The Mortgage Bankers Association’s latest forecast for 2025 expects volume to be slightly lower than previously thought, with a 14% increase in the number of units produced.

Mike Fratantoni, the group’s chief economist speaking at its Secondary & Capital Markets Conference in New York on Monday, recounted discussions he had in recent days with people in the industry about the rate environment, with the consensus being it is better than last year.

He noted an expectation of the share of ARMs rising within originations overall. While the MBA predicts two cuts from the Federal Reserve this year, Jeana Curro, managing director and head of agency MBS research at Bank of America Securities said the depository does not expect any reductions this year.

This latest forecast captures the feeling of the industry right now, he said.

What factors impacted the updated MBA forecast

“A percentage increase off of a pretty low base,” Fratantoni said. “Nobody’s feeling exuberant about the housing market right now or about the mortgage market, but it’s a little better than these last couple years, which have been truly very difficult for a lot of our members.”

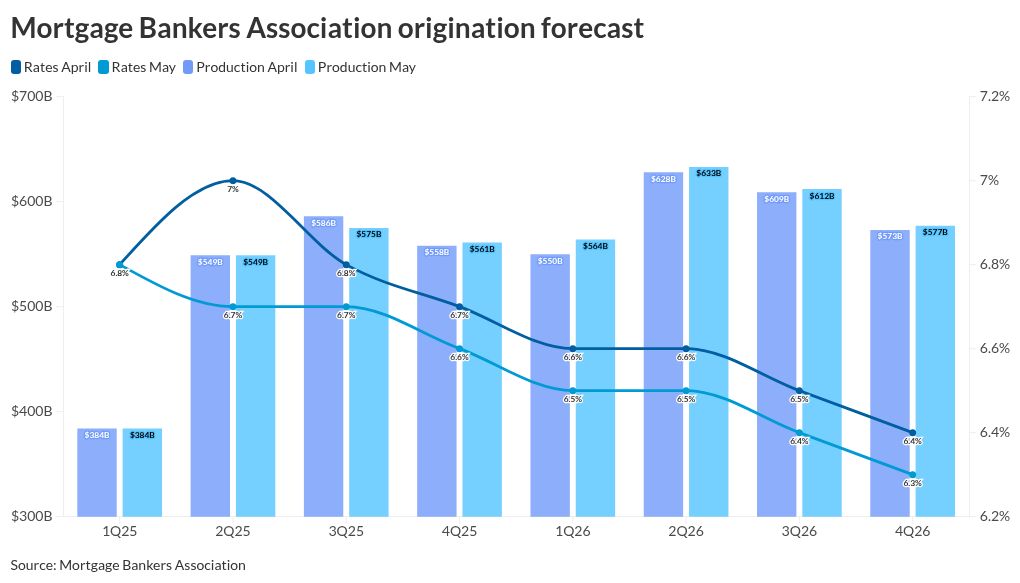

The May forecast drops the interest rate forecast to 6.7% for the current quarter, a 6.6% average for the fourth quarter and 6.3% by the end of 2026.

Fratantoni now expects dollar volume of $2.069 trillion this year, $2.386 trillion next year and $2.455 trillion for 2027.

Last month, the prediction was for $2.08 trillion in 2025. The purchase outlook was increased in May to $1.4 trillion, compared with $1.38 trillion in April.

Are Treasurys still considered a safe haven?

During his presentation, Fratantoni noted that the normal economic situation has not played out in the markets recently. In volatile times, capital flows from investors looking for safe havens into U.S. Treasurys, driving down yields and helping mortgage rates.

“Well, if U.S. Treasurys aren’t the safe haven that we thought they were, what is?” Fratantoni asked. “Is it gold? Is it Bitcoin? Is it some other asset? Is it real estate that’s going to be more likely to hold its value?”

Moody’s downgrade of the U.S. on Friday added “fuel to the fire” for investors who feel those bonds are no longer a safe haven, he said.

At noon Monday, the 10-year Treasury was just below 4.5%, after reaching 4.56% earlier, as a result of the Moody’s announcement. It closed Friday at 4.39%.

What is the range for the 10-year yield?

Fratantoni thinks the 10-year will be in the 4.4%-4.5% range going forward. At the same time, the abnormally wide spread between the 10-year and mortgages should narrow a bit, helping interest rates.

But he expects a steeper yield curve going forward, and that should help the continuing growth in government-guaranteed products, as well as the share of adjustable rate mortgages.

In a follow up panel, Steven Abrahams, managing director and head of investment strategy at Santander U.S. Capital Markets said investors have a new sense of caution about what is happening in this country’s economy.

“I don’t think that this suddenly means the end of the U.S. status as a safe haven, or the end of the dollar as a global store of value,” Abrahams said. “But we definitely saw a crack in the armor.”

Investors expected a lot of change after the U.S. elections, given what now-President Trump campaigned on, said Curro of Bank of America Securities.

But the change has happened faster than expected and that kept markets volatile, she added.

Why people are interested in ARMs

Building on Fratantoni’s earlier comments about ARM spreads, Curro noted an investor client she met with Monday morning asked about these securities.

“I do think it makes sense given the curve steepening,” she said. “I do think from an investor standpoint, given that it doesn’t feel like anyone wants to really extend the duration meaningfully just yet, it feels like the right product.”

Tactically for 2025, mortgage lenders need to focus on their purchase channel, but be ready for quick blips if rates go down, said Scott Buchta, senior managing director, Brean Capital.

Buchta noted that in this competitive landscape, some individual lenders reduced rates, with some banks in the low 6% range when everyone else was in the mid-to-high 6% area.

Points and other ways to cut rates

“Discount points right now are a big part of the game, especially on the purchase side,” Buchta said. “What you’re seeing is a lot of these below market rates and it’s not just one or two points, a lot of them are seller finance and builder finance.

Buyers are now more used to headline rates, so they are paying points. “A year ago, it was buy now, refi later,” he continued. “I think people are looking a little bit more longer-term.”

But to improve affordability, lenders have got to expand their offerings, he said and this involves understanding a lot of the different programs that are available from investors. Buchta gave the personal example of his son purchasing a home with a lower interest rate due to the fact that it was in an opportunity zone.