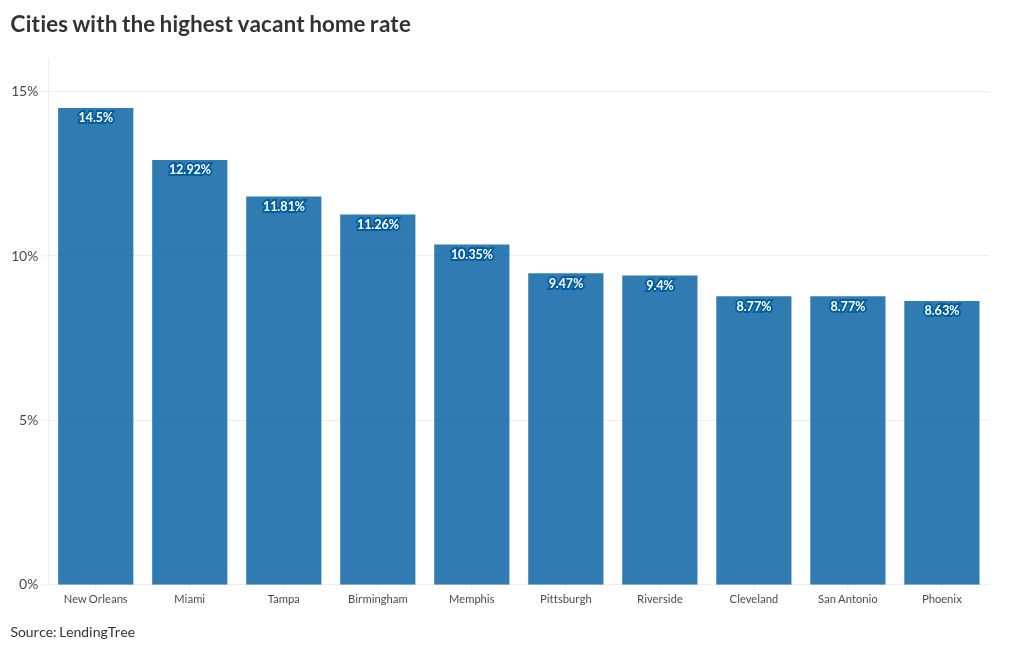

Why does the rise in vacant homes not solve inventory woes?

unitedbrokersinc_m7cmpd2024-10-09T20:22:45+00:00Vacant home rates increased nationwide in 2023 over the prior year, and these properties are empty for many reasons beyond simply being uninhabitable, a LendingTree study said.As a result, it is unclear on the impact making these available would have on reducing the inventory shortage.Just over 5.6 million units were sitting vacant during the period covered by the study in the nation's top 50 metro areas. This translates to a vacancy rate of 7.37%, up from 7.22% during 2022.More than half of those houses are vacant because they are waiting to be rented or are used only during part of the year; specifically 27.9% were empty because they're for rent, while 20.73% are only occupied part time for seasonal, recreational or occasional uses."Remember, just because there are millions of homes sitting vacant across the nation's 50 largest metros, that doesn't mean that the U.S. has an overabundance of housing,." said Jacob Channel, LendingTree senior economist and the author of the report."On the contrary, given the reasons why homes tend to sit vacant — and that vacancies tend to only be temporary — there isn't much reason to conclude that the nation's housing supply is anything but insufficient in the face of homebuyer and renter demand."Single-family rental properties are a hot button issue for consumer advocates, as well as the presidential campaign of Kamala Harris, who in August took aim at corporate ownership in a policy speech.New Orleans has the highest vacancy rate in the nation, at 14.5%, with the most common reason attributed to units being used to rent that are not occupied at the time. That is the case for just under one-quarter of the empty homes in that city.Seasonal or recreational use were the reasons for the vacancies in the Nos. 2 and 3 cities of Miami and Tampa.While "for rent" was cited as the reason in only five of the top 10 cities when it came to vacancy rates, it was the most cited cause, including for all but one metro area from slots 24 to 50."With home prices as high as they are, it may seem strange that so many homes in the nation's largest metros are sitting empty," Channel wrote.But "many nuanced factors" are used in setting home prices. These include the location, the mortgage rate, the size of the property, why the home is not occupied and how long it is empty."Why a home is empty is just as important as the fact that it's empty, if not more," he continued. "Only by analyzing the reasons behind a vacancy can you understand the relationship between housing prices and vacancy rates."While the vacancy rate on its own isn't nuanced enough to fully explain why homes are so expensive, that doesn't mean it can't help shed light on how an area's housing market is fairing, Channel said.Foreclosed homes, which also have been described as zombie properties, do not seem to be a major issue when it comes to vacancy share. Only three cities show vacancy rates exceeding 1% due to foreclosures: St. Louis, 1.48%; Chicago, 1.38%; and Richmond, Virginia, 1.14%, while Pittsburgh, it is at 0.9%.