Lenders can slash closing costs for consumers by streamlining their own operations and finances.

That’s particularly challenging given that the closing process has a lot of moving parts and jurisdictional differences. But companies that both have and use closing technology can decrease expenses in this area, according to research.

“There is, overall, a lot of process-oriented work that is involved in mortgage closing, and it is heavily labor intensive; but over a period of time, we also see this process getting heavily digitized,” said Rajul Sood, Acuity Knowledge Partners’ managing director and head of banking.

READ MORE: Why closing costs vary drastically across the US

Housing finance firms can save as much as 10 basis points through faster sales of loans into the secondary and capital markets, according to a survey by Snapdocs and Falcon Capital Advisors.

The study examined what the gains from the delivery of mortgages five days earlier through a digital closing employing hybrid, electronic note or remote notarization processes were.

Survey respondents found savings could be as high as 10 basis points for loan deliveries into the to-be-announced mortgage-backed securities market and one to two basis points in sales to aggregators.

In dollar figures, the average per-loan gross benefit was $115 for an hybrid process, $213 when that was combined with an e-note use; and for $283 for a full electronic closing utilizing remote notarization.

READ MORE: Closing-cost shopping: when to do it and why it’s limited

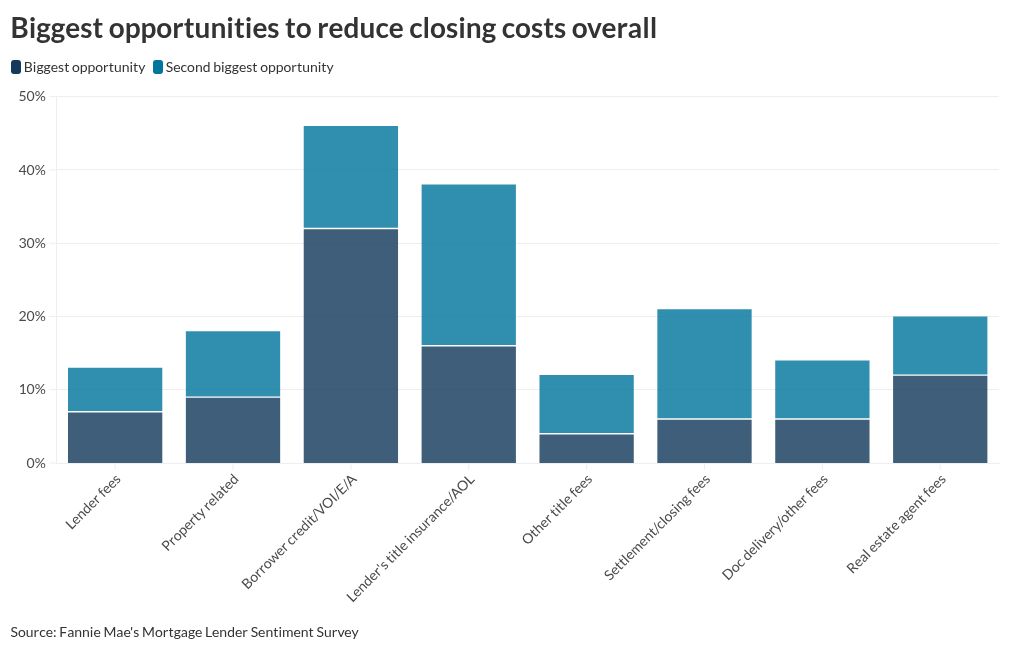

A separate Fannie Mae study looked at which part of the closing process offered the biggest opportunities to reduce costs. It found the most lender consensus around the part of the process concerned with borrower credit and verifications of income, employment or assets. Lender’s title insurance and attorney opinion letters ranked second, followed by settlement and closing fees.

The study, which was based on a survey of more than 200 senior mortgage executives also found that there were implementation challenges, the biggest of which was “getting key players to align on standardization.”

When automating is possible given that challenge, pricing improvement and error reductions are generally the biggest areas of savings, research suggests.

READ MORE: Error fees are draining lenders $1M per 1,000 loans

When the cost of having to make good on errors that require fee cures is considered, that category might be put at the top of the list, given ICE Mortgage Technology has calculated $1,225 per loan is spent on this expense, based on a review of 90,000 mortgages.

Even on a more general basis, a hybrid closing employing e-notes can reduce errors by 80%, accounting for the biggest component or $25 of a total potential $91 per loan savings in operational and processing costs.

Secondary and capital markets efficiencies can account for an additional $122 per loan in savings when a hybrid process and e-notes are utilized and provide a five-day reduction in the closing timelines, and the pricing gain represents the biggest component or $58 of that.

READ MORE: The outlook for home closing cost rules in 2025

Other secondary and capital markets efficiencies can come from savings generated between the interest paid to the warehouse lender and the interest paid by the borrower, custodial, shipping and investor penalty or hedge costs.

Additional operational and processing efficiencies can come from reductions in time spent on document management, post-closing quality control, funding or closing preparation, and lost or damaged promissory notes.