Rich in equity and low on new housing options, owners eye renovations

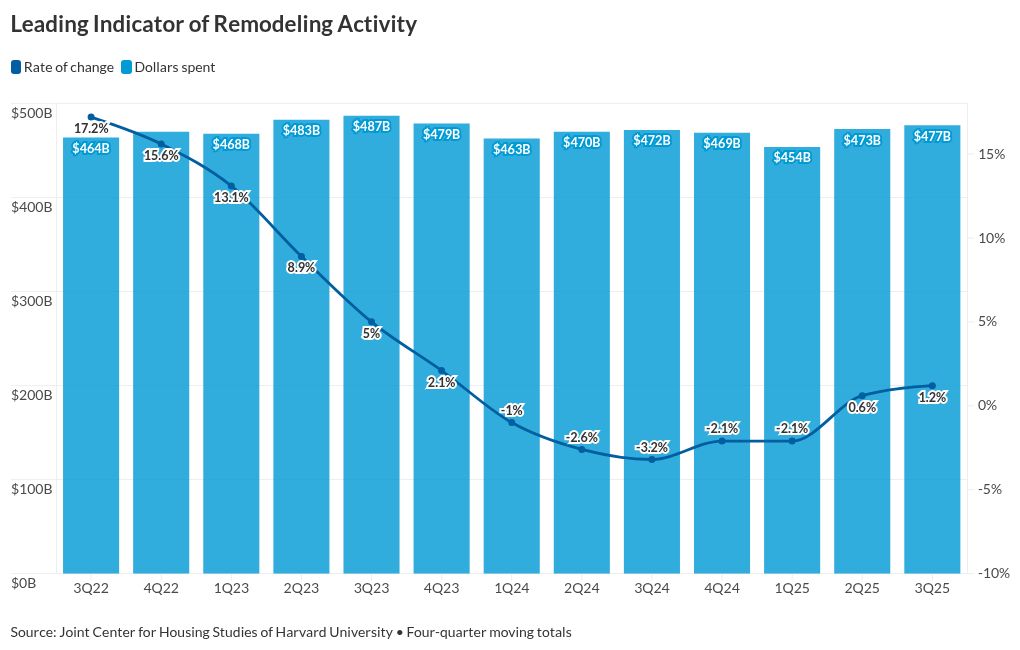

unitedbrokersinc_m7cmpd2024-10-18T17:24:23+00:00Roadblocks in the purchase market could be the green light for other types of home financing. Annual spending for home improvement and maintenance is projected to grow to $477 billion on an annual basis in the next 12 months, according to the Joint Center for Housing Studies of Harvard University. That projection, while trailing recent heights for 12-month stretches, indicates signs of life for consumer spending on the home.Carlos Martin, director of the Remodeling Futures Program at the JCHS, said the remodeling uptick will stem from lagging construction and muted sales of existing homes – what the market has deemed the "lock-in" effect. "Additionally, stronger gains in home values and thus home equity levels should boost both discretionary and 'need-to-do' replacement projects for owners staying in place," said Martin in a press release. Renovation spending could be a driver for refi volume expected to double next year. Economists at Fannie Mae forecast over $600 billion in refi volume in 2025, production expectations it said are still at risk of rate volatility. Mortgage rates are expected to drop to around 6% to end this year, and average 5.7% across 2025, according to the government-sponsored enterprise. Many borrowers appear to be hanging on to their ultra-low rates they secured during the pandemic, and refinance demand has wavered after a recent, short-lived boom. The Remodeling Futures Program's Leading Indicator of Remodeling Activity expects annual expenditures for renovations to grow by 1.2% through the third quarter of 2025. That would be far below the 17.2% growth in that metric in the third quarter of 2022, but still well above total spending levels of yesteryear. Lenders are keen on the apparent cash-out refinance opportunity, rolling out promotions to capture homeowners unmoved by rates still in the 6% range. Homeowners are also sitting on massive equity, built by the steady rise in home prices since the pandemic. Homebuilders are catching up to the nation's inventory shortage, and some green shoots in building statistics are emerging. The National Association of Home Builders recently put nationwide inventory at a relatively low 4.7 months worth of supply however, and experts emphasize the supply crunch is holding up the market.