Reverse mortgage lender Finance of America announced plans for new marketing campaigns in 2025 after seeing multimillion profits return in the third quarter thanks to increased business volumes and fair-value gains.

The Plano, Texas-based company posted net income totaling $203.7 million, rising from a $5.1 million loss three months earlier. The latest number marked a year-over-year turnaround from a $174.9 loss compared to the third quarter a year ago.

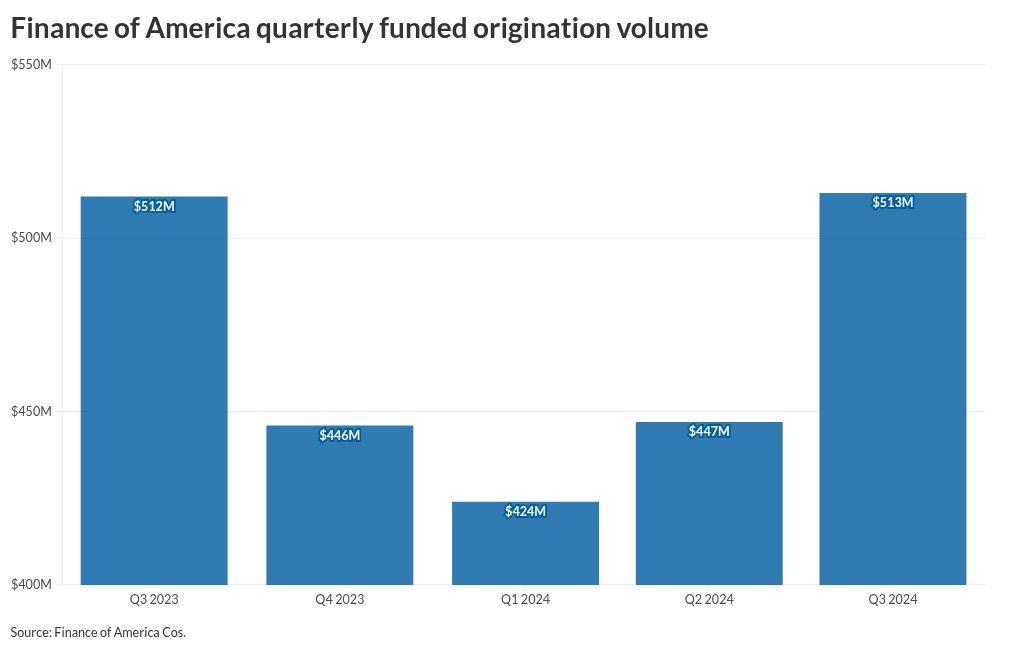

The company credited growing originations, particularly of its Homesafe second-lien product, for the improved results. Funded volume in its retirement solutions segment climbed up to $513 million from $447 million in the second quarter and near par to the $512 million one year earlier. Homesafe originations grew 89% quarter over quarter, company officials said.

The segment reported pre-tax income of $16 million, improving from a $2 million loss in the second quarter and a $20 million loss over the same three months of 2023.

“We surpassed our volume expectations and continued optimizing operations while staying dedicated to enhancing the customer experience,” said Finance of America Cos. President Kristen Sieffert in a company earnings call.

The successful integration of assets previously belonging to American Advisors Group earlier this year, as well as the unification of the former brand under the Finance of America banner also allowed the company to concentrate on growing the lending business. Finance of America acquired AAG in late 2022.

Further investment in the new combined brand will lead to investments in marketing, Sieffert said. “We are also focused on improving our overall marketing strategy with a new advertising agency, by introducing regional and local programs to build our brand profile and drive business and strategic markets starting in 2025,” she said.

Across the mortgage industry, lenders have ramped up their presence in the reverse mortgage space, as home equity consistently rises to record levels. In new research, the Mortgage Bankers Association also found baby boomers more likely to age in place rather than relocate, opening up a customer base for Homebase and other reverse products.

“We anticipate further growth in this area as we intentionally invest more capital and resources to the product,” Sieffert said.

Company leaders expect fourth-quarter funded origination dollar volume to be close to third-quarter levels and full-year 2025 to approach $2.7 billion, in spite of the current volatile rate environment.

In the third quarter, Finance of America’s portfolio management division also saw pre-tax profits of $217 million, jumping 886% from $22 million in the second, primarily through fair value adjustments resulting from higher interest rates. A year earlier, the segment posted a $124 million loss.

Total revenue across Finance of America also grew 267% to $290 million from $79 million between second and third quarters. In the third quarter of 2023, revenue had fallen into the red by $70 million.

In recent months, the company managed to address some of the issues that had raised concerns among trading regulators and ratings agencies. The company completed a 1-for10 reverse-stock split in July, putting it back in compliance with New York Stock Exchange policies. NYSE previously warned of possible delisting after the average value of its stock remained below the minimum level required for over a month.

The company also announced a debt exchange offer and consent solicitation for existing 2025 unsecured notes meant to address balance sheet issues. The offer saw a 98% participation rate, Finance of America said.

The restructuring, though, also led to a downgrade of some of Finance of America’s debt ratings. Fitch Ratings viewed the transaction as a distressed debt exchange, or DDE, “as it imposes a material reduction in terms compared with the existing contractual terms and is being done to avoid an otherwise likely eventual default.”

Fitch also cited low liquidity, high leverage and weak profitability among reasons behind the constrained ratings.