The anticipated impact of tariffs pushed consumers toward big-ticket items in April, but overall borrowing levels also show them becoming more discerning in light of political developments, according to Vantagescore.

Researchers noted earlier this year the likelihood of a bump in certain types of purchases before the implementation of various tariff measures proposed by President Trump. Evidence appeared notably in auto lending, but newly originated mortgages also saw an uptick.

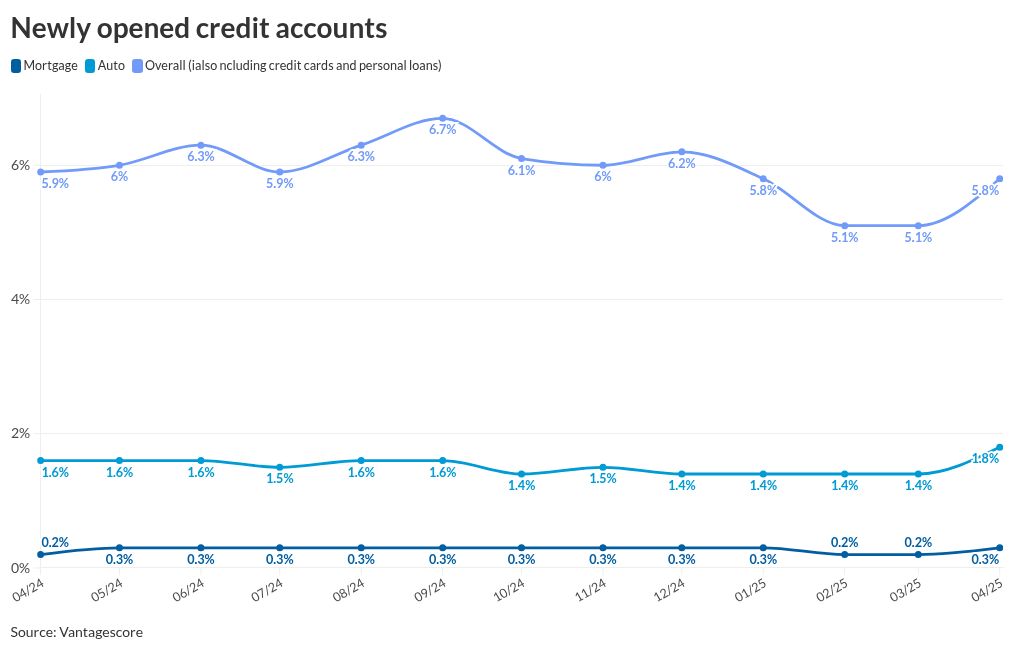

New auto originations increased to a nearly 1.8% share of consumers, up from the 1.4% level it held over the previous four months. The April rate was also higher than the 1.6% reported a year and in early 2020, immediately preceding the COVID-19 pandemic.

Mortgage originations edged up to 0.3% of consumers, rising from 0.2% on both a monthly and yearly basis. Sluggish sales activity has recent activity well below the 0.6% share in January 2020.

“Economic uncertainty was a driver of consumer decisions across all age groups in April,” said Susan Fahy, executive vice president and chief digital officer at Vantagescore, in a press release.

“Buyers appear to have accelerated their car purchases in anticipation of higher sticker prices due to the recently implemented tariffs,” she added.

Auto and mortgage borrowing contributed to an increase in the newly originated credit rate overall to 5.8% in April, up from March’s share of 5.1%, but just off from 5.9% reported 12 months earlier.

While some of Trump’s tariff proposals are on pause, others, including an across-the-board tax on steel and aluminum imports auto manufacturers and homebuilders often rely on, remain in place.

Despite the rise in originations, other data revealed borrowers becoming more “discerning” in their credit usage, Vantagescore said. Borrowing levels flattened overall, when all products, including revolving credit cards and personal loans, were factored in. Average credit balances rose by $14, or 0.01% compared to March. Balance-to-loan ratio, though, is on a downward trend in 2025, falling to 50.8% from 51.5% at the start of the year.

What auto delinquency levels mean for the mortgage market

Credit distress across all types of loans and delinquency periods decreased month to month to just under 1% of total outstanding balances, indicating short-term improvement in repayment activity. The number, though, rose from 0.9% one year ago.

A more pronounced rise in early-stage auto loans appeared with the share overdue by 30 to 59 days rising to 2.2% from 1.9%. On the other hand, mortgage payments late by 30 days dropped off to 0.9% from 1%.

The rise in early-stage auto delinquencies could portend emerging consumer distress if the trend holds. Borrowers’ payment hierarchy have them prioritizing mortgage payments first when they encounter economic challenges, followed by auto loans, making any spike in the latter worth observation.

“People definitely want to try to make their mortgage payments because the shelter is the first thing to make sure they have. Then, to get to work, they need that car,” said Rikard Bandebo, chief strategy officer and chief economist at Vantagescore, in a recent interview.

While mortgage distress is still low compared to pre-pandemic levels, it also is creeping upwards across credit-score tiers alongside auto delinquencies, Vantagescore researchers found.

The growth in late-payment rates is not restricted to specific income levels either, Bandebo said. Borrowers with higher income see lower rates of distress as expected, “but the rate of increase in delinquencies was growing much more in high income,” Bandebo said.

While counterintuitive, pandemic developments helped reshape the consumer landscape, he continued.

“It’s really wealth that is the bigger proxy for who’s doing well, because those that own assets, like homes or share portfolios or their own business, have seen the value of those assets disproportionately increase since COVID.”

The impact of student loan repayments stands to also drive delinquency rates upward. Late payments on student debt, which typically aren’t reported until 90 days past due, began reappearing on credit reports this year, steeply accelerating the share of later-stage delinquent accounts.

The overall rate of consumers with accounts overdue by three months or more shot up this year, surpassing the share of 30-to-59 day delinquencies, Vantagescore said.