Foreclosure starts are notably up from last summer as the strain of today’s high-cost environment is affecting more borrowers.

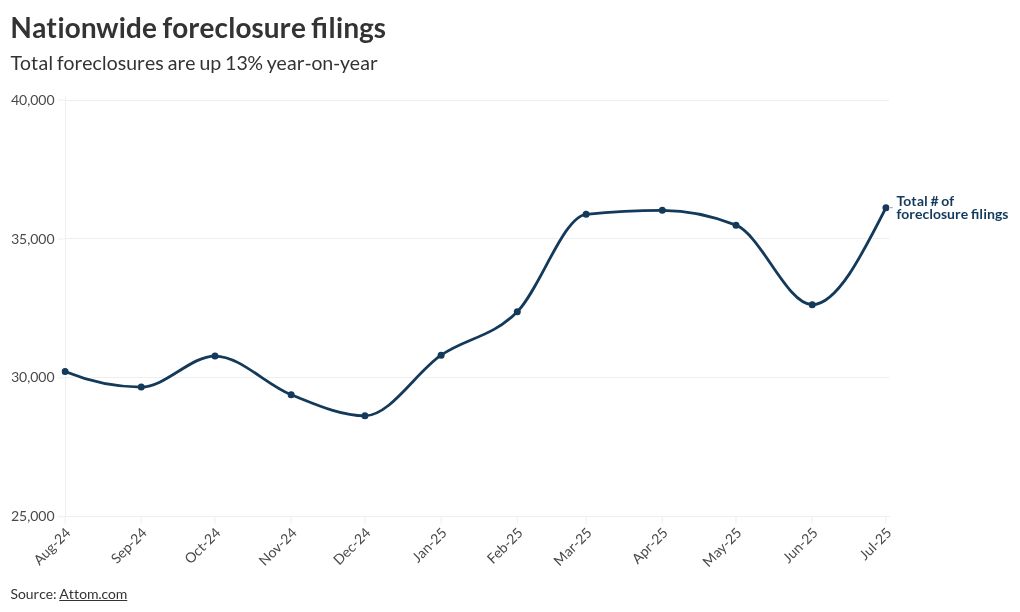

Lenders began the foreclosure process on 24,254 properties last month, up more than 17% from last August according to Attom. The total 35,697 U.S. properties with foreclosure filings last month represented 1 in every 3,987 homes with either a default notice, scheduled auction or bank repossession.

August was also the third consecutive month in which foreclosure activity grew by double digits year-over-year, Attom CEO Rob Barber said in a press release. On an annual basis however, foreclosures were down 1% from July.

The 4,077 completed repos last month was also up 5% from July but 41% greater than the same time last year.

The report didn’t speculate further on the pressures borrowers are facing, but challenges in today’s market include rising property taxes and homeowners insurance premiums. Delinquencies have also risen since the beginning of the year, according to a separate Cotality report, and the government recently reported anemic job growth.

Where are foreclosures rising?

Nevada had the nation’s worst foreclosure rate, and Las Vegas had the highest rate of foreclosed homes among cities with 1 million or more residents, with 1 in every 1,817 properties having a filing in August. The state’s high foreclosure rate was followed by South Carolina and Florida, which is home to both some of the nation’s hottest and coolest housing markets.

The states with the most REOs were the nation’s most populous, led by Texas which saw 476 REOs completed last month. While the largest Texas cities were among the top-5 nationwide with the most REOs, Chicago counted the most in August with 159.

The monthly trend follows a recent Attom third quarter analysis revealing 7,519 “zombie” properties, or unoccupied homes in the foreclosure process, a rate that has held steady in the past year.