Shutdown cuts off flood insurance program during storm season

unitedbrokersinc_m7cmpd2025-10-09T20:23:11+00:00A lapse in the National Flood Insurance Program because of the US government shutdown threatens to snarl home sales in the nation's riskiest floodplains and leave some homeowners without coverage in the middle of hurricane season.Without reauthorization, the program – which counts more than 4.7 million policies providing more than $1.3 trillion in coverage – cannot issue new policies or renew expiring ones. In areas that require flood insurance to close a loan, that's a problem. READ MORE: Shutdown hampers rates, rural, HECM and niche condo loansAs the government shutdown continues for a second week, with no sign of breakthrough on the horizon, the coverage gap is poised to keep widening. As many as 1,400 sales per day could stall or fall through without flood insurance, the National Association of Realtors estimates. "Each day that passes during the shutdown, potential real-life impacts will be felt in America's housing market, which accounts for nearly 20% of the US economy," said Shannon McGahn, the association's executive vice president and chief advocacy officer. Transactions are more likely to be delayed than scrapped outright, according to industry experts, as lenders relax requirements during the gap period. "It's not so much deals are being canceled right away, but as this goes on longer and longer it's going to be more people in limbo," said Daryl Fairweather, chief economist at Redfin. READ MORE: Shutdown tests lenders' plans to keep loans movingMore people will either go without flood insurance or be unsure of whether they are covered, according to David Maurstad, former senior executive of the program. "If there was a hurricane and you have a tremendous number of properties that are damaged, the confusion and the angst and anxiety people would have just gets ratcheted up during a time when they're already having the worst day of their lives," he said.The situation could easily have been avoided, he added. "It's not like the entire budget: It's one program, and we knew what the deadline was." Senator John Kennedy, a Republican from Louisiana, has introduced two bills to reauthorize and extend the program apart from the bigger shutdown spending clash. So far, though, Republicans have maintained a united front in pressuring Democrats to pass a larger measure known as a continuing resolution, which would fund the government and extend NFIP authorization into next month – without breaking off individual programs to fund on their own."It's expired thanks to the Democrats," Kennedy said. "It's stupid."READ MORE: Agencies issue shutdown-related guidance for lendersRepublican and Democratic congressional leaders continued to blame one another for the shutdown, sticking to their their talking points and stances as the impasse entered its ninth day on Thursday. Senator Rick Scott, a Florida Republican, whose state leads the nation in NFIP coverage, said the lapse "could have a pretty big impact on home sales in Florida" and urged Democrats to pass the continuing resolution.The program applies to just 4% of residential properties – but those are arguably some of the nation's riskiest. Floods are the most common natural disaster in the US, and they're not covered by most homeowners' insurance policies. Some of the fastest-growing American cities are also in low-lying zones on the coast. Flood losses in the US have been climbing as climate change loads the atmosphere with more moisture and amps up the rainfall associated with hurricanes and thunderstorms. Such storms caused more than $125 billion in damage in 2024 alone, according to federal data, largely tied to catastrophic rains from Hurricane Helene.Just one inch of water can cost tens of thousands of dollars in damage. And 1,400 stalled or thwarted home sales a day adds up."It's hard to believe how many homes we're talking about," said Neil Alldredge, president and chief executive officer of the National Association of Mutual Insurance Companies, which represents six of the 10 largest property and casualty insurers in the US."If you're living near a river or stream, you're probably going to flood at some point in time," Alldredge said. "And you probably would have the potential to flood at a higher level than you've seen before."Fannie Mae and Freddie Mac, the government-controlled mortgage financiers, will accept evidence that an eventual NFIP policy is in the works, including a completed insurance application and proof that the premium has been paid or that the seller's policy has been transferred to the buyer. Sellers and loan servicers are required to follow up once the program is renewed to provide final evidence of coverage.With its subsidized premiums and contested risk maps, the flood insurance program has long been criticized for doing too little to discourage people from living in risky areas. But according to federal estimates, NFIP has still managed to save the US about $1.7 billion a year in avoided flood losses.That's one reason Congress has gotten into the habit of repeatedly extending NFIP on a short-term basis while seeking a long-term solution for the viability of the program.A growing number of private insurers and intermediaries – including Neptune Insurance Holdings Inc., which raised $368 million in a US initial public offering last month – are offering flood coverage. But they still represent just a sliver of the market compared with NFIP. And premiums on the private market can be considerably higher than NFIP's rates, driving up costs for aspiring homebuyers who need insurance to secure a mortgage for a pending sale."There might be private market solutions that are double or much more expensive," said Charlie Sidoti, executive director of the nonprofit insurance think tank InnSure. "That makes the economics of a deal undesirable or undoable."

Fed's Barr skeptical that inflation has been tamed

unitedbrokersinc_m7cmpd2025-10-09T19:23:13+00:00Key insight: Federal Reserve Gov. Michael Barr said in a speech Thursday that he fears the way tariff price increases are being passed on to consumers could result in an unmooring of inflation expectations, potentially leading to more inflation — and higher interest rates — down the road.Expert quote: "While, in principle, tariffs are a one-time increase in prices and should not sustainably raise inflation, that may not be the case if prices keep rising month after month and affect expectations." — Federal Reserve Gov. Michael Barr What's at stake: Barr's views come in contrast with other Fed officials' recent remarks, which focused on the risks to the labor market of maintaining higher interest rates for too long.Federal Reserve Gov. Michael Barr said he is worried that the persistently high inflation rate observed in recent months could lead to higher consumer expectations of inflation over the long run, a phenomenon that would likely necessitate higher interest rates to counter.Speaking at a conference at the Federal Reserve Bank of Minneapolis Thursday, Barr — who had served as the Fed's vice chair for supervision until February — said that the way that price increases due to new tariffs have been passed on to consumers to date has led to lower headline inflation rates than many economists expected earlier this year. Part of that, he said, is because many retailers built up stockpiles of imported materials in anticipation of the new tariffs and have been using a combination of those stockpiles and thinner profit margins to keep price increases at the port from hitting consumers on-shore."While the immediate effects of tariffs on inflation have been smaller than most economic forecasters had expected, the inventories built up in anticipation of the tariffs may have had a role in easing the immediate impact, as have compressed profit margins," Barr said. "While that is good news for inflation, the corresponding bad news is that firms will eventually run down those inventories and will only be able to compress margins for a while."The effect of this softening of the one-time inflationary blow is to stretch that price increase out over time, which has the potential to lead consumers to expect inflation to continue even after the tariff-induced price increases have been absorbed."Normalizing margins over time implies a gradual, but longer, upward trajectory for inflation, a pattern of price increases that I fear could convince many consumers that higher inflation is going to be more of a permanent phenomenon," Barr said. "While, in principle, tariffs are a one-time increase in prices and should not sustainably raise inflation, that may not be the case if prices keep rising month after month and affect expectations. At some point, businesses and consumers could start to make pricing, spending and wage decisions based on their belief in higher future inflation, thereby driving a cycle of persistence."Barr's remarks come in contrast with those of other Fed officials in recent days. Fed Vice Chair for Supervision Michelle Bowman said in a speech last month that the labor market is at risk of "serious deterioration" and that further weakening of the jobs numbers could spur the central bank to cut interest rates "at a faster pace and to a larger degree going forward."Bowman's remarks echoed those of recently-confirmed Fed Gov. Stephen Miran, who last month argued that there has been a paradigmatic shift in the economy that the central bank has not sufficiently considered. Higher rates of immigration and fiscal policy observed in the Biden administration resulted in a higher neutral rate — that is, the interest rate that is neither accommodative nor restrictive to the economy — than central bankers appreciated. That miscalibration is now being thrown into reverse, Miran argued, because the immigration and fiscal policies enacted by the Trump administration are pushing the neutral rate lower than the Fed consensus thinks, rendering the current Fed rate considerably more restrictive than Fed officials think. "In my view, insufficiently accounting for the strong downward pressure on the neutral rate resulting from changes in border and fiscal policies is leading some to believe policy is less restrictive than it actually is," Miran said.Barr acknowledged that the gradual rollout of price increases may not necessarily lead to long-term inflation. The softening labor market could result in downward pressure on wages, which could at least partially counteract inflationary pressures, Barr said, noting that the gradual increase in prices has not spurred supply chain dislocations and that consumer inflation expectations to date have been well anchored. But he also noted that the labor market may not be in as perilous a position as it may seem. The delayed release of the Bureau of Labor Statistics' September jobs report means that Fed officials don't have the most reliable data on labor market deterioration, though private metrics suggest a modest contraction in the number of jobs in the economy last month. Even so, simultaneous reductions in labor supply stemming from the administration's immigration policies have blunted the reduction in labor demand, meaning that small rates of job creation may be healthier than they might otherwise appear. "With a reduced supply of labor, what constitutes a healthy growth rate for employment would be smaller," Barr said. "One can see that slower labor supply growth has been an important factor in the weaker job creation, because over the period that job gains have slowed significantly, the unemployment rate has only edged up to 4.3%, a level typically associated with a sound labor market."The rough balance of the labor market, however, should not be confused with stability, Barr said, noting that the labor market is still susceptible to destabilizing outside shocks that could throw the market out of balance. Workers' confidence in their ability to find another job if they lost their current one is the lowest it has been in more than a decade, Barr said, and unemployment rates for black and young workers — populations that often serve as the leading edge of labor dislocations — have been edging up in recent months. All of that paints a picture of a roughly balanced but highly delicate labor market, Barr said. "With job growth near zero for the past several months, the labor market could decline precipitously if the economy is hit with another shock," Barr said. "With the easing in output growth and the likelihood of tariffs and labor supply weighing on the economy in the months ahead, we need to be prepared for the possibility that the softening in the labor market will become something worse, especially if there is a further adverse shock to demand."Looking toward the Fed's near-term monetary policy stance, Barr said he supported the Federal Open Market Committee's decision last month to reduce the federal funds rate by 25 basis points, which he said sensibly brought the prevailing rate "a bit closer toward neutral." Since that time, Barr said, inflation has shown to remain persistently higher than the Fed's 2% target rate but consumer spending has shown to be more robust than expected. In the absence of an overpowering development favoring one side of the Fed's dual mandate over the other, the central bank should remain cautious in its future decisions, Barr said. "I believe that … the FOMC should be cautious about adjusting policy so that we can gather further data, update our forecasts, and better assess the balance of risks," Barr said. "If we see inflation moving further away from our target, then it may be necessary to keep policy at least modestly restrictive for longer. If we see heightened risks in the labor market, then we may need to move more quickly to ease policy. The FOMC can, and I believe would, act forcefully to stabilize the economy if necessary."

Aidium rebrands as Lendware after summer turmoil

unitedbrokersinc_m7cmpd2025-10-09T18:22:44+00:00Following a turbulent summer, customer-relationship management platform Aidium has relaunched as Lendware, with new leadership installed and existing operations overhauled. New York-based technology firm Lendware announced this week it had acquired assets belonging to the CRM platform, subsequently rebranding it to the new parent's name. The company also appointed longtime technology executive Josh Glantz as CEO and named Mike Wylie interim chief financial officer. "Aidium has long been considered the easiest platform for loan officers to adopt. As part of Lendware, we are setting the bar even higher with our newly formed leadership and visionary product strategy," Glantz said in a press release. Glantz's previous technology leadership roles include corporate executive positions at software platforms serving business segments from nonprofits to restaurant and cannabis industries. Terms of the deal were not disclosed. The brand refresh and executive moves reflect "a renewed commitment to support independent mortgage brokers," and adoption of "a forward-thinking" artificial intelligence strategy, Lendware said. The CRM already claims lending businesses, such as Neo Home Loans and First Option Mortgage as client partners. Among the company's future plans are the introduction of features created around an AI-backed user interface and engagement suite and development of new artificial intelligence tools, it said. "As interest rates are dropping, we will help loan officers and mortgage brokers take advantage of market trends with our software and strategic guidance," Glantz added. What led to the changes at AidiumThe latest developments at Aidium come after several months of controversy and personnel changes at the technology platform, according to recent reporting by The Mortgage Scoop. While admired for its technology, Aidium, whose previous headquarters were located in Boulder, Colorado, was dogged with reports of financial mismanagement marked by lavish marketing spending by leadership at the same time staff members were terminated. Aidium's former President Dan Bos stepped down from the role in May. Meanwhile, Peakspan Capital, Aidium's primary investor, removed co-founder Spencer Dusebout from his role as CEO. As recently as last year, Peakspan led a $19 million Series A raise for the mortgage CRM platform. Dusebout remains with Aidium as chief product officer. He co-founded the company originally known as Daily AI in 2019, before it was renamed to Aidium in 2023. Within the mortgage CRM space, the platform's primary competitors include Total Expert, Shape Software and Insellerate, with many lenders also making use of general-use platforms, such as Salesforce and Hubspot.

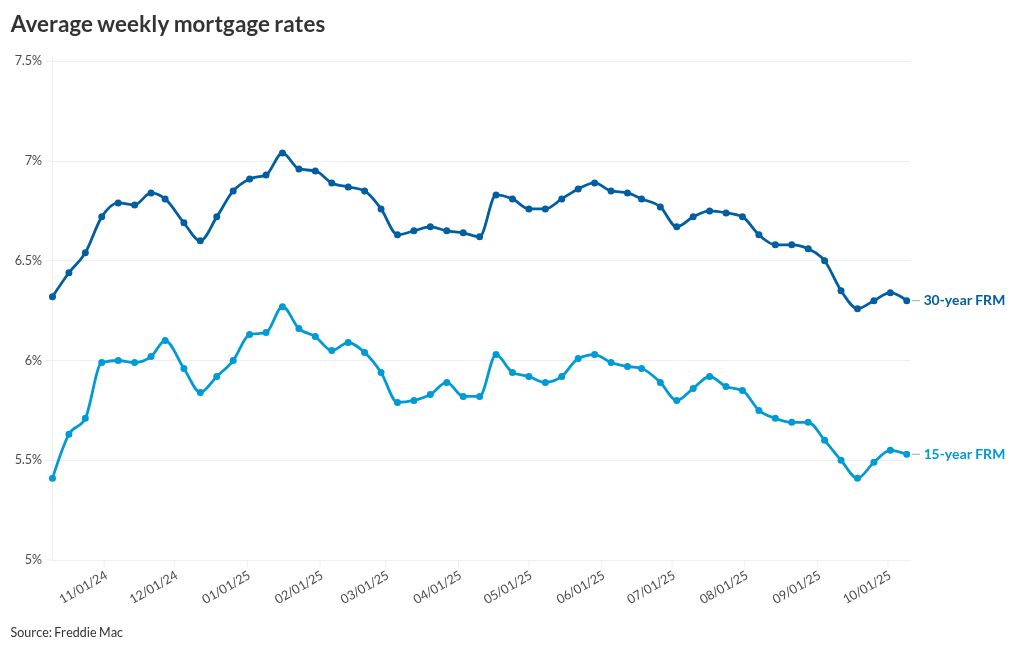

How mortgage rate have been affected by federal shutdown

unitedbrokersinc_m7cmpd2025-10-09T17:23:05+00:00The federal government shutdown and the resulting delay in the monthly employment report was the catalyst for the small movement in mortgage rates this past week.This data "would have been a key market mover for mortgage rates, offering insight into how much the Federal Reserve might adjust monetary policy in response to a cooling labor market," said Kara Ng, senior economist at Zillow Home Loans in a Wednesday evening statement."However, with the government shutdown delaying major economic data releases, markets are relying on alternative data sources, which may have contributed to the narrow range for mortgage rate movements over the last week," Ng explained.Where rates are today according to Freddie MacThe 30-year fixed rate mortgage dropped 4 basis points this week to 6.3%, compared with 6.34% for Oct. 2, the Freddie Mac Primary Mortgage Market Survey found. For this time last year, the 30-year was at 6.32%. The 15-year FRM averaged 5.53% for Oct. 9, a 2 basis point decline, from last week when it was at 5.55%. A year ago, it was at 5.41%.This marks the first time in three weeks, or since after the September Federal Open Market Committee meeting where short-term rates were reduced, that this mortgage rate indicator has declined."Over the last few weeks, mortgage rates have settled in at their lowest level in about a year," said Sam Khater, chief economist at Freddie Mac, in a press release. "There is growing evidence that homebuyers are digesting these lower rates and gradually are willing to move forward with buying a home, which is boosting purchase activity."A year ago, mortgage rates were on the rise following a different September FOMC cut, on their way to respective 52-week highs in January (in spite of a brief downward blip in December).How other indicators moved this weekAlthough the 10-year Treasury yield, one of the benchmarks used to price fixed-rate mortgages, was higher compared with one week ago, other indicators also noted the sideways movement in rates.As of 11 a.m. on Thursday, the 10-year was at 4.14%, up 5 basis points from its Oct. 2 close of 4.09%.But Lender Price data on the National Mortgage News website had the 30-year fixed at just under 6.43%, down 1 basis point from seven days earlier.Zillow's rate tracker put the 30-year FRM at 6.46% at that time, up 1 basis point from Wednesday but down 3 basis points from last week's average rate of 6.49%.Data from the Optimal Blue product and pricing engine had the conforming 30-year FRM at 6.277% for Wednesday, up from 6.262% seven days earlier and 6.253% for Oct. 2.Why lower rates may not be driving home salesNew listings of homes for sale rose 2.3% annually over a four-week period ended Oct. 5, which included a period when the Freddie Mac PMMS fell to 6.26%, a Redfin report released early Thursday said.However, buyers aren't acting, it said, as pending sales fell 1.3% from a year ago.In speaking with its agents, Redfin, now owned by Rocket, said they are seeing house hunters waiting for mortgage rates to drop even further, especially given that prices are remaining high; the median sales price rose 2.1% year-over-year, the biggest increase in six months.However, even though most of the rates tracked in the Mortgage Bankers Association's Weekly Application Survey released yesterday, new loan submissions were down.This is a sign that rates aren't low enough, said Bob Broeksmit, MBA president and CEO, in a Thursday morning comment."Rates on 5/1 adjustable rate mortgages are averaging almost a percentage point below 30-year fixed rates, which explains why the ARM share of applications increased to nearly 10%, and suggests that some borrowers are exploring lower-rate alternatives."However, in the view of Samir Dedhia, CEO of One Real Mortgage, which is affiliated with a real estate brokerage firm, the latest mortgage rate drops are making a meaningful impact on the housing market."Buyers who had paused their home search due to affordability concerns are showing renewed interest, and the data reflects it," Dedhia said. "We're seeing a consistent uptick in purchase activity, as more consumers grow confident that this lower-rate window may last longer than expected."Will the Fed cut rates further, and if so, whenThe FOMC is itching to cut short-term rates further, said Melissa Cohn, regional vice president of William Raveis Mortgage, referring to the recent release of the September meeting minutes in an emailed comment before the Freddie Mac release.It doesn't mean, however, that a rate cut is imminent."Fed forecasts, like any other forecasts, are cloudy at best," Cohn said. "We have seen in the past that the expectations of Fed members change, and economic and inflationary conditions change."So those looking for large scale mortgage rate changes should temper their expectations. Plus, the shutdown is affecting the Fed's data gathering and digestion."The Fed will have a tougher time this month when they meet, as the government shutdown has greatly reduced the data that is being released in order to guide their latest decision, especially as it relates to the employment numbers," Cohn noted.

Lagging builder stocks face new worry from Bill Pulte's ire

unitedbrokersinc_m7cmpd2025-10-09T15:23:32+00:00President Donald Trump and Federal Housing Finance Agency Director Bill Pulte are fueling a deeper selloff in already struggling homebuilder stocks.A series of social media posts, from the US president over the weekend and then from the FHFA director and real estate scion Pulte on Wednesday, are helping put an S&P gauge of builders on track for a four-day losing streak. The group has lost more than 9% over the period, the worst such selloff since Trump's tariff announcement in early April.READ MORE: Pulte hints at how Fannie, Freddie may spur builder activityHomebuilders are trailing the broader market this year, beset by rising inventories, stretched consumers and a fresh wave of levies on materials like lumber and kitchen cabinets. Now, with the Trump administration blaming the builders for the housing affordability crisis the selloff has gone from bad to worse. The group has tumbled about 19% in the past 12 months, badly lagging the S&P 500's AI-fueled 16% rally. The latest losses followed a Sunday post from Trump who said homebuilders were sitting on millions of empty lots, and "they have to start building Homes." Pulte followed with his own critique."When I was young and growing up in the Pulte Homes business, Big Homebuilders had less than 10% of the market. Today, that number is 50% and some say 60%. With great market share comes great responsibility," the grandson of the founder of PulteGroup Inc. wrote in a post on X Wednesday morning. "I encourage all builders to realize this, and sooner rather than later." For loans sold to Fannie Mae and Freddie Mac, the mortgage giants will be asking "relevant market participants to disclose Big Builder loans," Pulte added. READ MORE: More home sales fall through as buyers gain leverageTo Neil Dutta, Renaissance Macro Research's head of economics, the call to build more houses would only hurt builders, given the unsold inventory they are sitting on, while increasing industry concentration."Bill Pulte has shifted his ire to the public homebuilders," Dutta wrote in a note Wednesday. "Bullying builders to make homes when margins are eroding and prices are already falling is not exactly the best combination for homebuilders."The hardest hit stocks in the sector this year include LGI Homes Inc., Champion Homes Inc. and Century Communities Inc., which are all down 20% or more. Lennar Corp., the second-biggest index member, is down 10%, while PulteGroup, one of the largest homebuilders in the US, has advanced 12%.On Thursday, PulteGroup and Toll Brothers Inc. fell more than 3% each after CFRA analyst Ana Garcia downgraded the pair, calling PulteGroup "overvalued." She also flagged a "decelerating labor market and declining consumer confidence as consumers deal with economic uncertainty." Regarding Toll Brothers, she said the company's advantage with wealthier customers "may weaken as more expensive existing homes come on the resale market, giving luxury buyers more options."READ MORE: Trump calls on Fannie Mae, Freddie Mac to boost homebuilders The problems facing the industry are fairly well known. Last month, Bloomberg Intelligence analyst Drew Reading wrote that US homebuilders were dealing with growing margin pressure as rising inventory drives price cuts in key markets. He noted new-home supply had spiked, with for-sale inventory at the highest since 2007. Last week, Reading estimated that tariffs on softwood lumber and kitchen and bath cabinets could add more than $10,000 to the cost of a new home. Earlier this week, Evercore ISI analyst Stephen Kim downgraded builder names on depressed home-buying sentiment.

Pulte hints at how Fannie, Freddie may spur builder activity

unitedbrokersinc_m7cmpd2025-10-09T13:23:25+00:00Bill Pulte, the head of the oversight agency for Fannie Mae and Freddie Mac, signaled that he will be taking steps to follow up on President Trump's call for them to put a new focus on home construction companies.One step will involve tracking megabuilders' business, Federal Housing Finance Agency Director Pulte indicated in an X post. Pulte, who also refers to the FHFA as US Federal Housing, and Trump both frequently used social media posts to provide early hints at policy intentions. Fannie and Freddie "will be asking relevant market participants to disclose big builder loans they are selling," Pulte said, noting that the move will be made in order "to continue, and to strengthen, the safety and soundness of the market."Trump's Truth Social messaging suggests he wants the two government-sponsored enterprises to boost builders business while also indicating he holds them responsible for the high price of homes, which he wants to see lowered.Pulte told Builders Daily that FHFA wants to find ways to "incentivize the right things and disincentivize the wrong things" to that end."We're still evaluating the specific measures," he said.While Freddie and Fannie don't directly build homes themselves, they do buy and securitize loans from builders' lending units and other mortgages that fund new home construction. All of the top 10 builders have lending affiliates of some kind.Pulte said in yet another X post his examination of Fannie's builder data shows the GSE has bought well over $20 billion in loans from top three players in the space.Pulte has been watching big builders' growing influenceIn another X post, Pulte flagged the growth in large players' influence compared to what he saw during his youth as part of a homebuilding family, He estimated "big builders" have gone from representing 10% of the market at that time to as high as 50-60% currently, with some variation in data sources on that point."With great market share comes great responsibility. I encourage all builders to realize this, and sooner rather than later," he said.The numbers in Pulte's estimate may be on the higher end but are aligned with the trend seen in a recent National Association of Home Builders analysis.That NAHB analysis of data from Zonda, an information provider that publishes Builder magazine, finds the top 10's share based on closings has increased from around 8.7% in 1989 to 44.7% last year, marking a record high.DR Horton and Lennar dominate at 13.6% and 11.7%, followed by the FHFA director's namesake PulteGroup at 4.6%. Rounding out the top 10 are: NVR, 3.3%; Meritage, 2.3%; SH Residential Holdings, 2.2%; KB Home, 2.1%; Taylor Morrison, 1.9%; Century Communities and Toll Brothers, both 1.6%.During his confirmation hearing, the FHFA director said he sold all his stock in PulteGroup "a few months" prior to the event. He also said he severed ties with the company in line with information in financial disclosures and ethics agreements related to taking his position at the agency.(President Trump also took steps to distance himself from ties he had to Truth Social before taking office, including transferring a $4 billion stake in its parent company to a trust, according to a regulatory filing Politico reported on late last year.)Tri Pointe Homes exec moves into a key position at FanniePulte indicated in another post that he anticipates one of the newer GSE board members at Freddie with builder ties, Brandon Hamara, will be taking a full-time post at Fannie and playing a role in efforts to further President Trump's aims for home construction.Hamara, the vice president of land acquisition at Tri Pointe Homes, will move over to a position as senior vice president and head of operations for Fannie's single- and multifamily division with an estimated start date in November, according to a Securities and Exchange Commission filing.His target compensation is $1.9 million but he must fulfill several conditions to receive it in increments over time, according to Fannie's filing. Hamara has resigned from Freddie Mac's board, a securities filing by that enterprise shows.How the GSEs could may be able fund more constructionMany concepts that have been floated for builder lending could get new life in the wake of Trump and Pulte's new focus on construction such as a GSE equivalent of a program the US Department of Agriculture has pioneered which allows quicker securitization of one-time close construction loans.There has been a push in the industry to immediately allow Fannie and Freddie to purchase OTC construction-to-permanent loans, said Sean Faries, CEO of Land Gorilla, a technology provider in the space.The move would benefit mortgage lenders that currently must hold the construction loans on their warehouse lines of credit until the home gets built, because they would be able to free up credit to extend more financing more quickly."When you have a securitizable type of loan program, a mortgage bank doesn't have to tie up all their warehouse capacity for 12 months," Faries said.

Optimal Blue suit alleges cartel-style mortgage fixing

unitedbrokersinc_m7cmpd2025-10-09T10:23:02+00:00A new class action lawsuit accuses Optimal Blue and 26 lenders of price fixing and inflating mortgage costs for millions of consumers. The complaint says the industry's biggest players violated antitrust law in sharing sensitive home loan data with competitors and subsequently raising rate spreads. Borrowers specifically scrutinize Optimal Blue's competitive analytics and Competitive Data License tools rolled out in 2019. The lawsuit was first reported by Law360. In a statement Wednesday, attorneys for the four named plaintiffs said algorithmic pricing and information exchange platforms continue to spread to more industries. "Plaintiffs allege that these practices in the mortgage industry are anticompetitive, have placed American borrowers on the receiving end of inflated mortgage rates, and justify class relief," said Robin A. van der Meulen, partner at New York-based Scott + Scott, in an email. The prospective class spans likely millions of members, while neither attorneys nor the complaint speculated on the amount of damages plaintiffs could realize. The lawsuit focuses on rate spreads, or the difference between a loan's annual percentage rate and the Consumer Financial Protection Bureau's average prime offer rate. Since 2020, plaintiffs say mortgages issued by Optimal Blue users were around 2.68 basis points higher than non-users. "More damning still, Optimal Blue users' rate spreads after 2019 — controlling for pandemic effects and other variables — were 9.6 basis points higher than their pre-2020 baseline, representing a massive windfall extracted from American homebuyers," wrote counsel for plaintiffs. In a statement Wednesday, Optimal Blue said it doesn't agree with plaintiffs' assertions, but it could not provide further comment during the legal process. "We are confident that we can demonstrate how Optimal Blue's products actually foster competition in the mortgage industry," the statement said. Which companies are accused of price-fixing?The complaint names 29 companies as defendants, claiming the originators on the list used the Optimal Blue tools in question for at least a portion of their originations between 2019 and 2024. Of the 26 lenders, 11 responded to National Mortgage News and declined to comment. The independent mortgage banks being sued are: Rocket Mortgage and Mr. Cooper, United Wholesale Mortgage, Loandepot, Fairway Independent Mortgage, Freedom Mortgage, Rate, Newrez, CrossCountry, Pennymac, Guild, New American Funding, CMG Mortgage, Amerisave Mortgage, Better Mortgage, Churchill Mortgage, Movement Mortgage and Beeline Loans. The depositories and their home lending arms named as defendants are Wells Fargo, JPMorgan Chase, Bank of America, U.S. Bank, Citibank, Flagstar Bank, Firstbank Mortgage, and First Community Mortgage.Also being sued are former Optimal Blue provider Black Knight and that company's current owner, Constellation Software. Representatives for those companies didn't return requests for comment. Why borrowers are calling the firms a cartelThe homeowners, who obtained loans between 2022 and 2025, point to the data hubs in which originators share their real-time, sensitive loan and profit information to Optimal Blue "as the price of admission to this cartel."The nonpublic information includes loan originators' margins, loan-level pricing adjustments, concessions, servicing release premiums, loan officer compensation, and borrower credit profiles sortable down to LO, branch and geographic levels. "Defendants freely share this intelligence as the price of cartel membership, ensuring uniformly inflated mortgage prices for American families," the suit reads. Attorneys wrote that Optimal Blue claims to work with 3,500 lenders, although they did not respond to a question Wednesday why they named the 26 specific lender defendants. Plaintiffs say the conspiracy has compounded the current affordability crisis, in which borrowers today are beset by high home prices and mortgage rates sitting over 6%. The complaint states Optimal Blue users' rate spreads averaged around 4.52 basis points lower than other lenders on average, prior to its rollout of business analytics tools. Optimal Blue, which also publishes frequent public reports on market dynamics, was acquired by Toronto-based Constellation in 2023. The Canadian company paid $700 million for the platform which Intercontinental Exchange divested during its purchase of Black Knight.

Shutdown hampers rates, rural, HECM and niche condo loans

unitedbrokersinc_m7cmpd2025-10-09T10:23:07+00:00The lingering government shutdown has increased rate uncertainty, and cut off or curtailed some specialized mortgages while mainstream business moves forward, albeit at a slower pace in some cases."Until key reports like payrolls and the CPI return, rates are likely to remain range-bound but vulnerable to sudden shifts," said Sam Williamson, chief economist at First American, referencing the Consumer Price Index report.Although the shutdown began with some downward pressure on benchmark 10-year Treasury bond yield, it later experienced some upward pressure related to uncertainty around monetary policy direction and fluctuated."That volatility is spilling into mortgage rates, which loosely track the 10-year," Williamson said.Between rate uncertainty and shutdown-related slowdowns in processing that may be related to things like public staffing shortage or a need to work around federal flood insurance restrictions, mortgage applications inched down last week. In addition, some segments of the market are particularly constrained.Some of the details around how rural, reverse mortgage, condominium and home improvement loan markets have been impacted and the effect on lenders and borrowers follow. The current status of the USDA Rural Housing Service programIn line with past suspensions of federal budgetary functions, the Department of Agriculture's home lending has been "effectively shut down," said Daniel Jacobs, head of the TruTeam at CrossCountry Mortgage, in line with a statement on the USDA website."Their staff is on furlough and there is currently no ability to obtain conditional commitments," he said.USDA borrowers have been among the hardest hit because their loans are specialized in ways that make it difficult to find a private market equivalent. Exemplifying this is the fact that it is the only agency to offer a construction-to-permanent single-close loan that can immediately be securitized, noted Sean Faries, CEO at Land Gorilla, a provider of loan construction automation for lenders."That was starting to gain traction and won't be able to continue without appropriation," he said.What limits to FHA condo lending mean for single unitsAlso, FHA condo projects can't be processed through the Department of Housing and Urban Development's HUD review and approval process. HRAP otherwise would allow single-unit approvals even if the overall building they're in didn't have one, subject to limits.The lack of available condo approvals limits FHA lending in that sector to buildings that had approvals before the shutdown.While the HRAP is typically limited to 10% of a building's units — or two for housing projects with less than 10 — workarounds for those that can't access it may be limited to moving to options outside the FHA program. Some customers in the FHA market might not qualify for those.Some reverse mortgages face endorsement suspension and RFIThe FHA also is not processing new approvals to insure Home Equity Conversion Mortgages during the shutdown but other aspects of that market have been functioning."In the short term, only endorsements are on hold," said Michael McCully, partner at New View Advisors, a provider of capital markets and investment banking services for the reverse mortgage industry.A lender may choose to move forward with a HECM without an endorsement if they have the wherewithal to hold the loan on their balance sheet until the shutdown ends, similar to the way some companies have been willing to make conforming loans early."While HECM endorsements have been suspended it is not adversely impacting the ability of many lenders to facilitate timely closings for consumers," Jacob said.In addition to suspended endorsements, HECMs have drawn focus in a request for information that Ginnie Mae — which remains operational during shutdowns — released Oct. 2. The RFI seeks feedback on HECM securitization risks, opportunities, the impact on private capital and what's held back volume.While there are private market options and securitization numbers have seen limited growth over time, HECMs have historically constituted the largest part of the reverse mortgage market.Impact on Title I and the difference technology makesEndorsements for the niche Title I program, which includes home improvement products with a relatively small balance and certain manufactured housing loans, also have been suspended for the duration of the shutdown."The HUD Title I program is rarely offered by mortgage lenders anymore. Community banks and credit unions are the most likely sources," said Dan Green, president of Homebuyer.com, an information and lead generation website.Other types of renovation loan programs at the government-sponsored enterprises that operate outside the federal budget process and endorsements for another FHA program called 203k that serves as a rehab and purchase loan remain available.The 203k program, like other FHA offerings, could still be impacted by thin staffing due to furloughs amid the shutdown, which any service that's not completely automated may be susceptible to, said Faries. Because a 203k loan can be a bit more complicated than some other mortgages, it might be more likely to require staff intervention that could be affected by furloughs that the Trump administration has threatened to transform into layoffs, if allowed."You could get into a situation where you had to do some sort of manual underwriting exercise and needed guidance," he said. "If you know you have this loan that's super complicated and you need help, you could expect delays in the process just due to short staffing."Increased automation in government-related housing finance has made it easier to weather the shutdown in some cases, Faries said."I remember the IRS being a big hiccup, but now that they've got a lot of automation in place a lot of services provide that automatically," he said.