In a trend unlikely to continue into April, mortgage prepayment activity increased 30% during March, to its highest level since November, the ICE Mortgage Technology First Look report said.

The 59 basis point prepay rate compared with 46 basis points in February and 48 basis points for March 2024.

The 30-year fixed was in a tight range for much of March between 6.6% and 6.7%, its lowest levels since October, according to Freddie Mac.

However, following President Trump’s tariff announcement on April 2, bond yields spiked, pushing mortgage rates close to — and according to some sources, even above — the 7% mark in the days that followed.

The March rate drop was one of the reasons Mr. Cooper had to take a $82 million write-down to the value of its mortgage servicing rights in the first quarter.

In its direct-to-consumer channel, almost half of its production was cash-out refis, while another 14% were for rate-and-term loans. The 20% purchase share likely included buyers paying off the mortgage on their previous home.

Pennymac Financial Services took an almost $99 million charge to its earnings on the MSR valuation.

How many borrowers actually qualify for a refi?

In a separate study, Ardley disputes the commonly cited number of 6% of current mortgage borrowers with rates over 6.5% qualifying for a rate and term refi. Ardley found that just 1.48% actually are eligible as of the end of the first quarter.

If rates fall 25 basis points from end of first quarter levels, the refinancable population grows to 1.99%, and a 50 basis point drop, the pool grows to 2.69%, both still short of that 6% figure.

“There’s a big difference between theoretical eligibility and actual qualification,” said Nathan Den Herder, CEO of Ardley Technologies, in a press release. “Media coverage often zeroes in on rate thresholds, but real qualification depends on second liens, credit profiles, [net tangible benefit] calculations, and other nuances.”

Rate-and-term loan applications submitted in March made up 88% of the first quarter total in this product. For cash out refis, 81% of the application volume was in March, further supporting ICE’s data on prepayment speeds for that month.

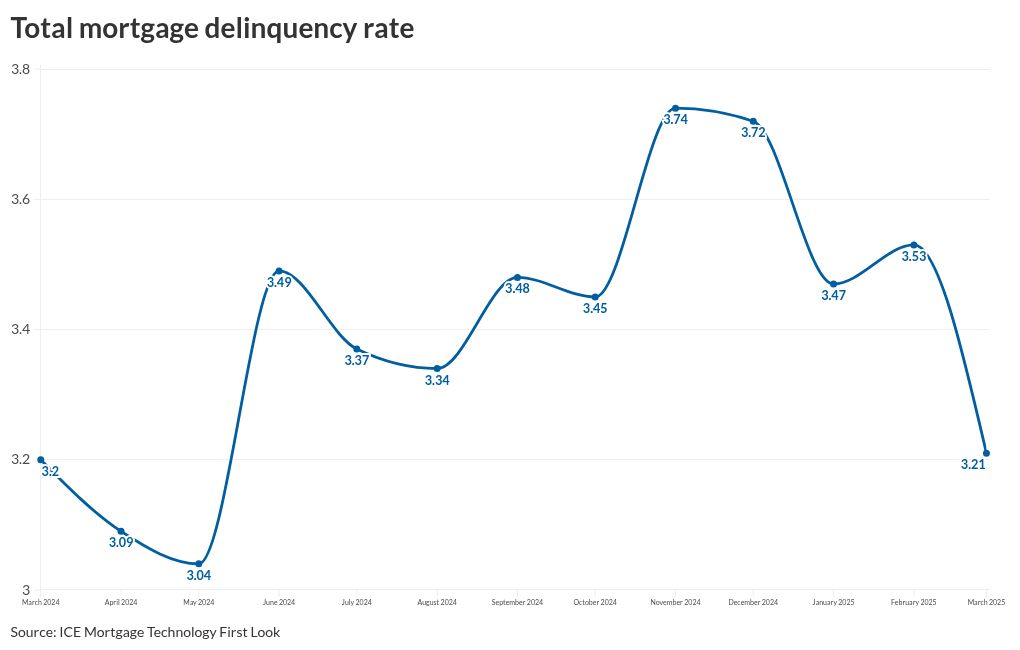

Delinquencies drop to 10-month low—but not everywhere

Meanwhile, the total delinquency rate for March was 3.21%, down 32 basis points from February, and up by 1 basis point from a year ago, ICE Mortgage reported. This is the lowest the rate has been since last May when it was 3.04%.

But several states impacted by natural disasters like hurricanes and wildfires recorded increases in year-over-year delinquency rates, led by Florida (up 44 basis points), South Carolina (17 basis points), Georgia (14 basis points) and California (10 basis points).

FHA delinquencies surge, driving foreclosure activity up

The number of loans which are seriously delinquent (90 days or more late on the scheduled monthly payment, but not yet in foreclosure) fell by 33,000 between February and March but increased by 60,000 from March 2024 to 495,000.

But this is a 40,000 increase from one year ago, driven entirely by the annual increase in Federal Housing Administration serious delinquencies, which were up 63% compared with March 2024, ICE said.

As a result of the increase in loans 90 days or more late, along with the lifting of a foreclosure moratorium on Veterans Affairs-guaranteed mortgages, fueled a modest bump in foreclosure inventory and sales, which both rose annually for the first time in nearly two years.

Foreclosure sales increased 4.4% compared with March 2024 to 6,100 units, while the presale inventory added 7,000 loans over the 12-month period to bring the total to 213,000.