Mortgage hiring tapers, U.S. job surge dampens rate cut hope

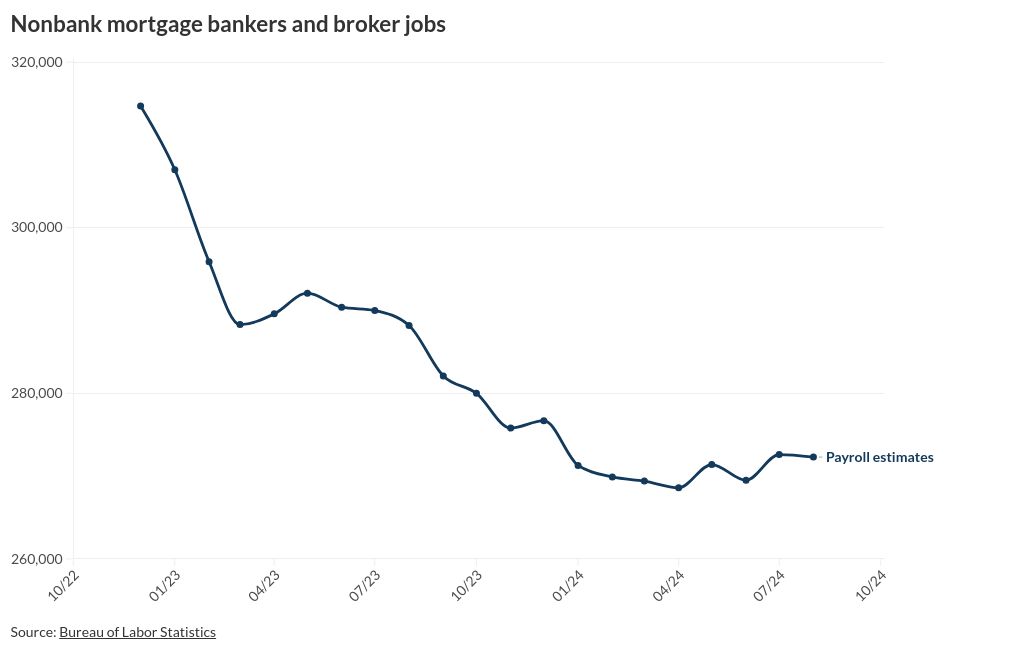

unitedbrokersinc_m7cmpd2024-10-04T14:22:39+00:00A jump in U.S. job numbers above the levels seen the previous month cooled interest rate cut expectations Friday, and nonbank mortgage broker and bank job estimates released that day softened.U.S. jobs rose by 254,000 in September, above expectations for 150,000 more in line with August's addition. Unemployment was 4.1% as compared to the 4.2% anticipated. New industry payroll estimates for August activity totaled 272,300 compared to an upwardly revised 272,600. "Employment continued to trend up in food services and drinking places, health care, government, social assistance and construction," the Bureau of Labor Statistics report said.The numbers suggest that while federal monetary policymakers may continue to cut short-term rates they control, it won't be as aggressive as the 50 basis point cut last month."A return to a more normal cadence of 25 basis point cuts is likely at the November meeting, and at each meeting beyond that, until the fed funds rate returns to a neutral level next summer," said Michael Brown, senior research strategist at Pepperstone, in a report. This makes it less likely mortgage borrowers, brokers and lenders will get much more interest rate relief."Interest rates jumped on the release of this report," Michael Fratantoni, chief economist at the Mortgage Bankers Association, said in an emailed statement."MBA's forecast is for longer-term rates, including mortgage rates, to remain within a relatively narrow range over the next year. This news will push mortgage rates to the top of that range, but we do expect that mortgage rates will stay close to 6% over the next 12 months," he added.While the market was somewhat surprised by Friday's employment report, there had been other indications that hiring has been a little stronger recently earlier in the week.The August Job Openings and Labor Turnover survey numbers had signaled that in some respects U.S. employment conditions are surprisingly robust, according to a report from Rania Gule, senior market analyst at global multi-asset broker XS.com.U.S. job openings rose during the month to 8.4 million, following two consecutive declines earlier, Gule noted."This reflects ongoing strength in the labor market, prompting traders to lower their expectations for any significant monetary easing," said Gule.Private payroll numbers released two days earlier showed 143,000 jobs added in September, according to a report ADP produced in collaboration with Stanford Digital Economy Lab. The number was larger than anticipated after five months of slower activity but still below the 200,000 benchmark.Compensation for private workers softened compared to a year earlier in the payroll provider's September report, particularly for workers who changed jobs. The latter category saw their average increase fall from 7.3% to 6.6%, while the former dipped slightly to 4.7%."Stronger hiring didn't require stronger pay growth last month. Typically, workers who change jobs see faster pay growth. But that premium over job-stayers shrank to 1.9 percent, matching a low we last saw in January," ADP chief economist Nela Richardson said. At 225,000, initial jobless claims outpaced estimates for 220,000 this week, according to Cody Echols at Mortgage Capital Trading. Continuing claims largely plateaued."Continued geopolitical tensions also continue to remain high, which is driving uncertainty with global markets," said Echols, who is a senior capital markets technology advisor at MCT.