A sluggish housing market is leading mortgage volume forecasts to shrink in 2025, with political and economic uncertainty also throwing a dose of volatility into the mix.

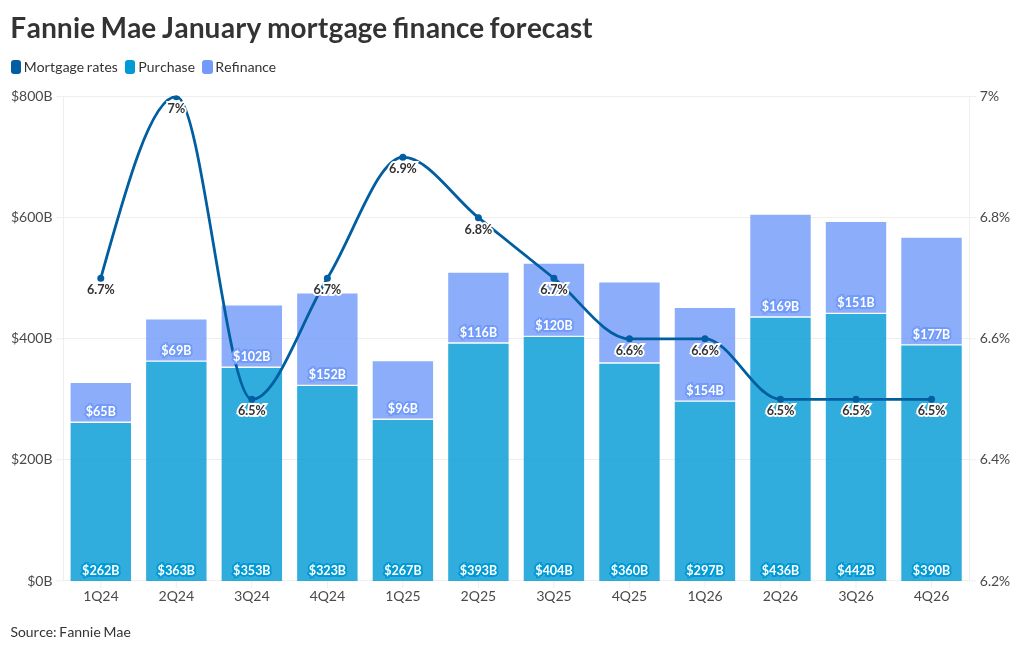

Fannie Mae revised its originations forecast downward while raising its anticipated year-end interest rate for 2025 in its latest economic outlook. Though not far off from the government-sponsored enterprise’s January numbers, the revisions suggest ongoing uncertainty to last throughout the year, with little expectation of a significant rush of business from improved market conditions that many had hoped for at the end of 2024.

Fannie Mae sees mortgage rates ending at 6.6% and 6.5% to close 2025 and 2026, respectively. The predictions are up from levels of 6.5% and 6.3% it published a month ago.

A strong U.S. economy entering 2025 provides little downward pressure on mortgage rates, but the effect of import tariffs is still not entirely clear, said Kim Betancourt, Fannie Mae vice president of multifamily economics and strategic research.

“Economic growth was strong to start the year as fourth-quarter personal consumption data came in above our expectations,” she said in a press release.

“Going forward, we expect the economy to decelerate slightly as consumer spending slows to a level more consistent with its historical relationship to income. However, ongoing uncertainty around trade policy adds risk.”

The forecast factored in the now existing 10% hike imposed on incoming Chinese goods. Additional tariffs on steel and aluminum imports, as well as all products entering from Canada and Mexico are currently scheduled to go into effect in March.

The direction of interest rate movements resulting from political developments depends on a number of variables that could lead to spikes and dips in lending, similar to what the mortgage industry saw in 2024, Betancourt added.

“Higher mortgage rates would exacerbate the existing ‘lock-in effect’ and worsen affordability, which may then weigh on home sales and mortgage originations activity. Of course, if mortgage rates move lower, we’d likely see an improvement in affordability and a corresponding pickup in housing activity,” she said.

With predicted year-end rates higher, Fannie Mae also pulled back its originations forecast to $1.89 trillion in volume this year from $1.92 trillion in its January research. For 2026, it expects mortgage volumes to eventually rise up to $2.22 trillion, coming in below the $2.27 trillion estimate of a month ago.

Of this year’s activity, purchases will account for approximately $1.42 trillion, close to the same number it predicted in January. Fannie Mae also pulled back the purchase origination forecast to $1.57 trillion from $1.58 trillion for 2026.

Revised refinance forecasts show originations coming in at $464 billion in 2025, $32 billion below last month’s outlook. In 2026, refinances will finish at $650 billion. Last month, Fannie Mae predicted $693 billion.

While 2025 might not result in the kind of change to brighten business sentiment, the originations number would still be higher than the $1.69 trillion the mortgage industry saw last year.

The gradual pace of mortgage growth also appears in research found elsewhere within the lending industry. In its latest credit insights report, Transunion said the number of mortgages originated during the third quarter last year came in 7.2% higher year over year. The latest surge was the sixth annual increase in the past seven quarters.

Still, the credit reporting agency echoed much of the subdued sentiment elsewhere, noting activity still lags a typical housing market.

“Despite recent quarters of growth, origination volumes continue to be depressed by historical standards,” said Satyan Merchant, Transunion’s senior vice president, automotive and mortgage business leader.

“Recent Federal Reserve indications that interest rate reductions may occur more slowly may result in decelerated growth in 2025,” he added.

Purchase originations made up an 82% share of volume during the quarter in Transunion’s analysis, a substantially larger slice compared to the average of 68% reported between July and October pre-pandemic.

Rate-and-term refinances also contributed to the third-quarter increase, as homeowners took advantage of a brief stretch when mortgage rates declined, with a 174% leap year-over-year.

The total number of mortgage originations should approach 5.7 million this year, with two-thirds expected to be used for purchases, Transunion said. Last year, the market saw approximately 4.6 million loans originated.