Freddie Mac’s latest economic forecast, while noting the policy uncertainty in the market right now, still calls for the Federal Reserve to keep to its “implied rate cut path” in 2025.

Its outlook was informed by what Freddie Mac defined as the top three trends in the housing market in 2024: jobs, rates and insurance.

While its November forecast did not take the election results into account, back then Freddie Mac felt economic conditions would keep the Fed on course for rate cuts going forward.

Mortgage rates are expected to decline gradually during the year which will boost home sales slightly over 2024, the December outlook notes. Unlike other forecasters, Freddie Mac does not provide detailed numbers in its outlook.

It also calls for home price appreciation to continue to moderate.

“This modest growth in house prices, and the increase in home sales should support the purchase market in 2025,” a blog post from the Freddie Mac economics team led by Sam Khater said. “We also expect refinance volumes to increase mainly based on declining mortgage rates.”

As for those three underlying trends for 2024 impacting next year’s market, first was the resilient labor market.

“Job openings and hiring rates stabilized compared to the post-pandemic recovery,” the post said. “As of November 2024, 1.98 million jobs were added to the economy, equating to 165,000 jobs per month.”

Next is the interest rate volatility for the full year, as the markets dealt with uncertainty around when the Fed would embark on a rate reduction program as well as the elections.

Since the Fed made its first cut in September, mortgage rates have climbed, ending November at 6.81%, Freddie Mac pointed out.

The 30-year fixed did decline in late November and early December, but for the week of Dec. 19 rose 12 basis points to 6.72%.

Even as Freddie Mac expects rates to “very gradually” decline next year, other forecasters, including Fannie Mae, say movements will continue on their wild ride in 2025.

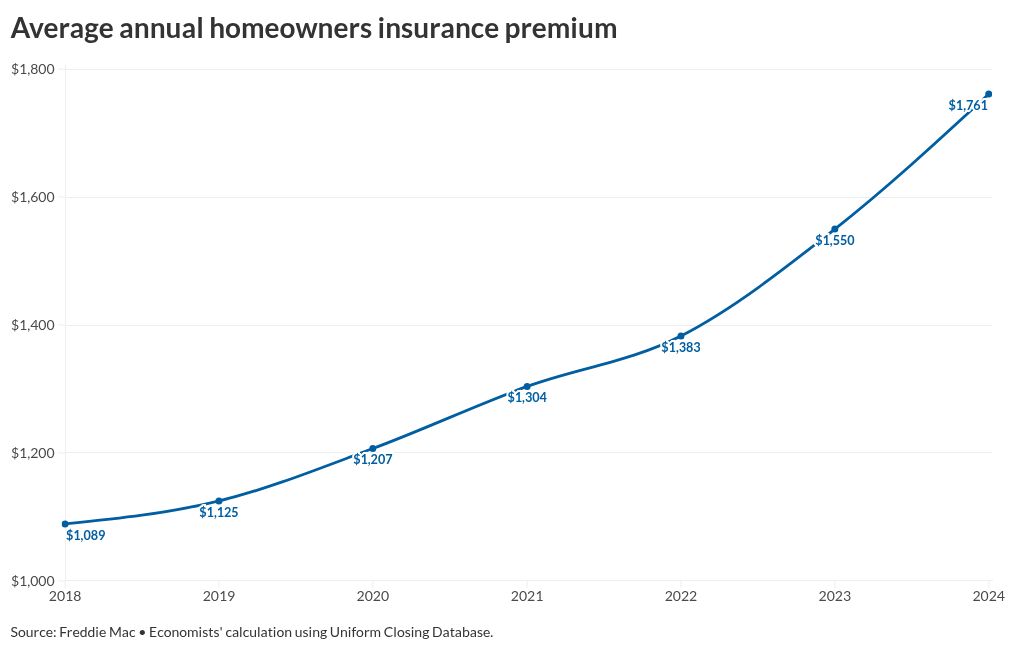

The third and final theme for 2024 was the rising costs of homeowners insurance.

An average borrower paid an annual homeowners insurance premium of $1,761 as of August. This was 13.6% higher than they did in 2023 and 61.8% higher than in 2018.

Lower income property owners are more affected by the increased cost of homeowners insurance compared with moderate- and high-income borrowers.

Low-income borrowers spent 3.4% of their monthly income on premiums, as of August. This compared with 1.7% for the average borrower.

“The impact of high interest rates and home prices affecting the principal and interest payments is much larger than the net impact of insurance cost, but it is still a significant burden on marginal borrowers trying to get into the housing market as well as homeowners with fixed incomes,” Freddie Mac said.