Rithm Capital’s mortgage operations are chugging along despite a large servicing valuation hit in the third quarter, but it has the tools in place for its desired borrower recapture opportunity.

The company Tuesday reported a $227.5 million net loss in its Newrez origination and servicing segment, including a $682.6 million change in fair value of mortgage servicing rights. That compares to a $208.7 million profit for the segment in the second quarter.

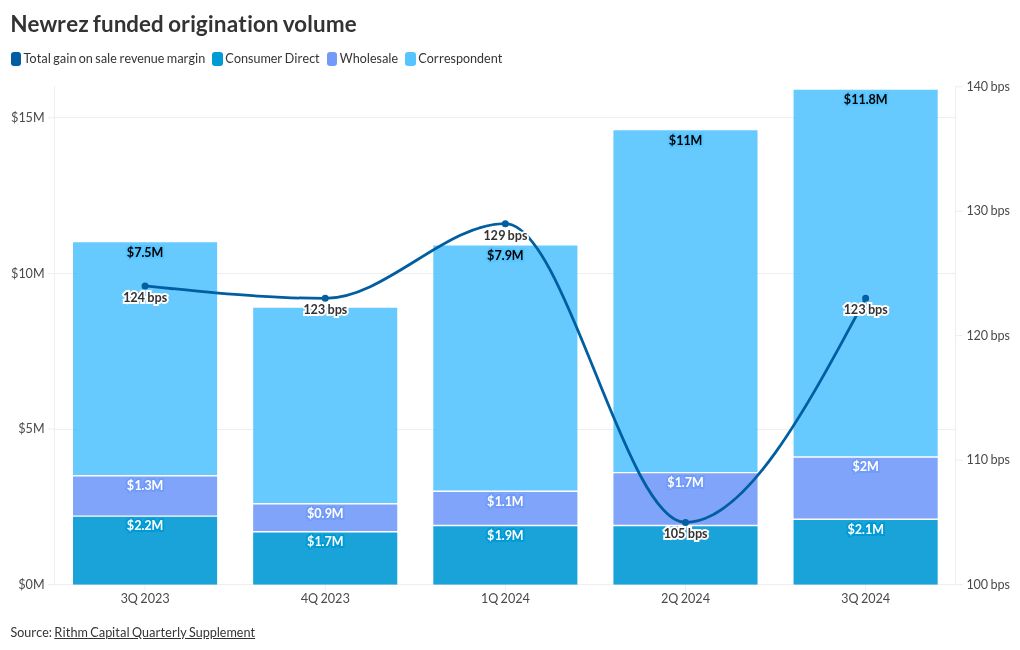

Its correspondent-heavy mortgage origination volume, however, grew to $15.9 billion in the third quarter, increases of 9% quarterly and 43% annually. Its overall gain-on-sale margin was flat from the year-ago period, but rebounded from 105 basis points in the spring to 123 bps in the third quarter.

Newrez’s unpaid principal balance, including third-party servicing, grew 34% from the last third quarter to $754.7 billion in the recent period. The self-proclaimed second-largest non-bank servicer in an earnings presentation suggested a $144 billion recapture opportunity within its portfolio, regarding borrowers with higher interest rates.

“We completed the first phase of our CRM rebuild in the second quarter of 2024, and we believe there is significant room to improve our ability to retain and continue to gain traction with our customers overall,” said Baron Silverstein, president at Newrez, in an earnings call.

The company touts a 3.4% mortgage market share, a servicing cost per loan of $113, and a consumer direct refinance recapture rate of 55% so far this year, including closed-end second liens.

Overall, the real estate investment trust had net income of $97 million, or $0.20 per diluted share, including its asset management and investment portfolio segments. The third quarter bottom line was around half of the figures it reported in the last quarter, and the $193.9 million in net income and $0.40 per diluted share in the year ago period.

Its Genesis Capital investor lending arm, which it acquired in 2021, also had a record third quarter, with $761 million in originations.

The New York-based firm’s long-mulled split of Newrez into a separate public entity could also happen next year, Rithm CEO, chairman and president Michael Nierenberg told analysts.

“There’s obviously other things we’re thinking about from an M&A landscape perspective, but I think it’s more likely going to be a (2025) event as we think about the mortgage company,” he said.

Nierenberg also opined on the upcoming election and its impact. Either incoming administration would have a difficult time passing legislation, and would face a growing federal deficit, he said. In the meantime, the company feels confident in its risk profile, and has $2 billion in liquidity.

“The way that we’re positioned now is to have an abundance of cash and liquidity,” said Nierenberg. ” … And that’s the way we’re going to run until we get some other kind of tea leaves that may rear their heads.”

Rithm’s stock trended up this morning on the earnings, trading at $10.67 per share as of late Tuesday afternoon.

BTIG analyst Eric Hagen said in a research note the Rithm isn’t receiving enough credit in its stock valuation for a “very strong track record” of hedging mortgage servicing rights marks against interest rate moves. The analyst is projecting $60 billion in originations for the firm over the next 12 months.

“The visibility for stable earnings at Newrez ultimately plays directly into the opportunity we think it can unlock as it looks to capitalize the asset manager,” he wrote Tuesday.