Waterstone Financial’s mortgage banking business recorded much higher net and pretax income in the third quarter compared to performance one year prior, even as the company produced 3.5% fewer loans.

The company, in both its mortgage banking and community banking segments, was able to sustain its improved performance for the year during the quarter, said William Bruss, CEO of Waterstone Financial.

“With improved earnings in both our community and mortgage banking segments, consolidated earnings totaled $0.45 per diluted share, which represents a 73.1% increase compared to the quarter ended Sept. 30, 2024,” Bruss said in a press release. “The mortgage banking segment recorded a second straight quarter of pre-tax income due to continued focus on expense management and improved margins.”

What are Waterstone’s mortgage financial results?

Using the pretax metric Bruss mentioned, Waterstone had $1.3 million of pretax income from mortgages, compared with $2 million in the second quarter and $144,000 for the same period last year.

But these profitable periods sandwiched pretax losses of $2.2 million in the first quarter and $625,000 in the fourth quarter of 2024.

On a net basis, Waterstone made $948,000 from mortgage banking in the third quarter, down from $1.47 million in the second quarter, but up from a loss of $50 million one year ago. The company has had up and down results in the mortgage business for at least three years.

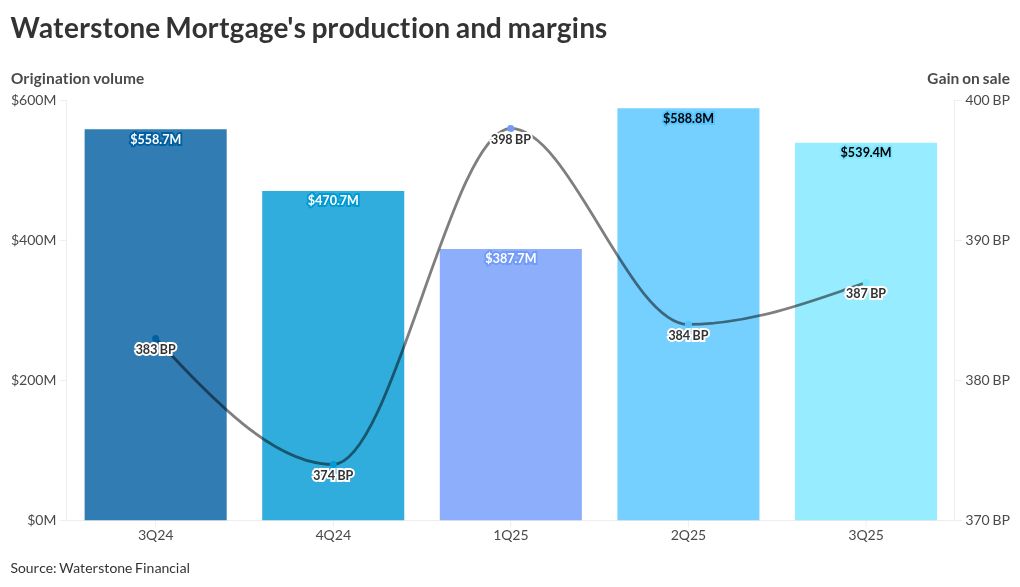

Loan production of $539.4 million in the third quarter was down from $588.8 million three months prior and $558.7 million for the same period last year. In the first quarter, Waterstone Mortgage had a net loss of $1.63 million, while three months prior it lost $197 million.

Gross gain on sale margins were only 4 basis points higher than the year ago quarter, 387 basis points versus 383 basis points. In the second quarter, the margin was 384 basis points.

How bonuses impact mortgage lender financials

Waterstone’s total compensation paid in the mortgage segment decreased by $214,000 from a year ago to $15.7 million. Waterstone said this was a result of decreases in commission expense, manager pay expense and salary expense which was partially offset by an increase in sign on incentives for new loan officers the company added.

Paying bonuses are a part of loan officer recruitment attempts, as well as retention efforts.

But compensation related expenses across the industry remain high, they did improve. Total loan production expenses as measured by the Mortgage Bankers Association — commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations — decreased to 321 basis points in the second quarter from 381 basis points in the first quarter.

On a dollar basis, this was $10,965 in the second quarter, down from $12,579, the MBA data showed.

What are Waterstone Financial’s results

Waterstone Financial reported net income of $7.9 million for the quarter ended Sept. 30. This compares with net income of $7.7 million in the second quarter and $4.7 million for the same period in 2024.