Low mortgage rates that continued in October brought prepayment speeds to their highest share in approximately three-and-a-half years, the ICE Mortgage Technology First Look report said.

The monthly prepayment rate of 1.01% was up by 36.84% over September, when it was 74 basis points, and by 19.29% as compared to October 2024’s 85 basis points. On third quarter earnings calls, several mortgage lenders noted how strong September was for refinancings, including United Wholesale Mortgage and Rocket Mortgage.

At the end of October, the 30-year fixed fell to 6.17% from 6.34% at the start of the month and 6.5% for the first week of September, according to Freddie Mac. Since then, this rate has been on the rise, back to 6.26%, in large part a likely result of the lack of data because of the government shutdown.

For the week of Jan. 16, the 30-year fixed was over 7%; in the succeeding weeks, and again in April and July, rates were 50 basis points or more above the current level.

“Softening mortgage rates expanded the pool of refinance candidates in October, pushing prepayments to their highest level in three and a half years,” said Andy Walden, head of mortgage and housing market research at ICE. “This trend was largely driven by people who purchased homes at elevated rates in recent years seizing the opportunity to lower their monthly payments.”

Whether that softening trend will resume is unknown, even though yields on the 10-year Treasury moved off of their post-shutdown peak, which should help mortgage rates.

Between Oct. 16 and Oct. 28, the yield closed under 4% every day except for Oct. 17.

On Nov. 14, two days after the budget extender was passed and signed into law, the benchmark 10-year yield closed at 4.15%. The following Friday, Nov. 21, it was down to 4.06%.

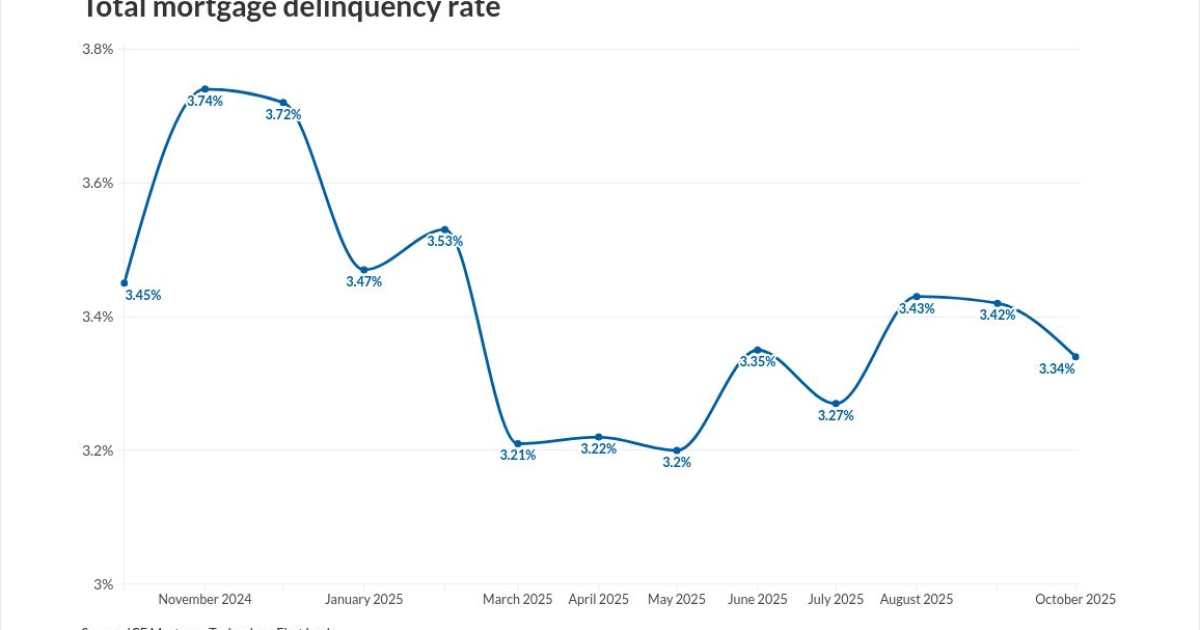

Delinquency rates continue to improve, the report found, with one blip on the horizon.

“While foreclosure activity has ticked up, levels remain historically low,” Walden said. “This uptick is driven by a rise in Federal Housing Administration foreclosures along with the resumption in Veterans Affairs foreclosures following last year’s moratorium.”

In the past, industry economists have said a rise in FHA delinquencies can foreshadow stress across the broader mortgage market.

The total delinquency rate, defined as any loan 30 days or more late on its payment but not yet in foreclosure, was 3.34% for October.

This was 8 basis points lower than September, when the rate was 3.42% and 11 basis points lower than 3.45% last October.

Total foreclosure starts numbered 38,000 units, a 9.83% month-to-month decline but up by over 29% compared with October 2024.

The number of properties in lenders’ foreclosure pre-sale inventory grew by 4,000 versus September and 37,000 over 12 months prior to 226,000.

Properties exiting foreclosure via a sale totaled 7,700, a gain of 8% over the prior months and over 32% compared with the prior year.

At the end of October, loans in active foreclosure were at their highest since 2023 because of the aforementioned growth in government-guaranteed products in this status.

The month ended with 1.84 million loans that were 30 days or more late on their payments but not in foreclosure, a decline of 36,000 units from September and 28,000 compared with last October.

The subset of 90 days or more late but not yet foreclosed upon totaled 476,000, which was 1,000 fewer than a month ago and 3,000 less than a year ago.

Including those properties already in foreclosure means the overall delinquent inventory grew by 9,000 units year-over-year to 2.07 million.