For the second time in three weeks, mortgage rates moved lower, but given rates are in the same range for the past month shows investors are uncertain about the U.S. economy under President-elect Trump, Freddie Mac said.

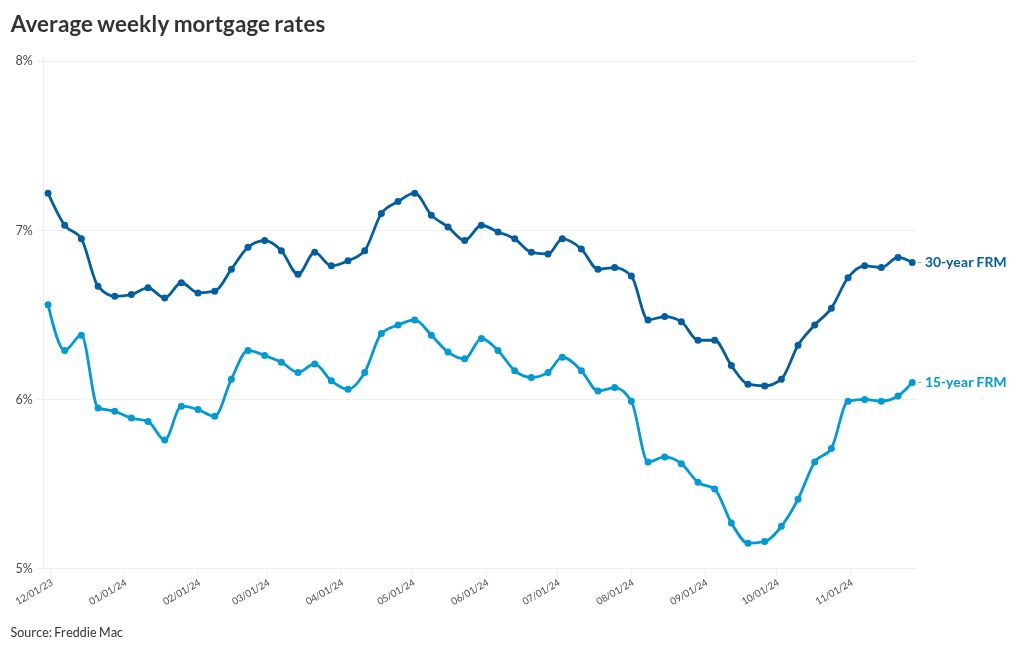

The 30-year fixed rate mortgage was at 6.81% as of Nov. 27, down from 6.84% one-week prior, the Primary Mortgage Market Survey reported. This week’s results include an adjustment for the upcoming Thanksgiving holiday.

For the same week in 2023, the 30-year FRM was 7.22%.

“Rates have been relatively flat over the last few weeks as the market waits for more clarity on specific economic policies,” Sam Khater, Freddie Mac’s chief economist, said in a press release.

The 30-year FRM is only two basis points higher than where it was for the first week of November, the Freddie Mac data shows.

“Potential homebuyers are also waiting on the sidelines, causing demand to be lackluster,” Khater said. “Despite the low sales activity, inventory has only modestly improved and remains dramatically undersupplied.”

Khater’s comment came even as the pending home sales report released Wednesday morning found they had increased due to the brief rate dip in September, which enticed buyers into the market in October.

Meanwhile, the 15-year FRM as tracked by Freddie Mac increased 8 basis points week-to-week to 6.1% from 6.02%. For the same time last year, it was at 6.56%.

Zillow’s rate tracker showed a significant decline from one week ago, with the 30-year FRM down to 6.45% as of 11 a.m. on Nov. 27. That was 17 basis points from the previous week’s average of 6.62%.

The 10-year Treasury yield at that same time was at 4.25%, down from 4.3% at the close on Nov. 26 and from 4.43% at the end of trading last Thursday.

This decline in the 10-year followed the Personal Consumption Expenditures index release on Wednesday morning. The Federal Reserve’s preferred measure of inflation increased 0.2% in November versus October.

On a year-over-year basis, the increase was 2.3%, compared with 2.1% in October.

Separately, the Freddie Mac economics team headed by Khater updated its outlook on Nov. 26, although it noted it was not adjusted to reflect the results of the presidential election.

Freddie Mac expects a moderation in economic growth next year, with a cooling of the labor market and less consumer spending. That would keep the Federal Open Market Committee on its course of rate cuts in upcoming meetings.

However, First American Financial Chief Economist Mark Fleming pointed to recent comments by Federal Reserve Chairman Jay Powell that the central bank is not in a rush to lower rates.

That has left investors split on whether the FOMC will cut rates by 25 basis points at its December meeting, “and calling into question the pace and extent of rate cuts in 2025,” Fleming said in his commentary accompanying the First American Data & Analytics Real House Price Index. “More importantly, recent history suggests that the yield on the 10-year Treasury bond is less sensitive to changes in the Fed Funds rate and more responsive to the longer-term outlook.”

The Freddie Mac posting noted mortgage rates have shifted upwards since the dip in October.

“In the near-term, rates may continue to be volatile and higher rates will keep home sales muted for the remainder of this year,” Freddie Mac said. “But as we get into 2025, we anticipate that rates will gradually decline throughout the year.”

While Fannie Mae’s November forecast also called for lower rates, it no longer expects them to slip below the 6% mark on average not just for next year, but for 2026 as well.

Fleming, too, is bearish on mortgage rate movements for the rest of 2024 and into next year, saying they are unlikely to decline in a meaningful amount “unless the Fed throws a curveball, such as cutting rates even more than expected, which would likely signal recession risk has risen significantly.”

Freddie Mac no longer provides forward looking guidance on origination volume. It noted in the second quarter it calculated $429 billion of total volume, of which $336 billion was for purchase.

“For 2025, we expect the decline in rates to boost refinance origination volumes,” the Freddie Mac economics team said.

“This, coupled with expected increase in purchase originations due to a modest growth in home sales and home prices, should improve the mortgage market in 2025.”

Zillow Chief Economist Skylar Olsen, in a 2025 outlook posting made on Nov. 25, pointed out that this year’s movements illustrate that “mortgage rates rarely follow the expected path.”

That means potential homebuyers next year should expect plenty of ups and downs.

“Mortgage rates fell in September, briefly bringing the share of affordable listings to a 19-month high,” Olsen said. “They have since climbed back to nearly 7%, changing the affordability picture for homebuyers. More swings like this are expected in 2025, with refinancing sprints occurring during the dips.”