Mortgage rates move lower for first time in four weeks

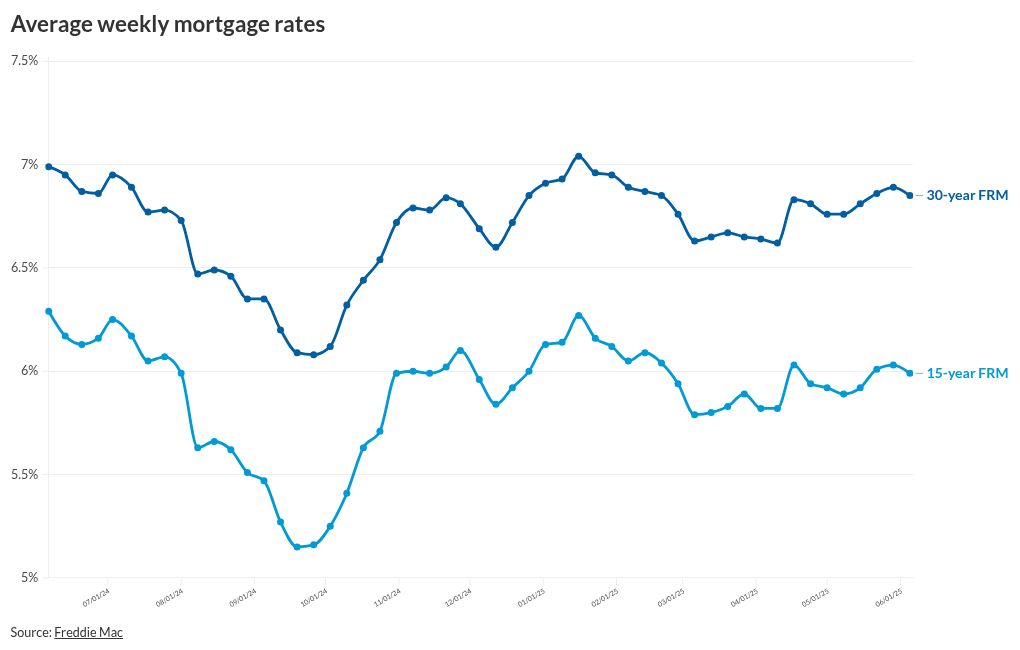

unitedbrokersinc_m7cmpd2025-06-05T18:23:07+00:00For the first time in four weeks, mortgage rates have moved lower, following another seven-day period where the benchmark 10-year Treasury yield moved in a wide range.However, rates are still at levels last seen in February, the Freddie Mac Primary Mortgage Market Survey showed."The average mortgage rate decreased this week, which is welcome news to potential homebuyers who also are seeing inventory improve and house price growth slow," said Sam Khater, Freddie Mac chief economist, in a press release.The 30-year fixed-rate mortgage averaged 6.85% as of June 5, compared with last week, when it was 6.89%. It remained lower than the same week a year ago, when it averaged 6.99%. Meanwhile, the 15-year FRM also moved 4 basis points lower than the previous week and back under 6%, to 5.99%. This compared with 6.03% on May 29 and 6.29% as of June 6, 2024.This rate drop, while lower than expected, is a "small but positive shift" for housing, said Samir Dedhia, CEO of One Real Mortgage.What other gauges show about mortgage ratesThe 10-year Treasury, which had a high nearing 4.5% intraday on May 28 before dropping down to 4.24% at its close, moved back above 4.6% earlier this week before ending June 4 at 4.37%.At 11 a.m. Thursday morning, it had regained 1 basis point and was at 4.38%. A higher number of jobless claims led to the increase, explained Louis Navellier, an investment banker. "The bond market was not very reactive to the labor news either," he added.Zillow Home Loans mortgage rate tracker reflected such movements, with the 30-year FRM falling to 6.9% on June 4 from an average of 7.01% one week earlier.By 11 a.m. on Thursday morning, it was up to 6.91%. At that same time on May 28, it was at 7.08%.Lender Price data posted at the same time on the National Mortgage News website had the 30-year at 6.902%, compared with 6.982% one week prior.What moved mortgage rates this weekThis was a "small respite" for mortgage borrowers, Kara Ng, Zillow senior economist, said in a June 4 blog posting."Bond yields — and the mortgage rates that tend to follow them — fell as the ADP employment report showed private employers added only 37,000 jobs in May, one third of what was expected by economists," Ng said. "The Bureau of Labor Statistics employment report, released June 6, will give economists another glimpse of how the labor market is faring."Easing inflation pressures and more stable activity in the bond market drove the decline in the Freddie Mac survey, Dedhia added. "As Treasury yields pulled back, mortgage rates followed, showing that the market is still very sensitive to economic data and investor expectations around future Fed decisions," Dedhia continued. "While we're not seeing a dramatic drop, this kind of consistency is a good sign as we move into the heart of the summer buying season."The rates some lenders are promoting aren't a reliable indicator of actual market conditions."Mortgage rates stay hunkered at 7%, and secondary [mortgage-backed securities] spreads are 155 basis points over Treasuries despite the budget deficit narrative keeping rate [volatility] relatively high," Eric Hagen, analyst at BTIG, wrote in his June 4 roundup."We see a handful of originators still advertising teaser rates near 6.5%, but it tends to include higher up-front points, which are typically less attractive from the borrower's perspective if there could be a refi opportunity in the near future," he said.How current mortgage rates affect first-time homebuyersHagen pointed to comments in the senior loan officer survey from the Fed in April indicating a tighter credit box for non-agency mortgages.It suggests "the marginal first-time buyer with a high debt-to-income [ratio] is probably getting priced-out right now versus remaining a renter, even if buyers are picking up some more bargaining power because home price appreciation is tapering off," Hagen said.The Mortgage Bankers Association's Weekly Application Survey released June 4 noted rates on the conforming 30-year FRM fell 6 basis points to 6.92% as of May 30."Mortgage rates near 7% are keeping mortgage activity in a holding pattern," MBA President and CEO Bob Broeksmit said in a Thursday morning statement. "Although refinance and home purchase applications are consistently higher than last year's pace, we expect activity to remain within the same narrow range until mortgage rates move lower."The group's current forecast is for rates to fall to 6.6% by the end of 2025, "which should increase demand," Broeksmit continued.Ng said even with higher rates, affordability is better than last year, as the typical mortgage payment is 1.7% lower than May 2024."Economic uncertainty held back sales activity in April," Ng said. "The stock market's significant volatility during this period may have impacted down payments and made households nervous about the future, leading to buyer hesitation."