Mortgage delinquency levels rise on softer FHA performance

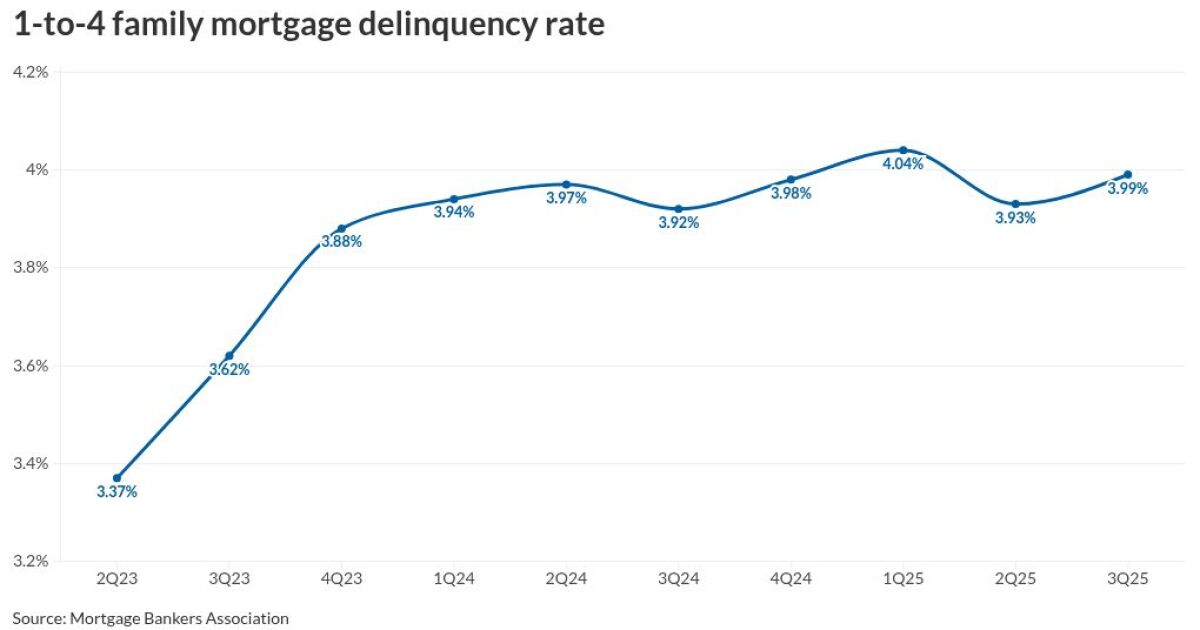

unitedbrokersinc_m7cmpd2025-11-14T22:22:49+00:00Mortgage delinquencies increased by 6 basis points from the second quarter, as the performance of Federal Housing Administration-insurance loans declined, the Mortgage Bankers Association National Delinquency Survey found.Recently, ICE Mortgage Technology executive Andy Walden said FHA loan performance trends were a yellow flag for the mortgage industry.Delinquent mortgages made up 3.99% of all outstanding loans when seasonally adjusted in the third quarter, up from 3.93% in the second quarter and 3.92% one year prior.This is the second highest delinquency rate since an all-time low was recorded in the second quarter of 2023. The 3.37% posted for that period was 62 basis points below the most recent data.While the foreclosure start rate was still rather low at 0.20%, it was 3 basis points higher than the previous quarter. The share of loans in the foreclosure process was 50 basis points, up 2 basis points from the second quarter and 5 basis points over the third quarter of 2024."Since this time last year, the FHA seriously delinquent rate — which includes 90-plus day delinquencies and loans in foreclosure — increased by almost 50 basis points," Marina Walsh, the MBA's vice president of industry analysis, said in a press release. "In contrast, the conventional and Veterans Affairs seriously delinquent rates remained relatively flat."The period's results were not affected by the government shutdown or the end of pandemic related FHA loss mitigation programs, although those are likely to affect delinquency activity going forward, Walsh said.FHA borrowers are more affected by a softer labor market, other personal debt obligations, along with increases in taxes, homeowners insurance premiums and other fees, she said."Additionally, home price declines in some parts of the country may lessen the ability to sell or refinance," Walsh warned. It is the growth in values which provides a level of protection for distressed borrowers in recent years.While the seasonally adjusted serious delinquent borrower rate (90 or more days) of 111 basis points was unchanged from the second quarter, the shorter term buckets were higher.For borrowers who are between 30 and 59 days late on their scheduled payment, the rate increased 2 basis points to 2.12%, while between 60 and 89 days rose 4 basis points to 76 basis points.FHA mortgage rates were 21 basis points higher to 10.78% versus the second quarter, while year-over-year they are 32 basis points more.Conventional loans overall late payments rose 2 basis points to 2.62% from three months prior but reported a 1 basis point drop versus the third quarter of 2024.While the overall VA rate rose 18 basis points to 4.5% between the second and third quarters, it dropped 8 basis points from one year ago.The seriously delinquent rate decreased 2 basis points for conventional loans, increased 30 basis points for FHA loans, and decreased by 1 basis point for VA loans quarter-to-quarter.Versus the third quarter 2024, this fell by 4 basis points for conventional loans, but rose 47 basis points for FHA loans and 4 basis points for VA loans.In recent reports from bond rating agencies KBRA and Fitch, both are expecting delinquency rates to increase next year.