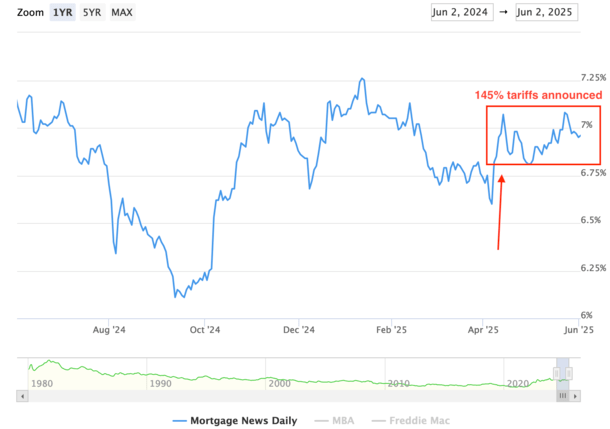

Bloomberg News For the past five years, the Treasury market has been a point of concern for financial regulators, market participants, academics and other observers. Earlier this spring, it looked to many like those fears might come to a head.On April 2, President Donald Trump rolled out new tariffs on virtually every country in the world, including prohibitively high levies against Chinese imports. Two days later, investors began shedding bonds rapidly, driving yields up and sapping liquidity from the Treasury market. While trade policy was an unlikely source of such financial volatility, it was the type of anomalous shock that stability hawks have feared since the last big Treasury market shake-up at the onset of the COVID-19 pandemic — an episode that caused the Federal Reserve to intervene to rescue the market. Anil Kashyap, an economics professor at the University of Chicago, said the ballooning federal debt, the rise of complicated Treasury trading schemes and waning intermediation capacity since 2020 have left the market vulnerable to what might otherwise be minor disruptions. "On April 1, I don't think a lot of people had Treasury chaos resulting from a tariff announcement on their bingo cards," Kashyap said. "The problem is that there are all kinds of potential triggers that we haven't thought of that we'll only recognize once they happen. That's the world we're living in now."Concerns in the Treasury market largely abated after the Trump administration placed a 90-day pause on many of the steepest tariff increases. Yields have continued to trend up, albeit less steeply than in early April, and demand has been weak for new bond issuances — developments that have been attributed to a bigger-than-expected budget bill that is poised to grow the federal deficit — but the potential destabilizing volatility has dissipated. In hindsight, Treasury markets continued to function through the distress. Unlike March 2020, primary dealers were able to absorb the excess inventory during the sell-off and hold it until demand rebounded. In early May, Treasury Secretary Scott Bessent told investors at the Milken Institute Conference that "U.S. markets are antifragile." Yet, where some see evidence of resilience in the market's ability to weather the storm, others see a close call that portends future upheaval. "It's a very good reminder that there are a lot of cracks in the system," said Phillip Basil, director of economic growth and financial stability at the consumer advocacy group Better Markets. "We're on a knife's edge, so to speak, with financial stability risks. It won't take that much more to tip us into a problem."JPMorganChase CEO Jamie Dimon expressed a similar view last week during an onstage appearance at the Reagan National Economic Forum in California. He described a major disruption of Treasury market function as an inevitability. "You are going to see a crack in the bond market, OK?" Dimon said. "It is going to happen."Dimon said he has warned regulators about this risk and let them know that he expects they will "panic" when the time comes. His bank on the other hand, will be "fine," he said, adding "we'll probably make more money."Bessent, this week, said Dimon's forecast, while prudent for a risk-sensitive banker, was overly pessimistic for the broader economy."I have known Jamie a long time. And for his entire career, he's made predictions like this," Bessent told CBS News on Sunday. "Fortunately, none of them have come true."Still, Bessent and the Trump administration are poised to oversee several changes aimed at reforming the Treasury market, including the shift to mandatory central clearing — an initiative started by the Securities and Exchange Commission in 2023 but poised to go into effect at the end of this year — and, potentially, a rethinking of the supplemental leverage ratio that would enable primary dealer banks to hold more Treasuries without facing restrictive capital requirements.During the past five years, the amount of outstanding Treasury debt held by the public has increased by nearly 50%, from $19.2 trillion in 2020 to roughly $28.5 trillion today. During the pandemic, much of that debt was absorbed by the Federal Reserve, helping it grow its balance sheet by more than $4.5 trillion in a little more than two years. Some of those Treasuries ended up on bank balance sheets — contributing to the short-lived banking crisis in 2023 — while others were purchased by money market funds. A large portion also found their way into complex investment schemes.Just one week before Trump's so-called Liberation Day announcement, Kashyap and three other economists released a paper exploring the fragilities that have arisen in the Treasury market. They focused on something known as the cash-futures basis trade, in which hedge funds seek to profit off the price difference between cash and Treasury futures through highly leveraged derivatives. While that trade is stable in isolation — because the funds' investments are perfectly hedged — it is vulnerable to rapid unwinds if any of the handful of firms in the space suddenly need to reposition their portfolios, Kashyap said."In early April, it looked like we had such a rapid adjustment that people were going to do prudent risk management and step back; that the volatility was going to result in margin calls on the derivatives involved in the basis trade, which could set off a spiral," he said. "We didn't get there, but that doesn't mean that problem can't arise in the future."According to the minutes from the most recent Federal Open Market Committee meeting, central bank officials were tracking the cash-futures basis trade during the April stress, concluding that it "appeared to remain largely stable." Kashyap said this was likely because the trade had less reliance on long-dated bonds than other similar investment strategies, including one focused on the spread between Treasury yields and interest rate swaps.The Fed minutes note that the unwind of the Treasury-swaps trade "appeared to have been a factor in the deterioration of liquidity and the associated rise in longer-term yields." Had that trade been larger, or had the disruption impacted the securities held by the cash-futures trade, the disruption could have been more severe.Basil, a former financial policy specialist for the Federal Reserve Board, said this dynamic is emblematic of one of the core issues with the Treasury market: that a growing share of securities are held by entities that are prone to sell them at the first sign of stress. "You have a larger proportion of Treasury holders that are more liquidity-seeking, particularly in periods of stress, so it's more likely that holders of Treasury securities will be selling them when there's market turmoil," he said. "At the same time, you have intermediary balance sheets that just haven't kept up, and the stock has grown tremendously."U.S. sovereign debt is also going through something of a sea change. Along with concerns about the country's outlook for economic growth and deficit spending — both of which seem to be causing investors to demand higher returns — there are also more fundamental questions being asked about the country's ability to be a safe haven for capital. Instead of flocking to Treasuries, as they typically do during times of crisis, investors actively moved away from dollar-denominated assets in April. Derek Tang, CEO and co-founder of the Washington-based research firm Monetary Policy Analytics, said the past two months have seen a "very big" repricing of Treasury debt based on various changes to government policy and practice. Tang said short-term volatility is to be expected as investors adjust to new conditions and should not diminish the Treasury market's global standing. But, he added, more significant changes could be on the horizon as the Trump administration weighs trade policies that would disincentivize foreign investment. "These things undermine confidence in Treasury markets and might prompt a longer-term withdrawal," he said. "It might not be fast, but if it happens over time, that is going to increase the interest rates that the United States has to pay on its debt and have knock-on effects on borrowing rates for households and businesses. All these things are interconnected."These new and worsening concerns surrounding Treasuries and their market stability also create potential complications for reforms. Banks have for years argued that Treasuries should be exempt from leverage ratios because they are effectively risk-free — with the backing of the U.S. government, they will always pay out at par value if held to maturity.But, Basil said, recent years have shown that bonds carry other risks, ones that could manifest more frequently as the Treasury market continues to grow. "On one hand, we have the government and certain policymakers saying there's trouble in the Treasury markets and a lot of turmoil. And then, on the other hand, they want to exempt Treasuries from the SLR because they're risk-free. It makes no sense," Basil said. "You can't call it both ways."