In today’s digital age, lenders are keenly aware of the value in maintaining essential mortgage technology systems, but expenses that hold back some from moving forward on upgrades and improvements can cause future financial pain.

Having strong, reliable and new tools is top of mind at many lenders, but the decision-making behind applying changes isn’t as simple as a flip of a switch for some companies that have used the same solutions for years. A host of factors demand that company leaders take a nuanced look at the potential effect on every item in their technology stack when considering the value of additions or enhancements to a key platform, particularly their loan-origination system.

“It’s not just one piece of technology, it’s a stack of technology, and when they make those decisions, they invariably involve trade-off choices,” said Jim Deitch, co-founder of mortgage consultancy firm Teraverde.

READ MORE RESEARCH: Why growth in cap markets tech use is up and what it means for LOs

The trade-offs over the years has resulted in technical debt, as lenders opt not to move forward on software upgrades, “oftentimes for very legitimate reasons,” Deitsch said.

“This creates the technical debt that hampers the full use of the advancement of the tech platform,” he continued.

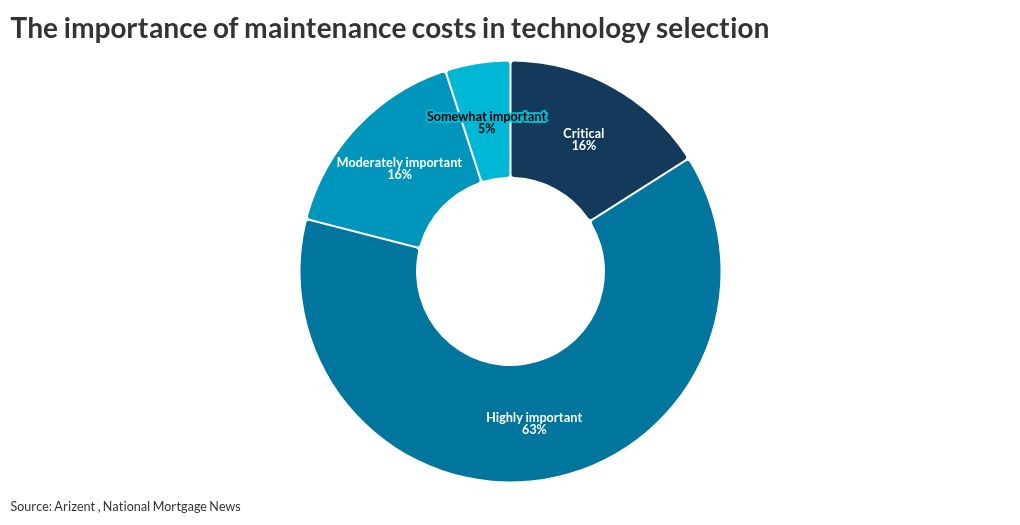

High among those reasons to move deliberately or even delay some maintenance or software additions is the cost. In a survey conducted by National Mortgage News this summer, 79% cited the expenses behind maintenance of any new tech stack software as a key factor behind their decision of which tools to add, if any. Of that share 16% said cost was a critical consideration while 63% called it highly important.

While many industry voices are actively leading the charge toward a digital mortgage future, a substantial share of lenders today still depend on tools that many would call outdated.

“I would say that typically, there’s been an accumulation of technical debt over the last 20, 30 years, especially for the legacy mainframe systems, that hasn’t been addressed.” said Mick Smothers, a former managing director at Ernst & Young and currently the founder and chief architect of technology consultancy firm Sophic Advisory.

For all the benefits of being among the first to adopt a new piece of software or an upgraded version, the stress of updating adjacent technologies in use serves as a disincentive, according to Deitsch. “You may have done other things with other systems that rely on the predecessor, which made sense at the time” he said.

MORE ON THE RESEARCH: Mortgage lenders top banks, credit unions in tech adoption

“But now, ‘I have this system in place. I have my people used to it. I’ve put a lot of other pieces that depend on existing standard conditions.’ It’s a really big deal to upgrade,” Deitsch added.

Rather than moving forward, lenders worried about the impact to bottom lines and staff production, especially during periods of high demand, are frequently “kicking the can down the road,” when they want to boost capabilities, Smothers remarked.

Instead of permanent changes, they apply what are meant to be temporary fixes or Band-Aids to give themselves added features they want, but the “solutions” only exacerbate technical debt

Businesses approach the changes with the idea of “someday we got to come back and actually create this function in our platform,” and then end up “never coming back to address that.” Smothers said.

Maintenance as modernization

Essential tech maintenance today can be viewed as going hand-in-hand with modernization, leaders emphasize.

Along with the cost of new digital tools, though, technology upgrades also require retraining, leading to a degree of unease or reluctance to move forward. Still, the status quo might be more costly.

“Stuff accumulates over time to the point where the cost to address all of that technical debt is prohibitive,” Smothers said. Along with the costs to keep systems operational, aging technology infrastructure elevates headcount numbers.

“When you have this technical debt, you’re substituting more labor to make up for it, and that’s the conundrum that the lender faces. You can substitute labor to do more manual effort to essentially work around the technical debt,” Deitsch said.

“At some point the question is, should I make the investment to improve the productivity of my technology and add more productivity and more bandwidth?”

The answer would be a resounding yes, according to Paul Gigliotti, chief growth officer at Prudent AI. Lender inertia results not only in costlier transactions, but higher rates of customer dissatisfaction and recruitment challenges that threaten lenders’ livelihoods, he said.

“The reason for the need to keep up with technology is the organizations that are tech forward tend to get the best cream of the crop for originators and be on the lookout for top producers as well as top level executives,” he said.

The complications involved with new technology implementation will provide gains, such as faster closing times, to sufficiently offset the pain.

“It allows you to be a top player,” Gigliotti said.

In an age when many consumer transactions can be done with ease digitally on phones and computers, borrowers have expectations their mortgage transactions can be handled similarly, he continued. Quick turnarounds and faster closing times will only come from the most up-to-date tools.

“Pretty soon, our consumer is going to say, ‘I am not sending you another paystub. You’ve seen it. It hasn’t changed. Get the loan done,'” Gigliotti said.

“As lenders, if we want to stay competitive, the consumers are our customers,” he added. “We have to be able to deliver their expectations.”

At the same time, maintenance and updates to newer technologies are also easier to incorporate and less expensive to implement today compared to older tools and bolster the case for lenders to invest soon instead of later, Gigliotti also noted.

For lenders still employing older platforms, a budget and plan to address maintenance needs or even a complete overhaul of entire systems needs to be on the agenda. The current mortgage market, with rates still above where most consumers would like, represents an ideal time to move forward.

“Something we’ve always preached is the downtime is the time to take these risks. Even though you might not be generating a lot of revenue, think of it as an investment to get out in front of the next boom,” Smothers said.

It also helps companies avoid having their vendors make decisions for them by retiring old versions of their systems, he added.

“Eventually the vendor has to say, ‘Listen, we can’t afford to support this platform anymore. We have this new one we want to move you to. We have a process to do that.’ Eventually that will happen.”

– This analysis is one of a multipart research series on mortgage technology disruption. Check back tomorrow for more analysis.