Pennymac’s financial services unit built profits as it produced consistent consecutive-quarter loan volume and reduced servicing valuation-related losses in a market with lower rates, but it fell short of some consensus expectations.

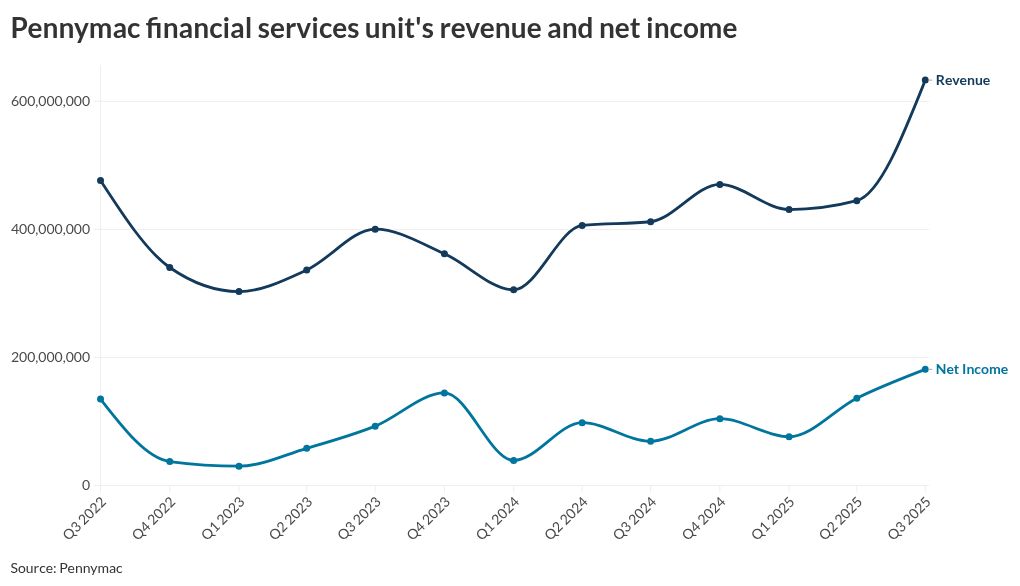

The $181.5 million in net income recorded under generally-accepted accounting principles topped the previous quarter’s $136.5 million and $69.4 million a year earlier, but didn’t quite reach the $200.9 million mark in Standard & Poor’s Capital IQ’s consensus estimates. Revenue jumped to $632.9 million from $411.8 million a year earlier and $444.7 million the previous quarter, outperforming a $573.5 million consensus mean.

“These results highlight the strategic advantage of our balanced business model,” CEO David Spector said in an earnings call, noting that strong hedging contributed to relatively strong servicing results.

What servicing and production numbers looked like

Highlights of the third quarter include a previously reported sale of $12 billion in servicing assets to mortgage real estate investment trust Annaly, with subservicing retained, he said.

“This transaction allowed us to monetize a mature asset with a weighted average coupon of 3.1% and projected go-forward returns at the lower end of our target range, freeing up capital to deploy into new higher coupon MSRs with greater recapture and return potential,” Spector said.

Reduced net valuation losses in servicing drove an increase in segment pretax income from $54.2 million the prior quarter and $3.3 million a year earlier to $157.4 million.

Hedge costs were “down significantly,” Chief Financial Officer Dan Perotti said.

While the company’s correspondent volume dominated, its direct-to-consumer share also climbed, and its broker business also is on the rise, Spector said, noting that lower rates could boost the DTC business with contributions from servicing portfolio recapture.

“Over the last 12 months, we have generated more than $100 billion in UPB of correspondent production, achieving an estimated market share of approximately 20% in the first nine months of 2025,” said Spector.

Spector said Pennymac is on track to grow broker channel share that’s just under 6% to a point above 10% by the end of 2026.

Originations totaled $36.5 billion during the quarter, down just 4% from peak homebuying season in the second quarter and up 15% from the same period a year earlier.

The production business’ revenue contribution was up but margins were down due to a shift in the mix of first- and second-lien loans, according to Perotti.

Production segment pretax income rose from $57.8 million in the second quarter to $122.9 million and inched down from $129.4 million from the third fiscal period of last year.

What analysts wanted to know about

Company executives said they have an uptick in borrower inquiries related to the impact of the government shutdown but have taken precautions to address such events based on historical experience, like ensuring they have at least nine months of Ginnie Mae commitment authority.

As one of the few large players in the publicly traded nonbank mortgage space, Pennymac also faced multiple questions from analysts about consolidation, but indicated it plans to stay the course as a company largely reliant on organic growth.

“While others may be focused on consolidation or other corporate activities, that allows us to continue to grow faster, and it allows us to do it profitably,” Spector said.

PMT is leaning into private-label securities

In a separate earnings call related to Pennymac’s mortgage real estate investment trust unit, which Spector also leads, he indicated the REIT has been ramping up its activity in the private label securities market. The two units have a complementary business relationship.

Perotti, who also fulfills a parallel role at PMT, said the company has been shifting more toward PLS and away from credit risk transfer securities, selling some during the period. The company’s PLS activity includes some securitization of conventional loans.

PMT reported $48 million in net income to common shareholders during the third quarter.