Loandepot leadership said the company has set the course for profitability but still ended up in the red at the end of the third quarter, posting a loss for the fourth straight earnings period.

The national lender reported a net loss totaling $8.7 million based on generally accepted accounting principles, with the total including fair-value changes in mortgage servicing rights. The company narrowed the loss by 65.4% from the second quarter’s $25.3 million. Over the same three-month period of one year ago, Loandepot recorded a profit of $2.7 million, which was its first positive result in nearly three years.

Despite recent challenges in getting over the hump back to profitability, the lender pointed to its diversification and changes implemented across the company after founder Anthony Hsieh returned as CEO earlier this year as investments that would pay dividends.

“The market is still highly fragmented. There is a ton of room chasing the leader in the space, so we’re very enthusiastic, and we are laser focused to stay on plan, get back into a standard of operations that allows us to be an industry leading mortgage bank,” Hsieh said on Loandepot’s earnings call.

“Having a fully diversified origination muscle — both builder and joint-venture market retail and direct-to-consumer model — really gives us an edge to scale up, particularly as we all hope there’ll be some growth and volume to a more favorable interest rate cycle next year,” Hsieh continued.

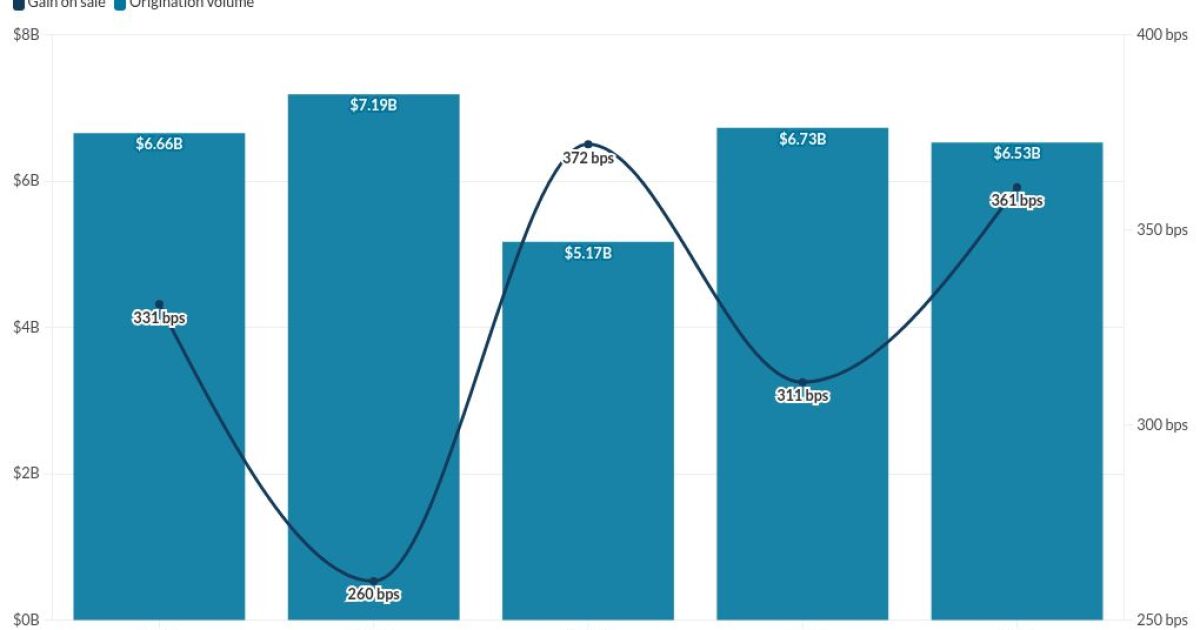

Third-quarter numbers came off of $6.53 billion in originations production, dropping from levels of both three months and one year earlier. The total decreased 3% from $6.73 billion three months earlier and 1.9% from $6.66 billion a year ago.

Gain on sale margins saw a bump up 361 basis points compared to 311 in the second quarter. On a year-over-year basis, gain on sale also increased from 333 basis points.

“Our higher gain on sale margin primarily reflected a channel mix shift with a higher contribution from our direct channel and a lower contribution from our joint-venture channel compared to the prior quarter,” said Chief Financial Officer Dave Hayes.

Unpaid principal balance in Loandepot’s servicing portfolio grew to $118.23 billion, rising from $117.5 billion in this year’s second quarter and $114.9 billion 12 months earlier.

Revenue between July and September clocked in at $323.3 million, reflecting an increase of 14.4% and 2.8% from $282.6 million and $314.6 million three months and one year earlier.

Loandepot’s new look since Hsieh’s return

Since his return to the helm of the Irvine, California-based company he originally founded in 2010 this past spring, Hsieh has largely reshaped the company in much of the image he helped create during his earlier leadership tenure. Notably, several recent appointments, including the return of some prior executives, bear the mark of Hsieh’s influence as the company tries to rise up among the ranks of industry business leaders.

“In the third quarter, we initiated a business transformation, including naming new leadership across all of our origination channels: consumer, direct, retail and partnership lending, as well as our in-house servicing platform. We also transformed our technology and innovation functions under new leadership,” Hsieh said.

While much of the personnel may now look familiar, the mortgage industry finds itself in a significantly different business environment compared to the last decade, leaving questions whether strategies employed in the past might work in today’s market.

“In order to really move forward, they need to be a more skilled player, drive their costs down to be able to generate more profits,” said director and senior equity research analyst at investment bank UBS Group.

“But if the market doesn’t come back, then they’re taking on extra costs at this point of trying to position themselves for growth. That’s the delicate balance,” Harter continued.

Shares of Loandepot’s stock saw a brief surge last month, where its value more than doubled from the beginning of the month to a closing high of $4.56 on Sept. 17. Social media chatter among retail investors helped drive up the value, briefly turning it into another meme stock.

Since its high, the equity has floated back down to a share price of $2.79 at the closing bell on Thursday, a number still well above where it sat throughout 2025 until the September surge.