If you recall, Chase took over troubled First Republic Bank back in May 2023.

Prior to First Republic going under, they were the leading jumbo home loan lender in the United States.

They catered to very wealthy homeowners and businesspeople. And it was ironically their ultra-low rate mortgages that eventually took them down.

Today, Chase is the top jumbo loan lender in the nation, with production of more than $8 billion in the first half of 2024, per Inside Mortgage Finance.

Like First Republic, they too are wooing high-net worth individuals with special mortgage rate discounts.

Up to 1% Off Mortgage Rates If You Bring Money to the Bank

In 2023, Chase was the third largest mortgage originator in the country, per HMDA data. And the largest depository issuer of home loans.

They were only beaten out by two nonbanks, United Wholesale Mortgage and Rocket Mortgage.

Their acquisition of troubled First Republic has only made them bigger, and put an even stronger emphasis on jumbo loan lending at the bank.

In essence, they are carrying on some of the same principles, though likely with added guardrails to avoid the same fate.

One of those practices is offering mortgage rate discounts to their wealthiest customers, namely those willing to park lots of money at the bank.

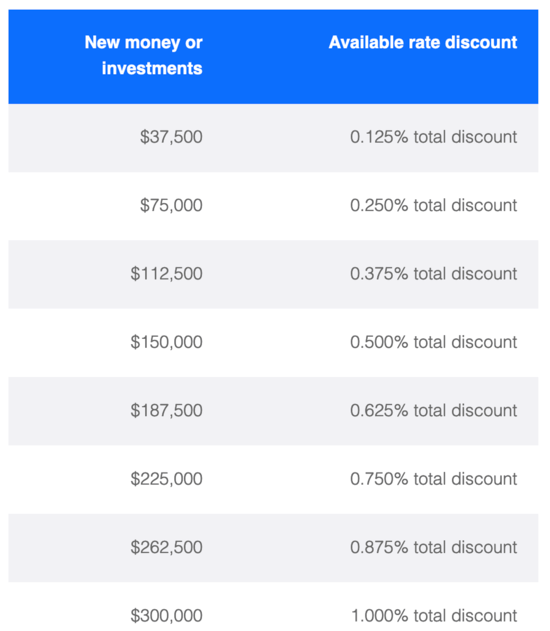

The NYC-based bank’s so-called “Relationship Pricing Program” offers mortgage rate discounts ranging from 0.125% and 1% based on new and existing balances at the bank.

These apply whether you’re buying a home or refinancing an existing mortgage.

As seen in the chart, those who can muster $37,500 in new money or investments can receive a 0.125% rate discount.

While that’s nothing big, customers who are able to bring in $300,000 in new money or investments can get a full 1.00% discount on their interest rate.

For example, if the offered mortgage rate were 6.5%, they could give you a rate of 5.5%. And that could be hard to beat by outside lenders.

On a large loan amount, we’re talking about some significant savings.

Using a $1,500,000 loan amount, the difference would be roughly $965 per month. Or $11,580 annually.

They also offer a rate discount of up to 0.25% for existing balances at the bank (0.125% for $500k-$999k, 0.25% for $1M+).

How the Relationship Pricing Program Works

To receive the interest rate discount, new money must be deposited in the customer’s Chase account at least 10 calendar days prior to the scheduled mortgage closing date.

Note that certain accounts don’t qualify, including business, deferred compensation, student, custodial, 529b college savings, donor-advised funds, select retirement accounts, and non-vested RSUs.

So make sure the new funds will actually count toward the discount.

Customers will be underwritten via the actual note rate before the discount, per Inside Mortgage Finance.

In other words, it doesn’t appear that you can qualify at the lower rate, assuming you needed to.

And note that funds that settle in a customer’s deposit and/or investment accounts 14 calendar days or more prior to the completion of a mortgage application aren’t eligible for the new money discount.

It’s also possible to receive a post-close rate discount if funds are received and settled within 30 days of loan closing.

But it might be lower than discounts available prior to closing, and the customer must sign a rate change modification.

These customers will also not receive a refund of any interest already paid prior to the rate change taking effect.

And while new and existing balance discounts can be combined, the total rate discount can’t exceed 1%.

Lastly, for adjustable-rate mortgages, the rate discount will apply during the initial rate period only.

For example, the first five years on a 5/6 ARM, or first seven years on a 7/6 ARM.

Good Deal or Not?

As with any of these types of deals, you need to compare what you could receive elsewhere.

I always look at the all-in cost of the mortgage. That includes both closing costs and the interest rate received.

A discount means nothing if another bank or lender can offer a lower mortgage rate with fewer closing costs.

For example, 1% off a rate of 7% is 6%. If another lender can give me 5.875%, who cares if it’s 1% off?

And how much do I need to pay to get that interest rate? Points, origination fees, etc.?

So take the time to compare offers, and also consider how much your money is expected to earn while parked in a Chase account.

There’s opportunity cost to consider here as well, which can cloud the comparison when expected returns aren’t guaranteed.

But if Chase is blowing the competition out of the water, then it might be a no-brainer and further reason to use them versus another mortgage company.