It’s no secret that banks have lost interest in mortgage lending in recent years.

It has become very much dominated by nonbanks, companies that do not accept customer deposits or keep loans on their books.

Facilitating this trend has been the originate-to-distribute model, where mortgage companies make loans only to sell them off shortly after.

In the past, banks would actually keep the loans they made, but it has become a lot less common these days.

This may explain why the top three mortgage lenders last year were all nonbanks.

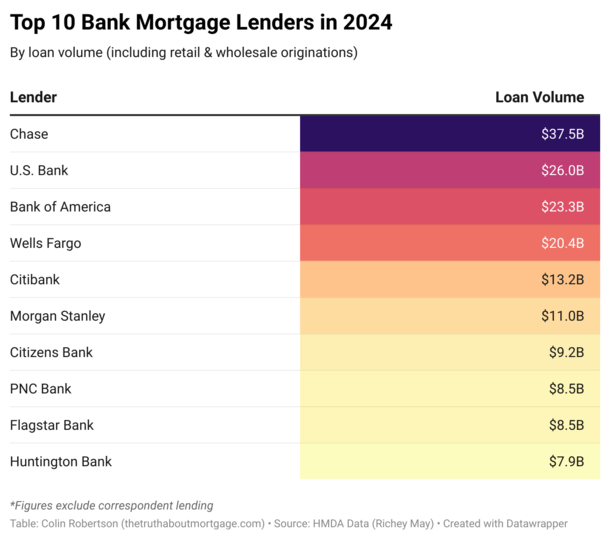

Chase Leads the Banks in Mortgage Lending Nationwide

I was curious to know which banks were dominating the mortgage space, despite ceding a lot of ground to nonbanks in recent years.

Easily leading the pack was NYC-based Chase Bank with about $38 billion in lending volume last year, per HMDA data.

They were followed by U.S. Bank with $26.0 billion and Bank of America with $23.3 billion.

Rounding out the top five were former mortgage behemoth Wells Fargo and Citibank.

Investment bank Morgan Stanley also made the list, as did Citizens Bank, PNC Bank, Flagstar, and Huntington.

While the numbers look okay, they pale in comparison to the nonbanks.

Top lender United Wholesale Mortgage (UWM) funded $137.8 billion while Chase only managed $37.5 billion.

Despite UWM working exclusively with mortgage brokers, they outperformed the top bank by a staggering $100 billion.

The nation’s second largest lender, Rocket Mortgage, did about 2.5X the volume of Chase too.

And even lesser-known CrossCountry Mortgage outpaced Chase by a couple billion as well.

Of course, we can’t blame Chase because they were still the top bank mortgage lender in the country.

Where were all the other banks? The answer: further down the list. Including former #1 Wells Fargo, who barely made the top-20 with a paltry $20 billion funded.

In total, nonbanks more than doubled the home loan production of the banks last year.

They funded $1.1 trillion in home loans versus just $491 billion for the banks.

It makes me wonder what would bring the banks back to mortgage, if anything.

Why Don’t Banks Want to Make Mortgages Anymore?

Earlier this year, WaFd Bank exited mortgage entirely, and their CEO said one the reasons why is that mortgages have become a commodity.

In other words, everyone just makes the same old 30-year fixed backed by Fannie Mae, Freddie Mac, or Ginnie Mae (FHA/VA loans).

You can go anywhere and get the same product, and it’s pretty much all government-backed, either explicitly or implicitly in the case of Fannie/Freddie.

At the same time, the nonbanks sell off all the loans they originate while the banks often hold onto them.

They do so despite not getting any additional business from the customer, who can also easily refinance their mortgage at any time and move away from the bank.

The WaFd CEO basically summed it by calling it a bad business, riddled with credit risk and interest rate risk. And because there’s no loyalty in today’s world, why bother?

Chase CEO Jamie Dimon Doesn’t Appear to Like Mortgages Either

While Chase is seemingly sticking with it, their CEO Jamie Dimon recently said they probably lost money on mortgages over the past 50 years.

He even went so far as to refer to the mortgage business as a “sh*tty business,” despite his bank ranking #1.

Why would he feel that way? Well, aside from claims to have lost money, he grumbled about the many rules and regulations tied to home loan lending.

Perhaps that was his way of hoping they ease up and make it easier for the banks, who knows?

But Chase is still plugging away and leading the nation in mortgage, partially thanks to their acquisition of First Republic after it failed in 2023.

The SF-based bank was a major jumbo loan lender that served ultra-wealthy clients, so Chase has undoubtedly gained volume from that pick up.

However, Chase only managed to place fourth on the list of top mortgage lenders last year.

Whether they look to make up ground remains unclear. Perhaps just being a megabank gets them that level of volume without too much effort.

Speaking of, Chase recently touted discounted mortgage rates for a limited time to drum up business. So who knows where they really stand on mortgages.