Mortgage critical defect rates improve, but issues remain

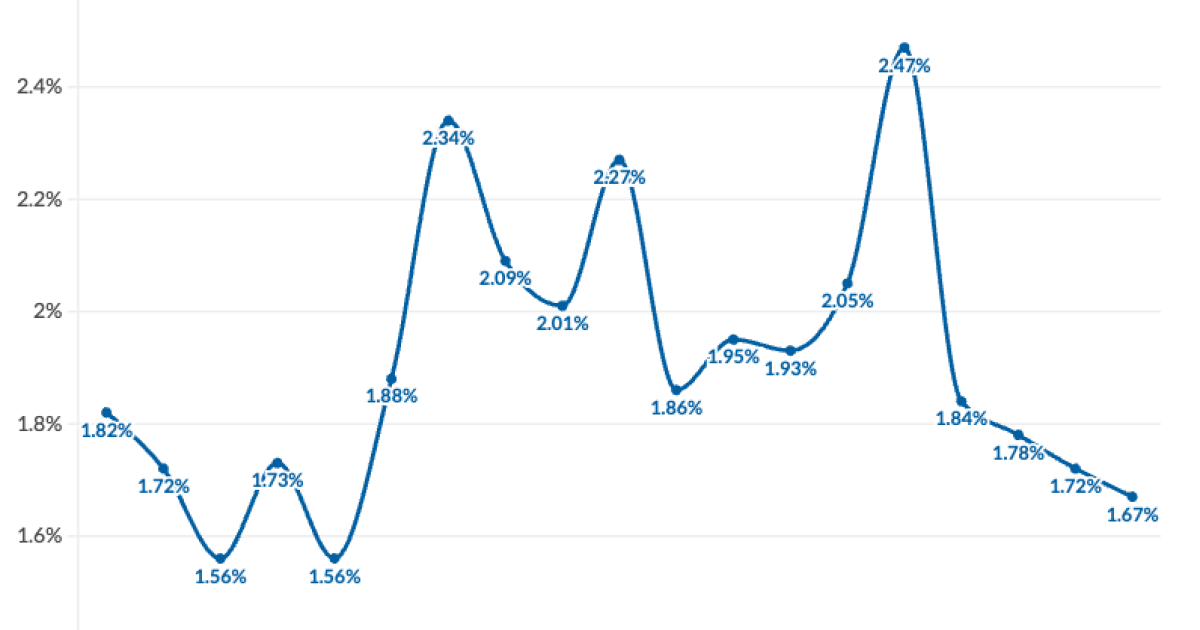

unitedbrokersinc_m7cmpd2024-04-04T22:16:48+00:00Mortgage production defect rates in the third quarter of 2023 showed continued improvement, even as origination volume was hard to come by, the latest Aces Quality Management report found.The company's post-closing review process categorizes file errors using the Fannie Mae defect taxonomy. Defects are indicators of, but not necessarily proof of, fraud.In the third quarter, the defect rate of 1.67% was 5 basis points better than 1.72% in the second quarter and a high point of 2.47% in the third quarter of 2022.That is the lowest rate since the first quarter of 2020's 1.56%, at the very end of which, restrictions related to the Covid-19 pandemic affected all parts of American life.Lenders have gotten a better handle on quality in their loan creation processes following that spike one year ago, said Nick Volpe, Aces executive vice president, in a press release. The decline in origination volume may have worked in some manner to the advantage of originators."While fewer loans may afford lenders the opportunity to intensify their focus on quality, it's clear that maintaining high standards amidst market fluctuations remains paramount," Volpe said. "The persistence of this trend underscores the industry's adaptability and dedication to ensuring the integrity of lending practices."Issues around income and employment remain the most common defect found, at a 23.4% rate, an improvement from the second quarter's 31.25%.Income documentation problems fell to a 27% share of the category, from 47% for the prior period. But income calculation issues had a 55% share."Amidst the backdrop of fighting for every loan, one would expect the calculation subcategory to make up the majority of defects in the income/employment category – with many harder-to-qualify borrowers going through the process," the Aces report said.The company saw increases in defects related to loan documentation as well as borrower and mortgage eligibility issues.Normally, loan documentation can swing wider than other categories going between quarters. But, Aces said this quarter's shift was more pronounced, up nearly 7 percentage points to 19.15% from 12.5%.It blamed the increase on closing documentation deficiencies, followed by upfront document collection in the application processing subcategory."These types of defects are often attributed to sloppiness in the manufacturing process," Aces said.General eligibility accounted for 52% of the borrower and mortgage eligibility defects. Typically, it means cash-out refinance requirements are not being met, the property listed for sale being used to secure a refinance, an excessive debt-to-income ratio and deficiencies in general requirements for various other loan types."As more and more loans that are harder to qualify enter a lender's pipeline, it is imperative that underwriting account for nuances associated with a borrower's specific situation and chosen loan type," Aces said.The liabilities category defect rate also increased from quarter-to-quarter, to 11.35% from 8.33%. While not as prevalent, appraisal-related defect rates grew to 4.26% from 3.47%.Although Federal Housing Administration-insured mortgages made up 24.11% of the file reviews, the defect rate was 42.61%.At the other end of the spectrum, conventional loans were 59.55% of reviews but 48.7% of files with defects. Veterans Affairs-guaranteed loans were 14.22% of the quality checks but just 6.96% of the errors."Last year, the lenders that thrived were those who embraced quality control and proactively prepared for the evolving market landscape," said Trevor Gauthier, CEO at Aces. "We eagerly anticipate witnessing lenders maintain their steadfast commitment to prioritizing quality as they navigate future market dynamics."