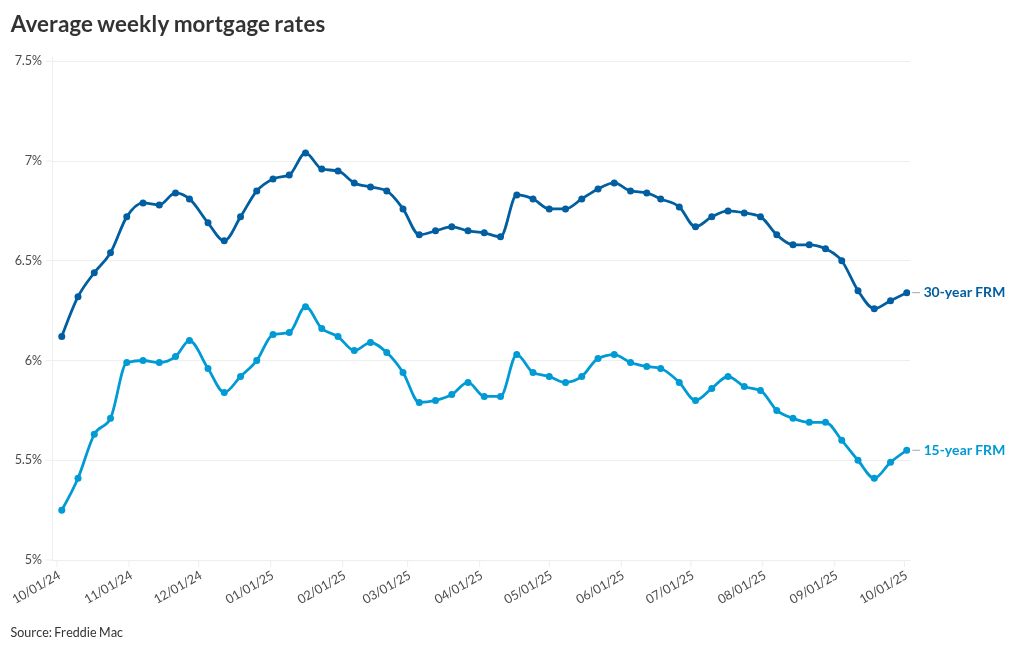

What's at stake: Mortgages requiring federal flood insurance will be more difficult to close during the shutdown, among other impacts. Expert quote: For "financial services broadly, banks in particular, there are going to be disruptions." — Brian Gardner, Stifel Financial Corp.Forward look: Extended shutdowns threaten federal worker pay and U.S. creditworthiness, potentially triggering broader market disruptions that would affect banks' Treasury holdings and lending activity.WASHINGTON — The threat of government shutdown has become somewhat commonplace in Washington, part of the push and pull of a tightly divided Congress. But when the government shut down at midnight Wednesday morning, it marked the first closure since early 2019, which was the longest in history at 35 days. Republicans and Democratic lawmakers are deadlocked as Democrats refuse to vote on a bill that wouldn't extend health care subsidies set to expire at the end of the year, subsidies that are necessary to stave off dramatic increases in health care prices for millions of Americans. Republicans won't negotiate or vote on Democrats' alternative legislation. Banking is more insulated than many other industries from the immediate impacts of a government shutdown. Most banking agencies, including the Federal Reserve, the Federal Deposit Insurance Corp. and the Consumer Financial Protection Bureau, are self funded or funded outside of the traditional Congressional appropriations process, and thus will continue operating mostly as normal. That being said, an extended shutdown that would slash pay cuts for federal workers and threaten the credit of the United States would have long-lasting implications for all kinds of financial institutions, banks included. "Financial services, broadly, banks in particular, there are going to be disruptions," said Brian Gardner, Chief Washington Policy Strategist at Stifel Financial Corp. "And the longer the shutdown, the more disruptive they are." And there are a few key programs that grind to a halt immediately. Here's the ways the government shutdown will most greatly affect the banking sector. Financial regulatory agencies face more uncertainty This shutdown is happening against the backdrop of a broader effort by the Trump administration to restructure the regulatory state, most notably for banks in the form of a radical reduction in the CFPB workforce. While the agency is self-funded, Trump has said that his administration might use the shutdown to lay off thousands of government employees, an effort that has been underway at the bureau since February. Adam Martinez, the CFPB's associate director and chief operating officer, sent an email to staff late Tuesday about planning for a lapse in federal funding, according to a copy of the email obtained by American Banker. The CFPB is funded by annual funding requests to the Federal Reserve, which is funded by its monetary policy activities. "CFPB will continue operations in the event of a shutdown, even though some other parts of the federal government would be affected. Therefore, CFPB employees should plan to report to work as usual on Wednesday October 1, 2025. Bureau leadership will monitor the situation and alert you if any services may be disrupted or if you will need to alter processes," Martinez said in the email. "The Bureau anticipates no disruption in pay, benefits, travel, or other services should other agencies close," the email said. Currently, the majority of CFPB employees are being paid not to work. Acting CFPB Director Russell Vought, who is also the Trump administration's director of the Office of Management and Budget, directed staff to "stand down" in February and moved to fire most of the bureau's employees. The CFPB workers' union sued, gaining an injunction against the administration issuing a reduction-in-force without following proper procedure. An appeals court stayed the injunction last month, and the union is now appealing the stay to the full DC Circuit.The FDIC and the Fed are also self-funded — the FDIC through fees to banks, the Fed via its monetary policy operations — and will continue to operate largely as normal during a shutdown. The Office of the Comptroller of the Currency, which is housed in the Treasury Department, could see some minor disruptions, although a large share of Treasury's workers are considered "essential" and thus not subject to furlough during government shutdowns. The Securities and Exchange Commission has in the past mostly shut down during a government funding lapse. "What is deemed to be non-essential activities are going to cease, said Gardner. "Nonessential is in the eye of the beholder, and there's a lot that the administration can decide is essential and what is nonessential." Based on historical patterns, that means the SEC will go dark, he said. "So if you're looking to raise capital, your registration statement is probably not going to get processed," he said. Flood insurance program grinds to a halt One of the most immediate and concrete impacts on banks' daily operations comes from the closure of the National Flood Insurance Program. Without congressional authorization, the Federal Emergency Management Agency cannot issue new flood insurance policies, effectively blocking a significant number of mortgage originations."What is clear is that the flood insurance program will close to new policies until there is a spending deal," said Jaret Seiberg, an analyst with TD Cowen, in a note Wednesday. "That means no mortgages which require federal flood insurance will be originated."The impact hits banks in coastal and flood-prone regions particularly hard. Any property in a designated flood zone that requires a federally-backed mortgage must carry flood insurance. When the federal program shuts down, those transactions simply cannot close. While private flood insurance exists, it remains a relatively small market and doesn't fully substitute for the federal program's reach and affordability.Banks have developed workarounds through repeated exposure to shutdown threats. "The short-term impact is limited as lenders have been through shutdown threats repeatedly," Seiberg said. "The industry will move up closings to get ahead of the Sept. 30 deadline. This softens the impact, though extended shutdowns will block mortgages from being made."The Fed, the FDIC and the OCC issued reminders to lenders that they may continue to make loans that are subject to the federal flood insurance statutes when the National Flood Insurance Program is not available. "Lenders may continue to make loans without flood insurance coverage during this time but must continue to make flood determinations; provide timely, complete, and accurate notices to borrowers; and comply with other applicable parts of the flood insurance regulations," the agencies said. "In addition, lenders should evaluate safety and soundness and legal risks and should prudently manage those risks during the lapse period." Both House Financial Services Committee Chairman French Hill, R-Ark., and the committee's ranking member Maxine Waters, D-Calif., pointed to the flood insurance lapse just after the shutdown. Hill said that the lapse hurts "at-risk property owners across our nation," while Waters said that the program "would largely be unable to pay out flood insurance claims, and its flood mapping process would ultimately come to a halt — all during the height of hurricane season." Small business lending and community development stallBeyond mortgages, the shutdown could immediately freeze Small Business Administration loan programs that many banks rely on to serve small business customers. "SBA loans probably will not be processed … during the shutdown," Gardner said. "This creates a particularly difficult situation for banks that specialize in SBA lending, where government guarantees allow them to extend credit to businesses that might not qualify for conventional loans." Community Development Financial Institution programs also face disruptions, mostly in processing updates to CDFI status and applications, a process already slowed by the Trump administration's hostility toward the CDFI industry. Updates to the CDFI website will be unavailable during the shutdown, the fund said in an update, and the help desk will be unable to respond to questions related to CDFI Fund programs, compliance or certifications. The CDFI Fund is also not able to process new applications for lending awards to replace previous applications that made references to ethnicity, race or climate — initiatives that the administration has pledged to end support for. Treasury said the CDFI Fund will resume processing applications after the government shutdown is finished, but it's unclear what will happen to applications received between when the government reopens and the deadline closes. Economic data blackout complicates planning Perhaps less visible but equally consequential is the shutdown's impact on economic data collection and publication. The Bureau of Labor Statistics, Census Bureau, and other agencies that produce the employment reports, inflation data, and economic indicators that banks depend on for strategic planning largely cease operations."The whole situation around the BLS, there's a lot of attention on they're not going to come out with data," said Ian Katz. "That's the same as it would have been in another time. But now, because that whole issue has become so political and fraught, BLS not putting out data is going to be a big deal in Washington."Banks rely on government economic data for everything from setting lending standards to stress-testing their capital positions to forecasting loan demand. Risk management teams use employment reports to gauge consumer credit quality. Commercial lending officers study GDP and manufacturing data to assess business borrowers' prospects. Treasury departments analyze inflation trends to manage interest rate risk.When this data flow stops, banks must rely on private-sector forecasts and proprietary models, introducing additional uncertainty into already complex projections. The problem compounds if the shutdown extends long enough that multiple scheduled data releases get skipped entirely, creating gaps in the economic time series that banks use for historical analysis and modeling.The data blackout also affects banks' ability to comply with regulatory stress testing requirements, which demand sophisticated analysis of how their portfolios would perform under adverse economic scenarios. While regulators may grant extensions or flexibility during shutdowns, the underlying challenge remains: banks are trying to make billion-dollar decisions with some of their most important information sources unavailable.Market impact uncertain Historical precedent suggests financial markets may shrug off the shutdown, at least initially."I went back and looked at lengthy government shutdowns — not the one or two day variety, not the ones that happened over weekends and holidays, but instances where there are shutdowns of five trading days in a row or more," Gardner said. "There have been some sell-offs years ago. But the more recent shutdowns, I don't think you can really see much going on with the markets."Markets have become desensitized to Washington's fiscal dysfunction, viewing shutdowns as political theater rather than genuine economic crises. Traders expect Congress will eventually reach a deal, and the direct impact on corporate earnings and economic growth from a short shutdown remains minimal.However, an extended closure that threatens federal worker paychecks, delays government contracts, and raises questions about U.S. creditworthiness could shift market sentiment. Banks hold substantial Treasury securities in their investment portfolios, and any hint of credit risk associated with U.S. government debt would reverberate throughout the financial system. The longer the shutdown persists, the greater the risk that it evolves from a manageable inconvenience into a confidence-shaking event that affects lending, investment, and economic activity in ways that ultimately hit banks' balance sheets.