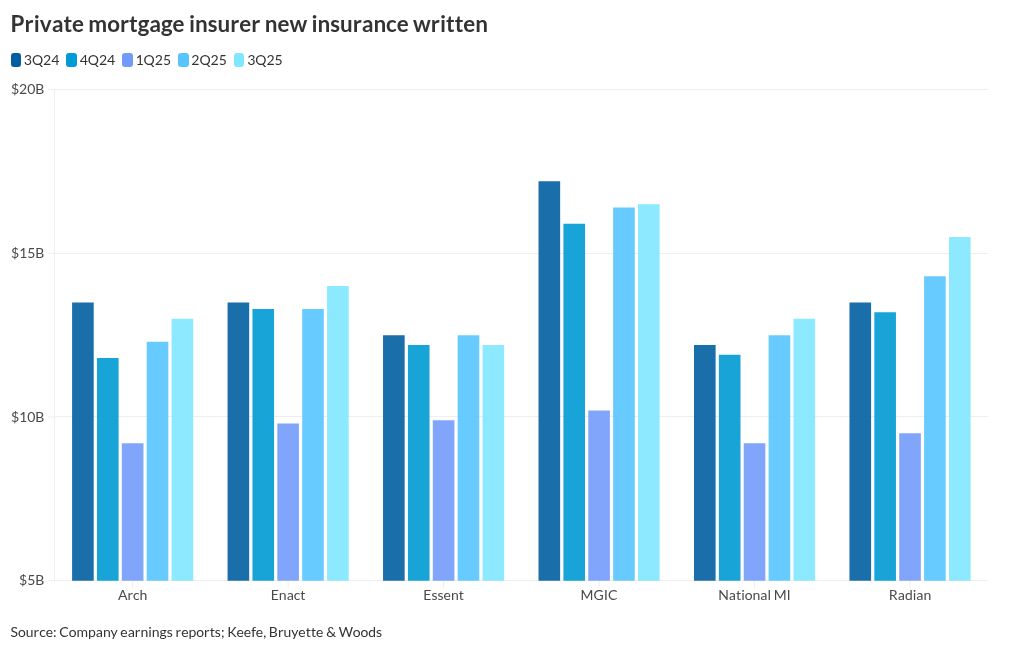

New insurance written at the nation's six active private mortgage insurers continued to run ahead of last year's pace during the third quarter, with the market share gap widening between the top and bottom.For the quarter, the MIs wrote $84.3 billion of new policies, compared with $81.2 billion three months prior and $82.5 billion one year ago, according to data compiled by Keefe, Bruyette & Woods.It is the second consecutive quarter of 2% annual growth, following a 1% contraction in the first three months of the year.Radian, whose parent company announced both an acquisition and a shedding of its non-MI product lines, had the largest annual growth, writing 15% more NIW."Mortgage insurers remain inexpensive and Radian should have the highest [return on equity] in the group after the Inigo acquisition," Bose George, an analyst with KBW, said in the investment thesis section in his report on Radian's results. But even with a 1.2% year-over-year decline in NIW and a 4% drop in market share, MGIC remained the most prolific private MI; but the gap between it and Radian narrowed to 1.2 percentage points from 2.6 percentage points in the second quarter.The following is a roundup of the six publicly traded active private MI underwriters' third quarter results:MGIC's insurance-in-force tops $300BNet income at MGIC Investment remained strong but lower versus the comparative periods.It reported net income of $191.1 million for the third quarter, compared to $192.5 million for the three months prior and $200 million one year ago.NIW of $16.5 billion was higher than the second quarter's $16.4 billion but 4% lower on a year-over-year basis from $17.4 billion. Even so, this beat KBW's $14.7 billion estimate.But, a major milestone at the first of the modern private mortgage insurers, Mortgage Guaranty Insurance Corp., was reached at period end, with insurance-in-force of over $300 billion, said Tim Mattke, CEO, during the earnings call. This compared with $297 billion on June 30."This milestone reflects our historical and ongoing leadership in the market," Mattke added. "This achievement also reflects the dedication and excellence of our talented team, their integrity, adaptability and focus sets us apart from others and propels our success."KBW's George was a bit pessimistic about the IIF numbers although he did increase his full year new insurance written predictions through 2027."However, the IIF impact is largely being offset by faster cancellations and did not change meaningfully," George said in his commentary on the company. The analyst models IIF growth of 2.1% for this year and 1.1% in each of the next two, which compares with 0.6% for 2024.Radian gains ground in market shareSince all of the private MIs adopted the black box form of risk-based pricing, quarterly market share had been volatile.But in the third quarter, Radian had the largest business growth. Besides 15% year-over-year growth in NIW, it gained 8% quarter-to-quarter, the KBW data said.During the quarter, it announced the proposed acquisition of Inigo, a specialty insurer in the Lloyds marketplace, and the divestiture of its conduit, title insurance and real estate services units.Inigo should close in the first quarter of next year, management said on the earnings call.Radian's sales process "is well underway, and has attracted interest from numerous potential buyers for each of the three businesses," said Rick Thornberry, CEO.Similar to MGIC, it reported a slight decrease in net income from the second quarter, to $141 million from $142 million, and a larger year-over-year drop from $152 million.But its NIW grew to $15.5 billion from $14.3 billion and $13.5 billion in the respective comparative periods. Refinancings made up 5% of the NIW, unchanged from the second quarter."Radian's transformation from a leading U.S. mortgage insurer into a global multiline specialty insurer is expected to increase our addressable market for continuing operations by a factor of 12, providing flexibility to deploy capital across multiple insurance lines through various business cycles," Thornberry said.The discontinued businesses lost $11 million for the quarter, inclusive of $7 million of estimated costs for their future sale. This compared with a year ago loss of $15 million; those figures are net of taxes.Enact increases dollar volume, but lower net incomeEnact tied for the second largest quarter-to-quarter gain in NIW share. When compared with one year ago, it joined Radian and National MI as the only firms which were able to increase the dollar volume of new activity.It had a bigger quarter-to-quarter drop in net income than its two larger competitors to $163 million versus $168 million in the second quarter. For the third quarter last year, it earned $181 million.For the third quarter, it had NIW of $14 billion, up from $13.3 billion three months prior and $13.6 billion one year prior.Overall, our business remains underpinned by strong demographic tailwinds, particularly from prospective first-time homebuyers entering the market," Rohit Gupta, president and CEO said during the earnings call. "We remain optimistic about the long-term health of the U.S. housing market and confident in our ability to deliver through economic cycles."When asked about artificial intelligence transforming the MI business, Gupta responded "I've said in the past that we continue to invest on that front both for efficiency reasons and making smarter and more granular decisions. So that's basically how we see that playing out for our business."Arch on pace for $1B in underwriting incomeArch Capital Group's mortgage insurance group remains on pace to deliver $1 billion in underwriting income for 2025. It did $260 million in the current quarter, compared with $238 million last quarter and $269 million one year ago.The improvement from last quarter was primarily due to a lower level of ceded premiums as a result of the tender offers we executed in the second quarter for two Bellemeade Re securities," explained Francois Morin, chief financial officer, during the earnings call. "There was also a slight benefit due to a higher level of cancellations on CRT transactions."Net premiums written by the mortgage insurance segment, which also includes international and reinsurance activities, was down 2.8% from the third quarter 2024."We are well positioned to support first-time home buyers when the U.S. housing market eventually expands," said Nicolas Papadopoulo, Arch CEO, on the call. "The broader mortgage insurance market remains healthy with disciplined underwriting and stable pricing."Arch, which has other insurance lines, had net income of $1.3 billion in the third quarter, versus $1 billion last year.NIW of $13 billion compares with $12.3 billion in the second quarter and $13.5 billion one year prior.NMI CEO says potential MI entrant not neededDuring NMI Holdings' third quarter earnings call, the management team was asked about a potential new entrant to the mortgage insurance business.Adam Pollitzer, president and CEO, said the company is aware of this development. According to a LinkedIn post from the Mortgage Scoop, the company is Anza Mortgage Insurance; the company has several experienced executives listed on its website as part of its efforts including Chris Gamaitoni as CEO, a former managing director at Tilden Park Capital Management and Compass Point Research and Trading.No clear need for another competitor exists in the market today, said Pollitzer. Moreover, he pointed to National MI's experience as a de novo entrant."We, perhaps more than anybody else, know the challenges and difficulties that come with building a private MI business, it is not easy at all, right?" he said. "It is hard to raise the capital needed, it's really hard to create an operating platform for the MI business."It's really hard to hire the right team to sign up customers, earn their trust and also manage through an extended J curve to get to a point of profitability," Pollitzer said.NMI Holdings had its first profitable quarter in 2016. National MI started underwriting policies in April 2013.While not knowing what will happen, it added "it's a very high bar," which requires a large amount of capital just to comply with the Primary Mortgage Insurer Eligibility Requirements.While National MI is still the smallest company in terms of IIF, it ended the quarter on par with Arch when it came to new insurance written. It has IIF of $218.4 billion as of Sept. 30; Essent, the other de novo formed after the Great Financial Crisis forced three companies into run-off, was the next smallest at $247 billion.NMI Holdings earned $96 million for the third quarter, flat with the second quarter's $96.2 million and up from $92.8 million one year ago.Its $13 billion of NIW was up from $12.5 billion in the second quarter and $12.2 billion for the third quarter of 2024.Essent NIW, market share both declineOf the six active companies, Essent was the only one which wrote less new business compared with the previous quarter and year. It did $12.2 billion of NIW in the third quarter, compared with $12.5 billion in both comparable periods.Essent's market share fell to 14.5%, down by 0.9% on an annual basis and by 0.6% from the prior year.Net income was $164.2 million, down from $195.4 million in the second quarter and $176.2 million one year ago."We remain committed to a prudent and conservative capital strategy that allows us to maintain a strong balance sheet to navigate market volatility while preserving the flexibility to invest in strategic growth," Chairman, CEO and President Mark Casale said during the earnings call. "Thanks to our robust capital position and strength in earnings, we are well positioned to actively return capital to shareholders in a value-accretive fashion," he added. Essent's title insurance business "has performed pretty much in line with what we thought, if we would have thought rates would be this high, to try to be honest with you," Casale said in response to a question."I think if rates go lower, we're very levered to rates given the lender focus of the business."It is growing primarily in Texas and Florida "and a bit of the Southeast," he said. Essent is still building out the business "and we're fine with that."If it gets big enough, title insurance will pop up as its own reporting segment but "if it stays small, it says small, and that could happen."