Senior home equity declined in the third quarter off of its all-time high, due to lower property values combined with an increase in debt that they hold, the National Reverse Mortgage Lenders Association said.

The totals show this age group has plenty of room to tap the value of their homes if or when needed. But other reports show reverse mortgage production has slowed in the last couple of years.

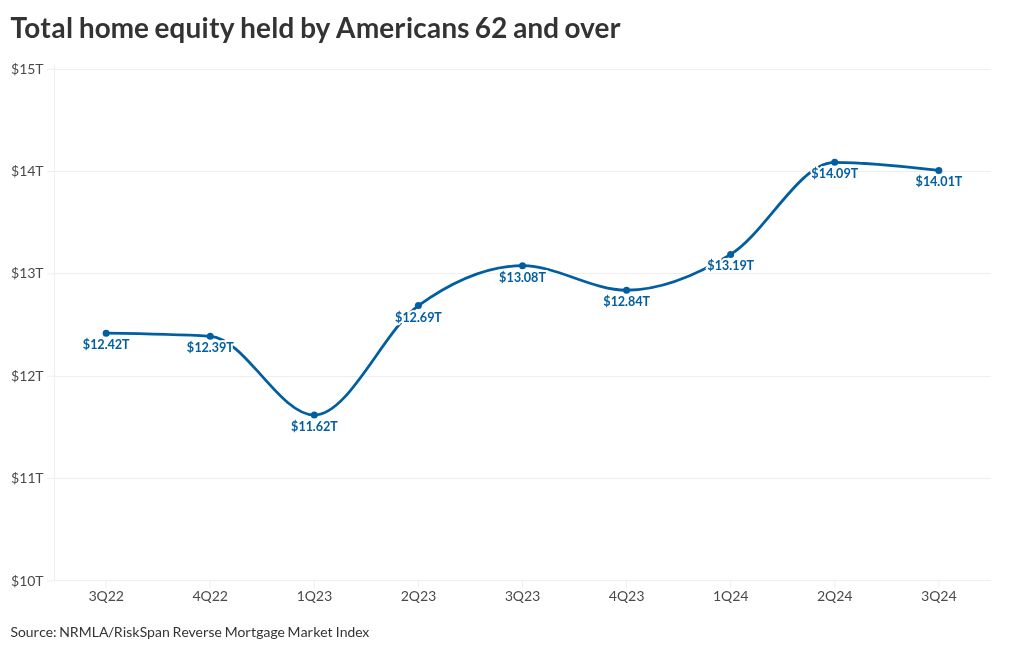

The NRMLA/RiskSpan Reverse Mortgage Market Index declined to 489.37 from 489.70 in the second quarter. On a dollar basis, the change was to $14.01 trillion from a record $14.09 trillion in combined equity held by homeowners 62 years old or over.

This drop in senior homeowner’s wealth was caused by a 0.3% (or $55 billion) decrease in home values combined with a 1% rise ($22.6 billion) in mortgage debt held by this age group.

“While most homeowners use a reverse mortgage to help pay for everyday living expenses or for home modifications to help them age in place, what they may not realize is that this product can also be used to purchase a new home that better fits their needs — without taking on a new mortgage payment,” said NRMLA President Steve Irwin in a press release. “As we kick off a new year, now may be the perfect time to consider the various finance options offered by reverse mortgage products.”

A December Consumer Financial Protection Bureau report using Home Mortgage Disclosure Act data showed the number of reverse mortgages that refinanced a first mortgage in 2023 was well below production in the low interest rate environment in 2022 and 2021.

Lenders reported approximately 29,000 reverse mortgage applications for refis in 2023, compared with 82,000 one year before that, and 75,000 in 2021. In 2020, the total was 58,000 while for 2019, it was 48,000.

Reverse mortgages originated during 2023 were 18,000, down from 52,000 and 50,000 in the prior two years.

Approximately 3,000 reverse mortgage applications and 2,000 originations in 2023 were used for home purchases, compared with 2,000 and 2,000 in 2022 and 4,000 and 4,000 for 2021 respectively.

Including all categories, 40,000 reverse mortgage applications and 25,000 originations were reported during 2023, down from 93,000 and 59,000 respectively for the prior year.

The CFPB report did not include data from 2024. During that year, the Federal Housing Administration endorsed 26,834 Home Equity Conversion Mortgages, according to Reverse Market Insight. HECMs are the predominant reverse mortgage originated, with proprietary products having a much smaller share.

The HECM endorsement total was a 12.2% decline from the previous year. Mutual of Omaha moved ahead of Finance of America as the leading HECM originator for the calendar year. But during fiscal year 2024, which ended on Sept. 30, the order was reversed, with Finance of America holding a 27.2% share and Mutual of Omaha at 24.8%.

What might benefit HECM volume in 2025 is the increase in the maximum claim amount for these loans to $1,209,750, the same amount as the high-cost forward mortgage conforming and FHA limit.

In addition, a recent Freddie Mac report noted that 68% of baby boomers expect to age in place according to a 2024 survey, down one percentage point from 2021 but up by two percentage points compared with 2016.

However, the share of homeowners who expect to have a comfortable retirement was well-below those prior surveys, at 68% in 2024, compared with 81% in 2021 and 76% for 2016.

Even so, other surveys, including one from Fannie Mae, found that the boomer generation is reluctant to tap their home equity for additional income.