New mortgage delinquencies showed overall improvement in loan performance, but in what could be a more concerning trend, later-stage distress and foreclosures trended upward in the second quarter.

The overall delinquency rate decreased to a seasonally adjusted 3.93% during the quarter, reflecting pullbacks from both three months and one year earlier from 4.04% and 3.97%, respectively, according to the Mortgage Bankers Association. The historical average stands at 5.21%.

“Conventional loan performance continues to perform exceptionally well, with delinquencies hovering near record lows,” said Marina Walsh, MBA vice president of industry analysis in a press release.

Potential signals of financial issues plaguing some borrowers, though, appeared in later-stage distress. “While overall mortgage delinquencies are relatively flat compared to last year, the composition has changed,” Walsh added.

“Earlier-stage delinquencies declined while serious delinquencies — those loans 90 or more days delinquent or in foreclosure — increased. This was the case in the second quarter of 2025 across the three major product types,” she added

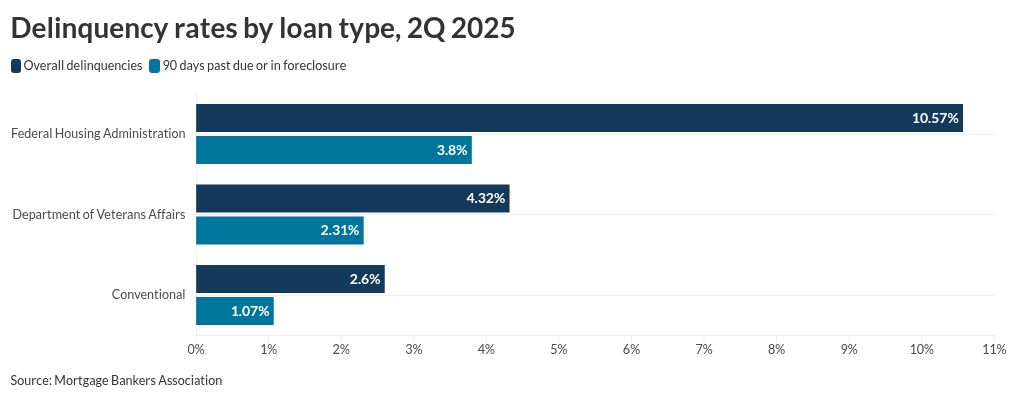

The share of loans either 90 days or more past due or in foreclosure jumped up 14 basis points year over year to a non-adjusted 1.57%, with Federal Housing Administration-backed loans driving much of the increase due to a 63 basis point rise to 3.8%, according to the survey. Meanwhile, loans backed by the Department of Veterans Affairs also saw a hefty 24 basis point jump to 2.31%. While more muted, latter-stage conventional delinquencies and foreclosures grew by 3 basis points annually to 1.07%.

The latest numbers, though, represented a pullback of 6 basis points from the first quarter, which likely saw elevated foreclosure numbers after the expiration of a moratorium affecting VA-backed loans in late 2024. Ninety-plus day late shares receded on a quarterly basis for all loan types.

The growth in foreclosures and end-stage delinquencies corresponds to rising signs of economic weakness reported recently, including in the most recent government jobs report, MBA said. Meanwhile, rising delinquencies in other forms of consumer debt, such as student loans, credit cards and auto lending, could serve as potential precursors to rising mortgage distress.

By contrast to the late-stage numbers, the 30-day delinquency rate improved to 2.1% from 2.26% one year earlier. On a quarter-to-quarter basis, the 30-day share eased 4 basis points from 2.14%.

Mortgages 60-days or more past due came in at a share of 0.72%, down from first quarter’s 0.73%, but up 2 basis points from 0.7% year over year.

How mortgages are performing overall by loan type

For conventional loans, the overall seasonally adjusted delinquency rate decreased to 2.6% from the first quarter’s 2.7% and 2.64% a year ago. While conventional loan borrowers have showed resilience, their performance “contrasts with the rise in government delinquencies over the past few years,” Walsh noted.

Still, both FHA and VA delinquencies fell on a quarterly and yearly basis. The FHA delinquency rate stood at 10.57% at the end of the second quarter, while for VA borrowers, it was 4.32%.

Foreclosures, which are not included in the overall delinquency rate, edged down a single basis point from the prior quarter to an 0.48% share. The percentage, though, increased from second-quarter 2024’s rate of 0.43%.

MBA’s latest foreclosure numbers come after other data providers, including Attom and ICE Mortgage Technology, reported a similar rise in recent months.