Early- and mid-stage mortgage delinquencies saw the biggest yearly increases among all credit products, a development Vantagescore deemed a “surprise”, which “may be demonstrating early signs of borrower financial stress.”

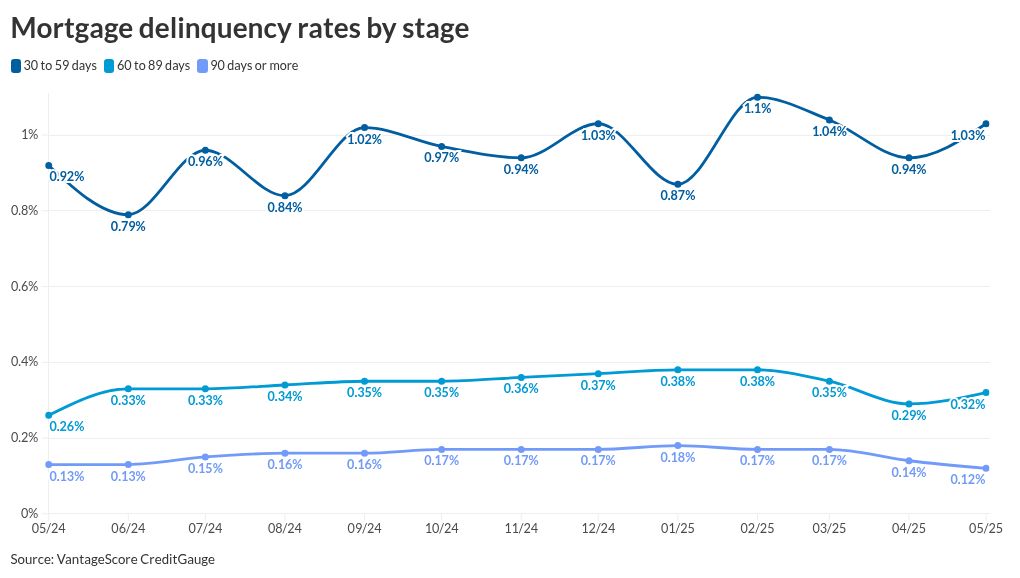

The share of mortgages 30-to-59 days behind on payments jumped to 1.03% in May from 0.92% during the same month a year earlier. Among all types of accounts 60-to-89 days past due, mortgage holders’ share grew to 0.32% from 0.26% in May 2024. The increase in both stages exceeded the pace seen in all other types of loans monitored by the credit-scoring agency in its monthly gauge.

By comparison, shares of early-stage delinquencies increased by just 0.08% for auto lending and 0.02% among personal loans compared to May 2024. Credit cards, though, posted an annual rate decrease of 0.05%.

The data signals consumer difficulty ahead if trends hold, the Vantagescore report said.

“The rise in early and mid-stage delinquencies this month indicates potential financial strain among some consumers,” said chief digital officer Susan Fahy in a press release.

The increase in home loan delinquencies, in particular, came as a surprise because consumers typically prioritize mortgage debt over other credit payments, Vantagescore noted.

“Mortgages may be an area to watch for increasing credit stress, particularly for traditionally less risky segments,” Fahy also remarked.

The average mortgage loan balance held by American consumers trended upward, as it has every month this year, coming in at $267,700 in May. The total increased 2.8% from $260,400 on a year-over-year basis, and 0.3% from April’s $266,900.

The mortgage balance-to-loan ratio stood at 79.9%.

What’s fueling consumer credit distress?

Vantagescore’s findings come as consumer worries about personal financial situations worsened this spring, according to recent research published by the Federal Reserve Bank of New York.

The percentage of consumers who feared they may miss a payment rose at the same time their outlook regarding their personal financial situation “deteriorated sharply,” Fed researchers reported. Labor worries, including both wages and the likelihood of finding work, contributed to a higher degree pessimism.

Ongoing volatility in interest rates, with a majority of consumers expecting them to increase further, means homeowners are finding little relief in housing affordability as average new monthly payments consistently run above $2,000 since 2023, according to the Mortgage Bankers Association.

Uncertainty surrounding tariff policies is also leading to consumer worries, with many, including some in the housing market, anticipating price hikes to come due to the impact of the import taxes.

Credit quality is across the country

The average credit score held steady at 702, as it has for all but one month over the past year. February saw a brief dip to 701, Vantagescore’s credit gauge report said. New Hampshire borrowers posted the highest average of 727 last month, with Mississippi coming in at the bottom at 668.

New credit accounts of any type opened in May accounted for 5.9% relative to the total volume of existing accounts, edging down from 6% a year ago but inching up from April’s rate of 5.8%.

For mortgages by themselves, new loans came in at an approximately 0.3% share. The number has remained within the 0.2% to 0.3% range since November 2022.