of its affordable product suite. Consumer interactions with the firm’s consumer-facing generative chat more than doubled quarterly. Its Logic Synopsis tool for analyzing customer calls was also supporting 1 million calls weekly at the end of October.

Rocket remains well insulated against any market turmoil, with $8.3 billion in liquidity. Fitch Ratings this month also upgraded Rocket to BBB-, and executives claim their firm is the first nonbank to achieve an investment grade rating from one of the three major ratings agencies in two decades.