Independent mortgage bankers reported a second consecutive quarter of profits on their loan production, helped by the September rate drop and surge in application volume, the Mortgage Bankers Association said.

Between originations and servicing income, roughly 85% of the 325 companies which participated in the Quarterly Mortgage Bankers Performance Report were profitable.

“After a series of volatile quarters since 2021, mortgage companies delivered healthier results in the third quarter,” said Marina Walsh, the MBA’s vice president of industry analysis, in a press release. “While third-quarter closed loan volume was relatively flat, and per-loan production expenses rose slightly compared to the second quarter, the increase in recorded production revenue drove profits higher in the third quarter.”

Contributors to third quarter profitability

After 8 consecutive quarters of losses and 10 out of 12 between the second quarter of 2022 and the first quarter this year, IMBs have made money on their originations four out of the last six three month periods.

The additional September application and rate lock volume was recognized as income in the third quarter by mortgage lenders. UWM Holdings, for example, attributed the September rate drop for its strong production quarter since 2021.

But Walsh added that the September rate locks, minus any pipeline fall out, will be reflected as closed loan volume in the current period, along with any mark-to-market adjustments which will impact earnings.

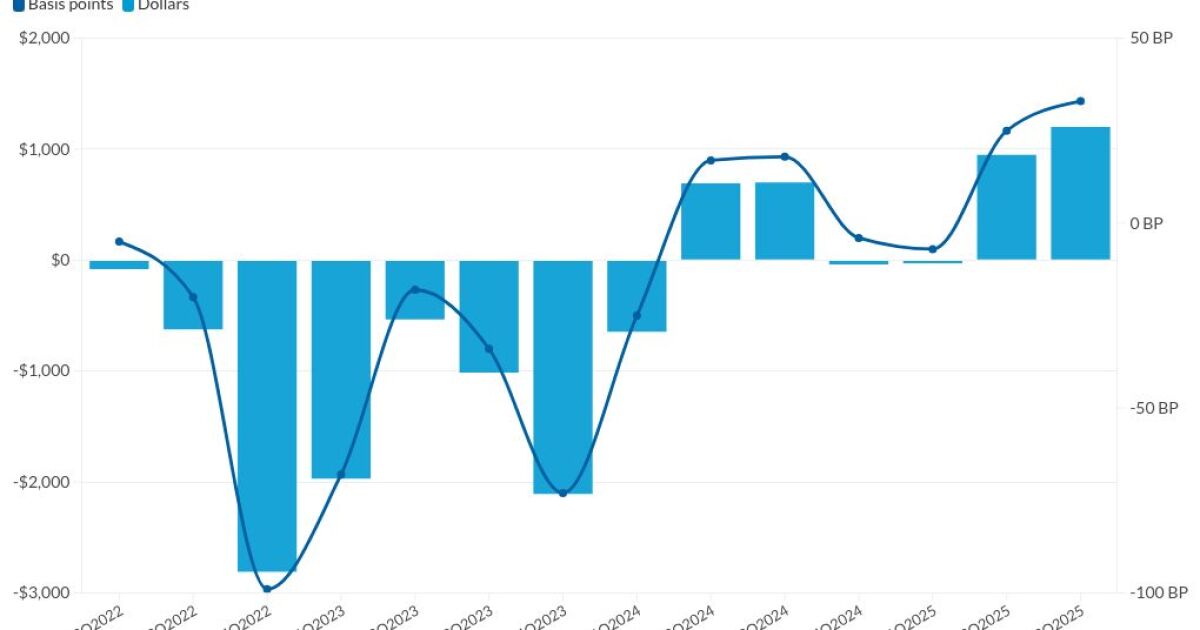

How much did lenders make per-loan in 3Q25

IMBs made $1,201 per loan originated, up from $950 in the second quarter and $701 one year ago.

Measured in basis points, the average pretax production profit in the third quarter was 33 basis points, a gain of 8 basis points from three months prior, when it was 25 basis points and almost double the year ago’s 18 basis points. This was still below the long-term average of 40 basis points.

Total production revenue, inclusive of fee income, net secondary marketing income and warehouse spread, was 359 basis points for the most recent period. This was up from 346 basis points in the second quarter and 341 basis points in the third quarter of 2024. On a per-loan basis, production revenues increased to $12,310 per loan in the third quarter, up from $11,914 per loan in the second quarter.

But expenses, which includes commissions and compensation among other production-related items, rose quarter-to-quarter to 326 basis points from 321 basis points. For the third quarter last year, this was 323 basis points.

Measured in dollars, this was $11,109 per loan in the third quarter, versus $10,965 for the second quarter and $10,716 one year ago.

Servicing earnings in the 3Q

Servicing net financial income fell slightly from the second quarter, to $29 per loan from $30. For the year ago period, servicers lost $25 per loan.

Segment operating income, which among other things removes mortgage servicing rights amortization, changes in MSR values and any gains or losses from bulk sales, was $92 per loan in the third quarter. This compared with $90 in the second quarter and $93 per loan for the third quarter of 2024.