Freddie Mac earnings rise on better rate environment

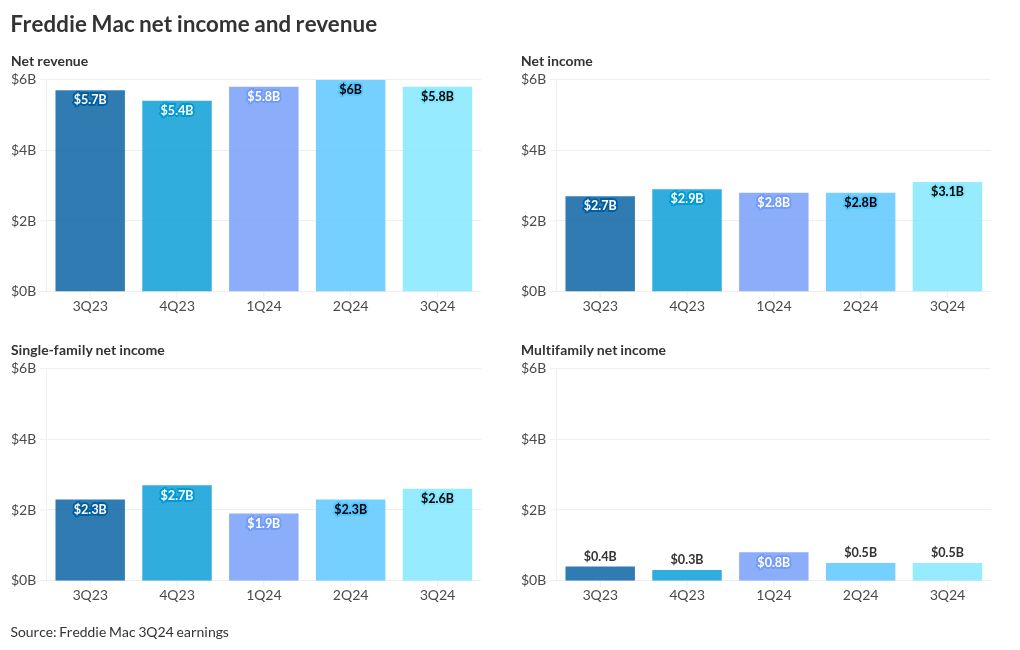

unitedbrokersinc_m7cmpd2024-10-30T16:23:11+00:00Freddie Mac had its strongest quarter of the year for both net income and in new business acquired as mortgage rates dipped.Its earnings call, hosted by James Whitlinger, interim chief financial officer, was terse, as it has been in recent years as Freddie Mac remains in conservatorship.The opening statement on the call covered Freddie Mac's efforts to keep people in their residences on both the multifamily side, with its August framework regarding minimum lease standards, and in single-family by reminding borrowers affected by Hurricanes Helene and Milton regarding the options available to them, such as forbearance."We also provide dedicated resources to renters and apartment buildings to help them plan and prepare for natural disasters as well as respond and recover after they strike," Whitlinger said. "Freddie Mac, communities and mortgage security investors all benefit alongside renters and homeowners when families are able to continue living in their homes."Net income at the government-sponsored enterprise was higher than the comparative periods. Freddie Mac earned $3.1 billion in the third quarter, up from $2.77 billion in the second quarter and $2.69 billion for the same period one year ago.The increase was primarily driven by a rise in net revenues and a decline in noninterest expenses. The latter improved because one year ago, Freddie Mac made an accrual of $313 million for an adverse judgment at trial when it was sued by preferred stockholders.That expense did not recur this quarter.Most of Freddie Mac's third quarter growth in net income came from the single-family business, which earned $2.57 billion, up from $2.28 billion in the prior quarter and $2.32 billion for the third quarter of 2023.The recent third quarter was the best by far this year for single-family new business activity, with $98 billion, versus $85 billion for both the second quarter and one year ago. This was the beneficiary of mortgage rates dipping as low as 6.08% by the end of the period, although they have been on the rise in the weeks since then.Purchase business made up $84 billion of the third quarter total of loans acquired, while refinances accounted for the remaining $15 billion.However, the serious delinquency rate in the segment rose four basis points, albeit off of an all-time low in the second quarter, to 54 basis points from 50 basis points. Whitlinger noted that was still 9 basis points lower than the 63 basis points recorded at the end of 2019.Notwithstanding that, "In the third quarter of 2023 we had a benefit for credit losses of $263 million which was primarily driven by credit reserve release in single-family due to improvements in house prices," he noted.Multifamily new business also rose to its highest level of the year so far, to $15 billion, compared with $11 billion in the second quarter and $9 billion in the first quarter. For the third quarter of 2023, Freddie Mac did $13 billion of new business activity in this segment.This line remained profitable at $532 million of net income, up by $51 million from $481 million one quarter ago, and by $170 million from $362 million for the third quarter last year.Its multifamily serious delinquency rate, which has been on the rise, had a much more moderate increase than in recent periods. It ended the quarter at 39 basis points, up 1 basis point from the second quarter. A year ago, it was at 24 basis points."This increase was driven primarily by an increase in delinquent floating rate loans, including small balance loans that are in their floating rate period; 96% of these delinquent loans have credit enhancement coverage," Whitlinger said.Freddie Mac's net worth increased to $56.4 billion as of Sept. 30, versus $53.2 billion on June 30 and $44.7 billion one year ago.That increase is a result of not having to pay any dividends to the U.S. Treasury because of the Preferred Stock Purchase Agreement modifications.But that means the liquidation preference for those holdings will increase in the fourth quarter to $129 billion from $125.9 billion on Sept. 30.