Better Home & Finance will likely be in the red for a while, but is gaining momentum with new partnerships and growing volume, its CEOVishal Garg said in a Thursday earnings call.

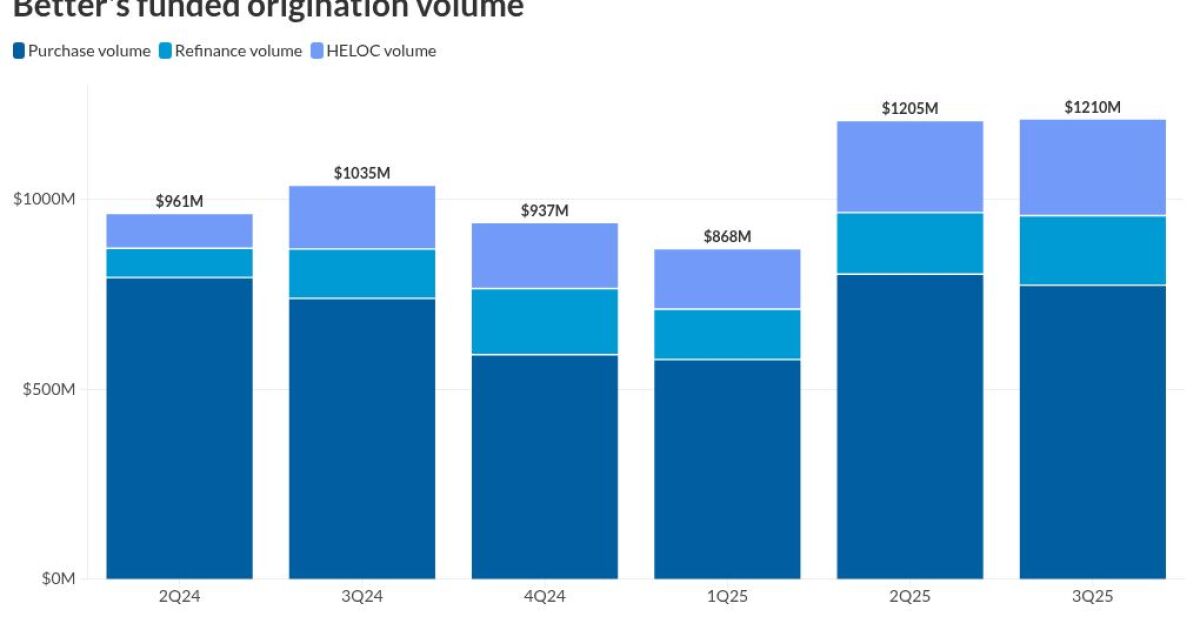

The New York City-based lender posted a $39.1 million net loss for the third quarter, and hasn’t gotten much closer to breaking even since going public in August 2023. While the company’s revenue also inched down from the second quarter, its production continued to trend up at $1.21 billion in the recent period.

Garg, the lone executive to speak in Thursday’s earnings call, further promoted Better’s artificial intelligence bona fides and discussed his firm’s growing partnership pipeline. He noted that “the largest incumbent solution” — Intercontinental Exchange, though he did not name the company — was going through an SDK change and forcing reintegrations with all of its partners.

“It’s been an interesting moment where a lot of people are very, very frustrated with the incumbent solutions that are out there and are looking for something new,” he said.

The lender’s partnerships include offering home equity loans with Finance of America, arrangements with two large servicers, and a new deal with an unnamed “top-five” non-bank originator to use Better’s Tinman platform with its direct-to-consumer and mortgage-servicing rights recapture teams. Garg suggested those partnerships will help Better reach $500 million of funding per month and beyond.

In touting AI tools, Better demoed its AI Mortgage Advisor, which advised Garg on a loan transaction the CEO compared to being in a Zoom call with an expert. Garg also described how no underwriter at Better is allowed to decline a loan without checking with its AI voice assistant Betsy, to determine alternatives to restructure the loan, a process the CEO said was a first in the industry.

Inside Better’s financial numbers

The lender broke $1 billion of origination volume for the second consecutive period, with increased home equity line of credit and refinance volume adding to slightly lower purchase volume in the third quarter.

The company maintained its projection to reach positive adjusted EBITDA by the end of the third quarter of 2026. While its net income slipped from a $36.2 million net loss in the second quarter, it was a step up from a $54.2 million loss last summer. On an adjusted basis, the third quarter net loss was $28.4 million.

Garg has frequently mentioned Better’s lower costs to originate, and said its contribution margin per fund has risen from $500 in the last third quarter to $1,772 this year. The company’s customer acquisition cost was over $3,000 per loan, as Better is pre-approving many consumers that may not close a loan for up to 18 months.

“In the last rate cycle, when rates were coming down, our CAC on a refi was $1,000 a loan,” said Garg. “There is a lot of positive convexity in the CAC as the rate environment changes.”

Better’s stock was trading at around $55 per share midday Thursday, down nearly 7% following the earnings figures. The lender’s stock had surged in September and October to upwards of $86 per share, after a hedge fund manager posted to social media about the company, describing it as the “Shopify” of mortgages.