Mortgage application activity picked up for the third week in a row, driven in part by a pullback in interest rates, according to the industry’s largest trade group.

The Mortgage Bankers Association’s Market Composite Index, a measure of weekly application activity based on surveys of its members, jumped a seasonally adjusted 6.3% for the seven days ending Nov. 22. The latest increase comes off a 1.7% rise in the previous survey. Compared against the same period in 2023 when Thanksgiving arrived a week earlier, application volumes surged 18.1%.

“Purchase activity drove overall applications higher last week, as conventional purchase applications picked up pace, and mortgage rates declined for the first time in over two months,” said Joel Kan, MBA vice president and deputy chief economist, in a press release.

The conforming 30-year fixed-mortgage rate slipped down 4 basis points from the previous week among MBA lenders to an average of 6.86% from 6.9%. Points used to buy down the rate remained unchanged at 0.7.

Averages for the other most commonly used rate types saw similar downward movement. The 30-year contract jumbo rate averaged 6.97%, decreasing from 7.03% a week earlier. Borrowers used 0.73 points on average, rising from 0.63.

The average 30-year rate for loans backed by the Federal Housing Administration fell 7 basis points to 6.61% from 6.68% week over week. Borrower points increased to 0.99 from 0.9.

Rate movements led the seasonally adjusted Purchase Index to accelerate 12.4% from seven days earlier, maintaining momentum after a 2% increase in the previous survey.

“With the growth in for-sale inventory and signs that the economy remains strong, buyers have remained in the market even though rates have increased recently,” Kan said.

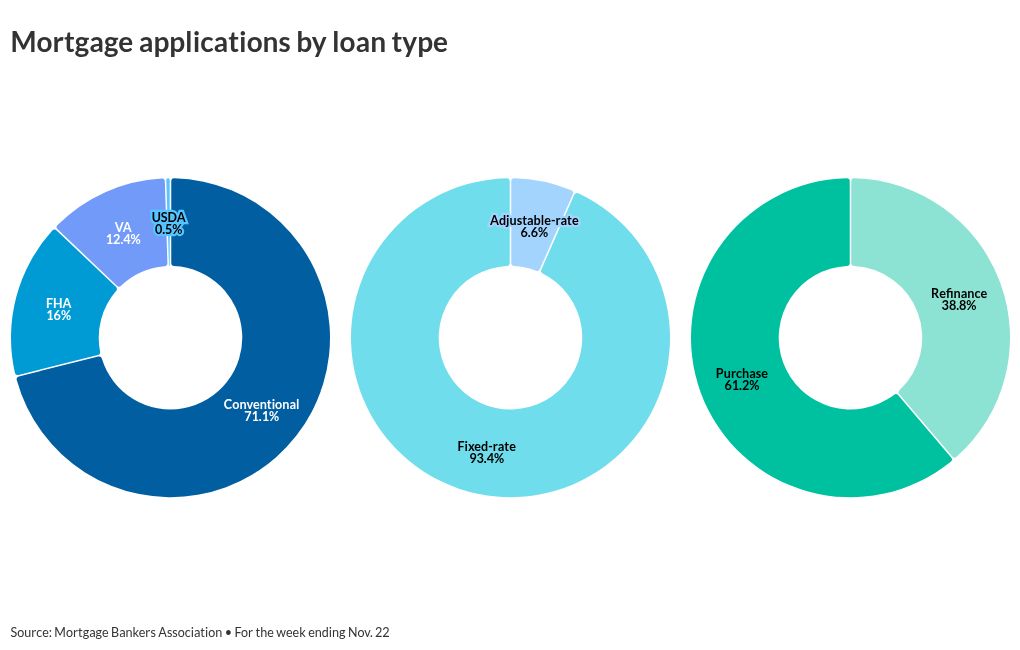

The Refinance Index, on the other hand, pulled back 2.6% following the previous week’s 1.8% uptick. The share of refinances relative to total volume shrank to 38.8% from 41%.

The encouraging signs overall for lenders last week came even as economic researchers, including experts from Fannie Mae and the MBA, lowered their forecasts for both full-year 2024 and 2025. Economists cited the likelihood of mortgage rates remaining higher than previously anticipated for tempered growth over the next several months.

MBA predicted 2024 dollar volume to finish at $1.78 trillion, after forecasting a total of $1.79 trillion in October. The dropoff comes from fewer refinances, as the purchase outlook was left unchanged.

For 2025, MBA sees both purchases and refinances dropping to a combined $2.14 trillion, down from the previous month’s prediction of $2.3 trillion.

In the weekly data, though, numbers still pointed to robust demand among buyers, across price levels. “The increase in conventional purchase applications helped push the average purchase loan size to $439,200, its highest level in almost a month,” Kan said.

Higher purchase activity also led the seasonally adjusted Government Index to squeeze out an 0.1% weekly increase. A 9.8% spike in federally backed purchases was largely offset by a fall in refinances.

The share of government-sponsored activity shrank, though, with new FHA applications accounting for 16%, compared to 16.6% one week prior. The share of applications guaranteed by the Department of Veterans Affairs represented 12.4%, down from 13.6%. Mortgages backed by the U.S. Department of Agriculture grew to 0.5 of activity from 0.4% week over week.

Meanwhile, adjustable-rate mortgage volume, which historically rises and falls in the same direction as fixed rates, bucked usual trends. The ARM share grew to 6.6% from 5.9% the previous week.