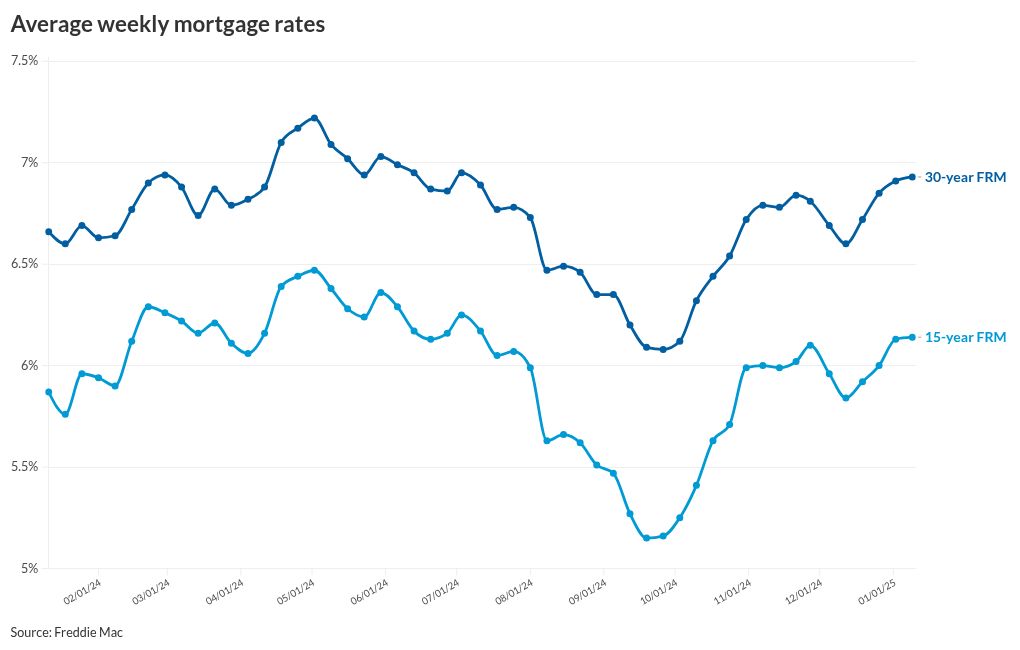

Mortgage rates rose again this past week, but are still just shy of 7%, as the benchmark 10-year Treasury continues its rise due to the ongoing economic uncertainty, Freddie Mac said.

The 30-year fixed-rate mortgage averaged 6.93% as of Jan. 9, a 2 basis point rise from last week, when it was at 6.91%, the Primary Mortgage Market Survey found. One year ago it averaged 6.66%.

Meanwhile, the 15-year FRM averaged 6.14%, a 1 basis point gain week-to-week from 6.13%. For the week of Jan. 11, 2024, the 15-year FRM averaged 5.87%.

“The continued strength of the economy has put upward pressure on mortgage rates, and along with high home prices, continues to impact housing affordability,” said Sam Khater, Freddie Mac chief economist, in a press release. “The lack of entry-level supply also remains an issue, especially for those looking to become first-time homeowners.”

The 10-year Treasury yield closed at 4.68% on Wednesday. That was a 10 basis point gain from Jan. 2, when it closed at 4.58%.

Markets were closed on Thursday because of the national day of mourning for Pres. Jimmy Carter.

Lender Price data posted on the National Mortgage News website had the 30-year FRM at 7.15% on Thursday morning, compared with 7.22% one week prior.

Zillow’s rate tracker for the 30-year FRM was at 6.74% on Thursday morning, up 5 basis points from the previous week’s average of 6.69%.

The rise in the 10-year Treasury is being influenced by other factors in addition to how many times the Federal Open Market Committee will cut rates this year, such as increased government spending leading to more borrowing, said Kara Ng, senior economist at Zillow Home Loans.

“Inflation remains top of mind for the Federal Reserve, as the Fed and businesses react to new government policies,” said Ng in a statement. “In a recent data release, the price component of the Institute for Supply Management’s services index surprised to the upside, and hit the highest level in almost two years, suggesting that businesses may anticipate tariffs to raise prices for goods and services.”

While more houses for sale should help the market in 2025, higher mortgage rates will affect affordability, leading some priced out of buying a property staying renters longer, and thus putting upward pressure on those.

“There are still a few months before the home shopping season begins in earnest, with plenty of opportunity for policy announcements and data moves to drive rates higher or lower,” Ng commented.

Odeta Kushi, deputy chief economist at First American, said based on the Fed’s comments, two short-term rate cuts are likely in 2025. That would keep monetary policy restrictive, as those would remain above the Fed’s definition of neutral.

“As the Fed maintains a ‘higher-than-goldilocks’ stance, mortgage rates likely will also remain above 6%,” Kushi said. “However, mortgage rates may drift lower from 2024 levels, in part driven by some narrowing of the mortgage rate spread as the Fed’s policy outlook becomes clearer.”

The rate environment will affect the decision to sell, keeping inventory lower than pre-pandemic levels, Kushi said.

“Mortgage rate volatility will persist until the Fed’s policy outlook becomes clearer, and the mortgage rate lock-in effect will prevent a full housing market recovery,” she said. “Nevertheless, the 2025 housing market is poised to make strides forward — offering progress, but still far from perfection.”

Mortgage rates are likely to trend higher until the market gets a sense of Pres. Trump’s economic policies, said Jacob Channel, senior economist at LendingTree, in his outlook.

“If he goes through with inflation-inducing policies such as tax cuts, blanket tariffs on key trading partners and mass deportations, mortgage rates will probably trend higher,” Channel said. “Similarly, if he succeeds in ending Fannie Mae and Freddie Mac’s government conservatorships (something he tried in his first term), that would put significant upward pressure on mortgage rates,” likely driving them well-above 7%.