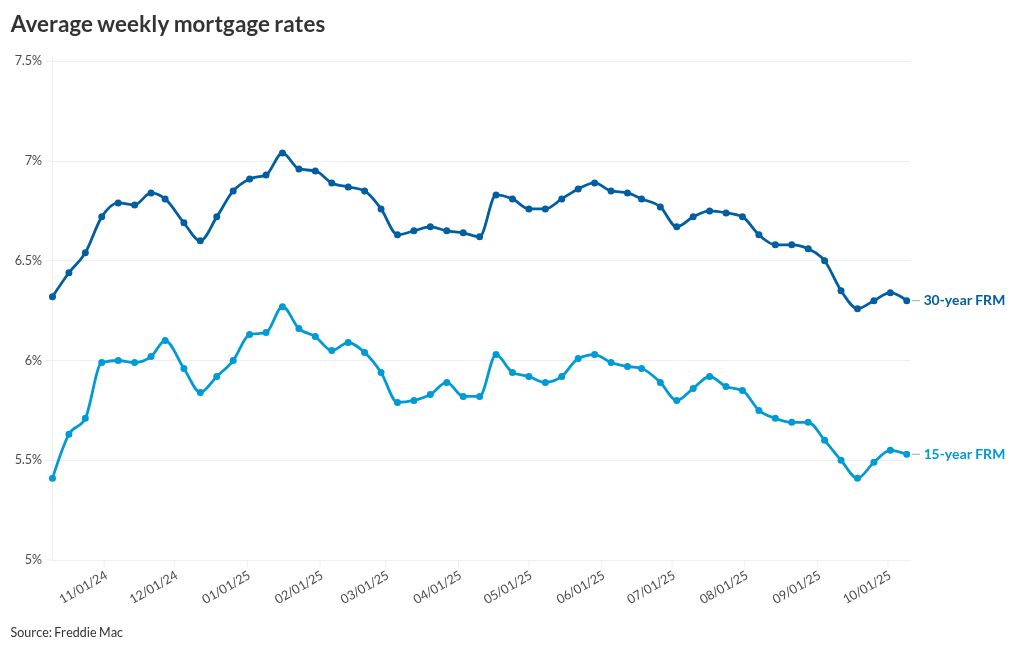

The federal government shutdown and the resulting delay in the monthly employment report was the catalyst for the small movement in mortgage rates this past week.This data "would have been a key market mover for mortgage rates, offering insight into how much the Federal Reserve might adjust monetary policy in response to a cooling labor market," said Kara Ng, senior economist at Zillow Home Loans in a Wednesday evening statement."However, with the government shutdown delaying major economic data releases, markets are relying on alternative data sources, which may have contributed to the narrow range for mortgage rate movements over the last week," Ng explained.Where rates are today according to Freddie MacThe 30-year fixed rate mortgage dropped 4 basis points this week to 6.3%, compared with 6.34% for Oct. 2, the Freddie Mac Primary Mortgage Market Survey found. For this time last year, the 30-year was at 6.32%. The 15-year FRM averaged 5.53% for Oct. 9, a 2 basis point decline, from last week when it was at 5.55%. A year ago, it was at 5.41%.This marks the first time in three weeks, or since after the September Federal Open Market Committee meeting where short-term rates were reduced, that this mortgage rate indicator has declined."Over the last few weeks, mortgage rates have settled in at their lowest level in about a year," said Sam Khater, chief economist at Freddie Mac, in a press release. "There is growing evidence that homebuyers are digesting these lower rates and gradually are willing to move forward with buying a home, which is boosting purchase activity."A year ago, mortgage rates were on the rise following a different September FOMC cut, on their way to respective 52-week highs in January (in spite of a brief downward blip in December).How other indicators moved this weekAlthough the 10-year Treasury yield, one of the benchmarks used to price fixed-rate mortgages, was higher compared with one week ago, other indicators also noted the sideways movement in rates.As of 11 a.m. on Thursday, the 10-year was at 4.14%, up 5 basis points from its Oct. 2 close of 4.09%.But Lender Price data on the National Mortgage News website had the 30-year fixed at just under 6.43%, down 1 basis point from seven days earlier.Zillow's rate tracker put the 30-year FRM at 6.46% at that time, up 1 basis point from Wednesday but down 3 basis points from last week's average rate of 6.49%.Data from the Optimal Blue product and pricing engine had the conforming 30-year FRM at 6.277% for Wednesday, up from 6.262% seven days earlier and 6.253% for Oct. 2.Why lower rates may not be driving home salesNew listings of homes for sale rose 2.3% annually over a four-week period ended Oct. 5, which included a period when the Freddie Mac PMMS fell to 6.26%, a Redfin report released early Thursday said.However, buyers aren't acting, it said, as pending sales fell 1.3% from a year ago.In speaking with its agents, Redfin, now owned by Rocket, said they are seeing house hunters waiting for mortgage rates to drop even further, especially given that prices are remaining high; the median sales price rose 2.1% year-over-year, the biggest increase in six months.However, even though most of the rates tracked in the Mortgage Bankers Association's Weekly Application Survey released yesterday, new loan submissions were down.This is a sign that rates aren't low enough, said Bob Broeksmit, MBA president and CEO, in a Thursday morning comment."Rates on 5/1 adjustable rate mortgages are averaging almost a percentage point below 30-year fixed rates, which explains why the ARM share of applications increased to nearly 10%, and suggests that some borrowers are exploring lower-rate alternatives."However, in the view of Samir Dedhia, CEO of One Real Mortgage, which is affiliated with a real estate brokerage firm, the latest mortgage rate drops are making a meaningful impact on the housing market."Buyers who had paused their home search due to affordability concerns are showing renewed interest, and the data reflects it," Dedhia said. "We're seeing a consistent uptick in purchase activity, as more consumers grow confident that this lower-rate window may last longer than expected."Will the Fed cut rates further, and if so, whenThe FOMC is itching to cut short-term rates further, said Melissa Cohn, regional vice president of William Raveis Mortgage, referring to the recent release of the September meeting minutes in an emailed comment before the Freddie Mac release.It doesn't mean, however, that a rate cut is imminent."Fed forecasts, like any other forecasts, are cloudy at best," Cohn said. "We have seen in the past that the expectations of Fed members change, and economic and inflationary conditions change."So those looking for large scale mortgage rate changes should temper their expectations. Plus, the shutdown is affecting the Fed's data gathering and digestion."The Fed will have a tougher time this month when they meet, as the government shutdown has greatly reduced the data that is being released in order to guide their latest decision, especially as it relates to the employment numbers," Cohn noted.