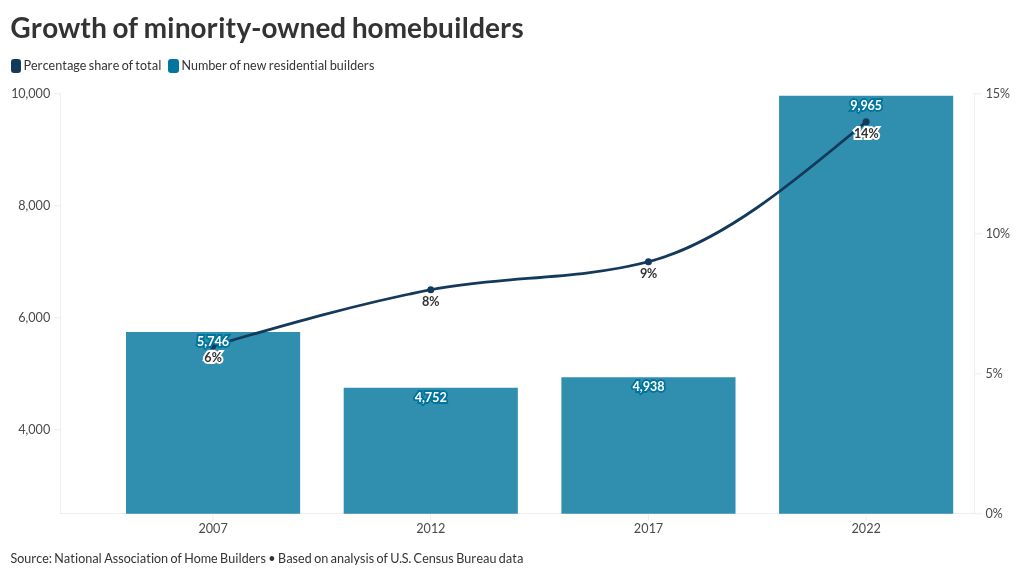

Growth of minority builders collides with policy rollback

unitedbrokersinc_m7cmpd2025-10-07T20:22:54+00:00Minority homebuilding businesses grew noticeably in the years after the Great Financial Crisis, but their share still lags when compared to the total population of people of color in the U.S., new analysis finds. The percentage of newly established minority-owned homebuilders more than doubled between pre-crisis 2007 and 2022 from 6% to 14%, according to an analysis of U.S. Census Bureau data. The bureau defines minority-owned if the majority share of equity in the business belongs to "any race and ethnicity combination other than non-Hispanic and white." Research was conducted by the National Association of Home Builders. Much of the growth in businesses came during the five-year period from 2017 to 2022, when the number of new residential building companies surged noticeably from 4,938, which represented 9% of the industry at the time, to 9,965. "Nevertheless, when compared to the overall U.S. population, minority-owned firms continue to be underrepresented," wrote NAHB researchers.Similar growth trends emerged in the remodeling sector, with the number of firms expanding from just 8% of businesses in 2007 to an 18% share by 2022. On a unit-business basis, the total number grew from 7,093 to 22,119. Much of the minority-business expansion also occurred in the five years after 2017, when 11,565 such companies were already established. Despite the rise in business opportunities, though, the growth in homebuilder and remodeling companies still come in significantly below the share of racial minorities currently residing in the U.S., which was approximately 40% in 2022. How government policies could impact minority-owned businessesThe acceleration in the number of new minority-owned construction enterprises between 2017 and 2022 came as housing and lending organizations prioritized policies and initiatives aimed to close the homeownership gap existing between whites and nonwhite ethnic groups. The spike in the number of businesses also occurred under both Republican and Democratic presidential administrations.Since the start of his second term, President Trump has made the elimination of programs and agencies supporting what might he deemed "woke policies" a cornerstone of his administration. Federal initiatives aimed to increase minority homeownership or invest in underserved communities have been among many eliminated or revoked. Some private businesses have largely followed suit by curbing efforts to promote diversity, equity and inclusion, including removing associated mission language or reducing community outreach. In March, the president also moved to dismantle through executive order the Minority Business Development Agency, which helped lead to growth of homebuilding firms. Housed within the Department of Commerce, the agency was established in 1969 and was made permanent in 2021 under the bipartisan infrastructure bill. Two months later, a federal district court issued a preliminary injunction requiring the Trump administration to reverse its actions against MBDA and other programs. The administration has appealed the decision.