Those who expected lower mortgage rates in the immediate aftermath of yesterday’s Federal Open Market Committee actions are likely disappointed with the early market response.

The 10-year Treasury yield rose to 4.13% at 11 a.m. Thursday, up 5 basis points from its close at 4.08% at 3 p.m. on Wednesday, an hour after the Fed announcement.

At one point on Wednesday, for the second time in a week, the yield did slip below 4%. Last Thursday, the 10-year ended the day at 4.01%. The 10-year yield is generally indicative of the 30-year mortgage rate’s direction.

Zillow’s rate tracker was 10 basis points higher than Wednesday’s average as of 11 a.m. Thursday, at 6.52% for the 30-year fixed rate mortgage. The average for a week ago was 6.45%.

Lender Price’s product and pricing engine data posted on NMN’s website at that same time was 6.42%, up almost 5 basis points on the day. A week ago, it was at 6.41%.

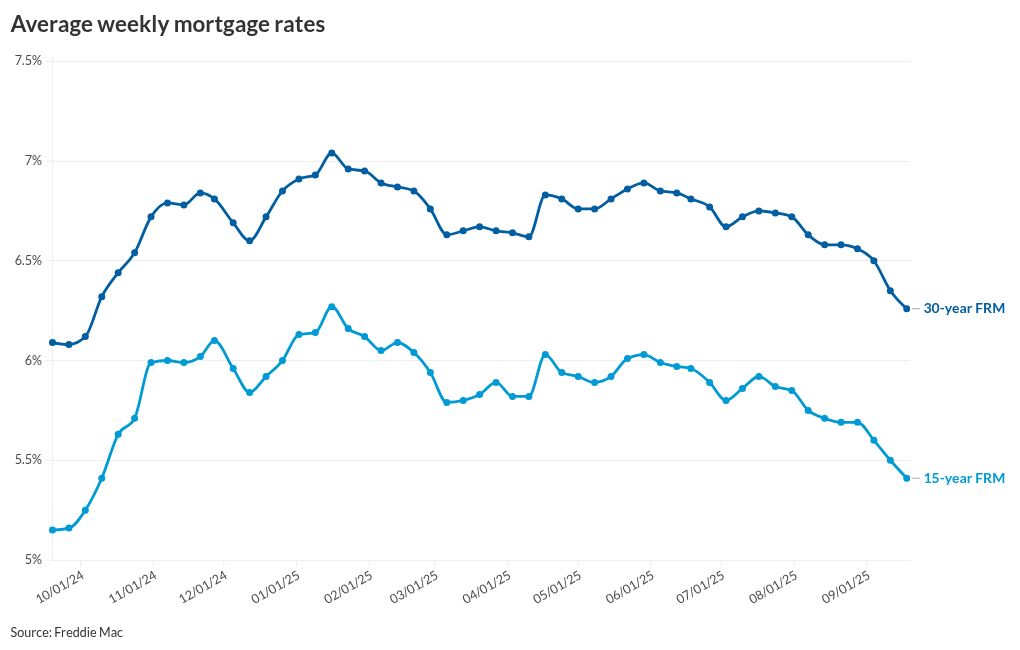

What the Freddie Mac Primary Mortgage Market Survey reported

Freddie Mac’s Primary Mortgage Market Survey did drop another 9 basis points last week, reflecting price changes many lenders made in anticipation of the FOMC meeting.

The 30-year FRM averaged 6.26% as of Sept. 18, down from last week’s 6.35%. A year ago this week, the 30-year FRM averaged 6.09%.

Meanwhile, the 15-year FRM at 5.41%, was down from last week’s 5.50%. However, it also remained much higher than one year ago, when it averaged 5.15%.

Last week’s rate movements did spur some borrowers to seek out their lender.

“Mortgage rates decreased yet again this week, prompting many homeowners to refinance,” said Sam Khater, Freddie Mac’s chief economist, in a press release. “In fact, the share of mortgage applications that were refinances reached nearly 60%, the highest since January 2022.”

How mortgage rates moved in the immediate aftermath of the FOMC meeting

As some observers in advance of the Fed meeting noted, it was not so much what the FOMC did, but what and how Chairman Jerome Powell said in his press conference after. The market responded to a cautious tone in Powell’s statements, Samir Dedhia, CEO of One Real Mortgage said in a commentary released in anticipation of the Freddie Mac survey.

“While the Fed did deliver the first rate cut in nine months, Powell emphasized that future moves will depend on how the data unfolds, especially around inflation and employment. In short, there’s no set path forward,” Dedhia warned. “This has created some uncertainty in markets, which could lead to small rate fluctuations in the short term.”

It’s not just refinance applications entering the market. Purchase activity also jumped as buyers regained confidence in the housing market, Dedhia said.

Dedhia noted that one product which doesn’t get talked about a lot is now seeing interest from consumers.

“Many are also exploring alternative terms like the 20-year fixed, which can strike a nice balance between savings and shorter payoff timelines,” said Dedhia. “For those still waiting, this may be the right time to re-engage with the market.”

The Fed’s move eventually “should put more downward pressure on mortgage rates, which is good news for borrowers in the coming weeks and months,” Mortgage Bankers Association President and CEO Bob Broeksmit said in Thursday morning commentary about the group’s Weekly Application Survey.

However, post-Fed commentary from Zillow indicated mortgage rates are not expected to fall much lower than their current levels, said Orphe Divounguy, one of its senior economists.

“Mortgage rates have moved lower and, if that sticks, the move could help revive some buyer competition,” Divounguy said.

The nation’s economic outlook will play a role in determining demand as well, and the current uncertainty may result in people staying put.

“Heading into the slower season of the housing cycle — when school, holidays and cooler weather dampen housing activity — the impact of any small changes to mortgage rates up or down is likely to be muted,” Divounguy warned.