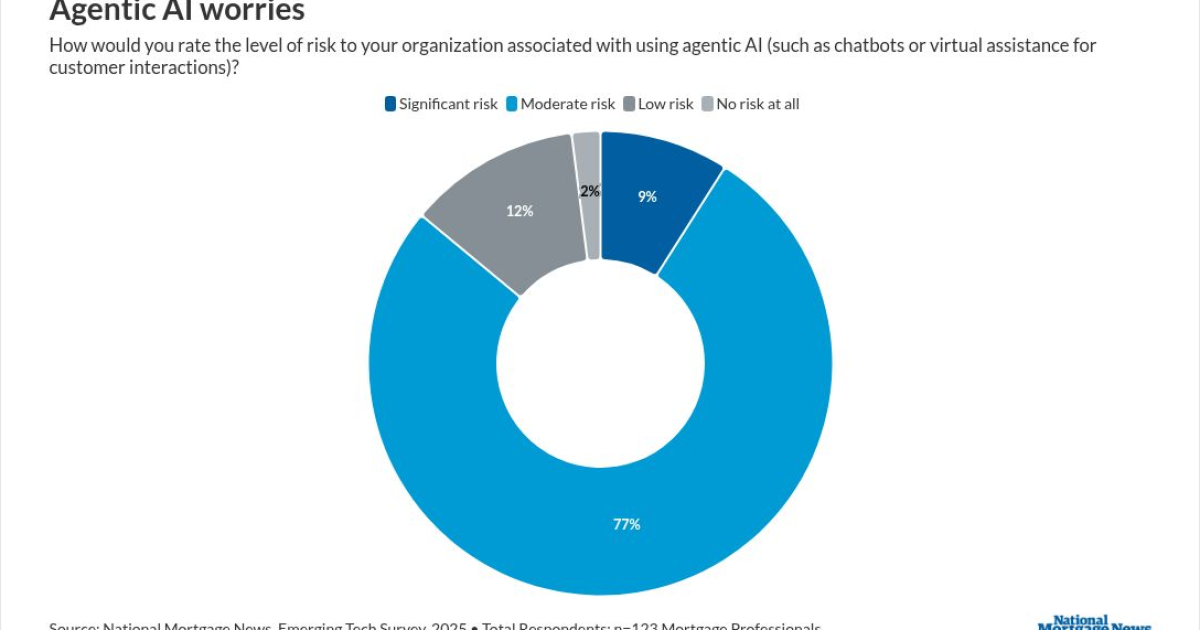

The goal for artificial intelligence in mortgage isn't total automation, but misunderstandings surrounding the purpose of the technology can lead some to believe it is, resulting in a certain level of apprehension and mistrust today. If anything, the technology industry's efforts to market AI, particularly its ability to automate, might be too successful, unintentionally creating apprehensions and misconceptions in highly regulated segments like mortgage over what agentic tools are actually doing, industry leaders suggest.The real and imagined risks that all types of agentic AI could pose for businesses, though — whether associated with regulation, data security or misinformation — are at top of mind for mortgage lenders. In a survey of over 100 lending professionals conducted this summer by Arizent, parent company of National Mortgage News, 86% of the industry cited agentic AI use as an enterprise risk factor. Nine percent went as far as rating it a "significant" risk, with 77% deeming it "moderate."Part of the problem may be that AI is making the work look too easy, according to Diane Yu, CEO of point-of-sale software platform Tidalwave. "A lot of technology companies are trying to sell it that way: 'I will automate everything,'" she explained. While the ability of agentic AI to act and complete tasks autonomously is an important selling point, it's a far cry from making approval or denial decisions — a point even its staunchest advocates in the mortgage industry say is not their goal. Regulators themselves also have not given signals that an AI-produced loan decision would be compliant. "A lot of people don't understand that, though," Yu added, referring to the consumer population. because what AI automation can accomplish is "a good story." More than just ChatGPTMany people today equate artificial intelligence output to ChatGPT production, but agentic AI expands that definition, ranging in form from automated voice service technology to tools that operate in the background reading, extracting and analyzing data and documents.The accelerated improvement of artificial intelligence over the past year means that, despite industry hesitance, many mortgage professionals want to explore the potential benefit it will bring, regardless of their institution type. Large banks and credit unions are already actively looking for ways to apply it effectively in mortgage operations, according to John Geertsema, managing partner at business and technology consulting firm Capco. "They're asking, 'Where is it safe to use? Where will regulators be comfortable with us using it? And what can we automate without creating a risk for, say, a repurchase?'" Geertsema said. "A lot of what we were talking about was large language models for the last couple years. The difference now is that with agentic AI, it goes beyond just being conversational and now the agents are actually executing multistep tasks," he added. Ensuring humans are in the loopWhile its aptitude at accomplishing tasks and analysis in a fraction of the time it might take a live employee to do them, agentic AI won't be able to provide optimal results by itself, experts warned, emphasizing long-standing industry sentiment that humans will remain vital to its expansion. They raised caution about the perils of handing too much responsibility to agentic AI programs and its potential to harm business, particularly if human oversight is discarded.In an analysis of the performance of end-to-end agentic AI workflows conducted by attorneys at Debevoise & Plimpton, they determined the technology was effective when automating aspects of a complex project but struggled to maintain that level consistently across a project. "Many of these AAW projects fail because, as various tasks are stitched together without any human review in between them, the risk of errors compound, and any time saved in the process is lost by needing human intervention to fix the end product," the attorneys wrote in the law firm's data blog. The benefits agentic AI offers is only as good as the data it has available to analyze, meaning important variables may be left out when it considers all possible outcomes. "The rules that we set up for agentic AI systems usually cannot capture the nuanced social and cultural contexts that experienced employees rely on when deciding that not following a policy is actually the right course of action because the policy was drafted without this particular situation in mind," the blog stated. In the case of mortgage, any incomplete or outdated source data could result in a customer being deemed ineligible for certain loans simply because incorrect guidelines were applied. While the AI may technically still be operating within the rules, the use of faulty data in such cases brings the same type of outcome a denial would — lost business. The findings add credence to technology experts' emphasis to keep humans in the process, not just to review exceptional findings, but also override AI when necessary. "You want a human in the loop on a lot of these decisions that are occurring," Geertsema said. Achieving the right balance means finding the right formula "to make things more efficient and more accurate, but still keeping that human touch and reasoning in there." Agentic AI's scrutinization of source data and the speed at which it can to spell out its findings after completed tasks are helping to provide lenders some peace of mind, Yu said. Understanding how autonomous determinations were made, including any flaws AI may have uncovered, and seeing suggestions for future action items goes a long way in helping them get to the lightbulb moment. "Loan officers, processors, underwriters — they don't have to chase down all those data points.They don't have to run calculations. They can see them in the review," Yu said.As a result, "they can make a long decision much faster, and I think that's the key here. They are making the loan decision," she said.