VA foreclosures surge to 5-year high

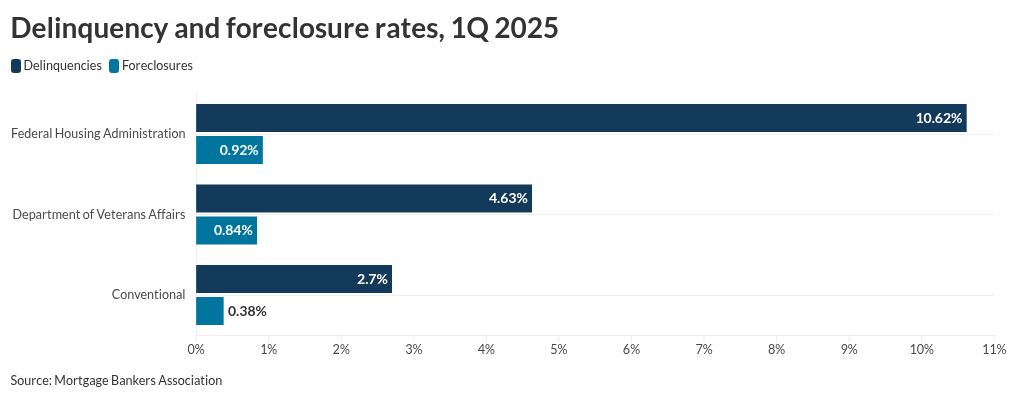

unitedbrokersinc_m7cmpd2025-05-13T19:22:30+00:00The expiration of the Department of Veterans Affairs loss-mitigation program drove an overall rise in foreclosures to start 2025, with the jump among VA loans the highest in decades, according to the Mortgage Bankers Association. The share of mortgages in foreclosure relative to total volume increased to 0.49% in the first quarter, up 4 basis points from 0.45% three months earlier. The latest percentage is also up 3 basis points from 0.46% year over year, MBA said in its latest national delinquency survey.At the same time, new foreclosure starts climbed up to 0.2% from 0.15% during the fourth quarter of 2024. "Foreclosure inventories increased across all three loan types, and particularly for VA loans," said Marina Walsh, the trade group's vice president of industry analysis, in a press release. "The percentage of VA loans in the foreclosure process rose to 0.84%, the highest level since the fourth quarter of 2019. The increase from the previous quarter marks the largest quarterly change recorded for the VA foreclosure inventory rate since the inception of MBA's survey in 1979," she added.Numbers among VA borrowers took a turn upward to start the year following the expiration of a voluntary foreclosure moratorium tied to the Veterans Affairs Servicing Purchase program. Initial data at the start of the year in several reports showed a noticeable spike in foreclosure starts as well as auctions. Against that backdrop, MBA and other mortgage industry groups are sounding the alarm about the need to introduce new relief for distressed veteran homeowners, with VASP no longer available for new applicants as of May 1. Successor VA loss-mitigation measures have yet to be enacted, but a new partial-claim proposal is currently making its way through Congress.While the rise was more muted elsewhere, the share of Federal Housing Administration-guaranteed loans in foreclosure also climbed upward to 0.92% during the quarter. Forborne conventional mortgages made of 0.38% of the outstanding volume. Why this report paints a mixed pictureAlthough trends show reasons for concern, Walsh pointed out that current delinquency and foreclosure rates both sit under historical averages, with first-quarter numbers offering a mixed picture of borrowers' standing.The total delinquency rate increased for the second quarter in a row to 4.04% and was also up year over year, driven by conventional mortgage activity. The share rose from 3.98% three months earlier and 3.94% a year ago. Numbers were adjusted for seasonality. The delinquency rate, however, does not include loans that rolled over into foreclosure. Compared to the previous quarter, the delinquent share among conventional loans backed by Fannie Mae and Freddie Mac increased 8 basis points to 2.7% from 2.62%. The FHA segment saw a 41 basis point drop to 10.62% from 11.03%, while delinquency share among VA loans slid 7 basis points to 4.63% from 4.7%.Current delinquency rates are 8 basis points higher for conventional mortgages on an annual basis. Among government-backed loans, the FHA share increased 23 basis points year over year, with the percentage falling 3 basis points for VA loans.By delinquency stage, the portion of loans 30-days past due rose a seasonally adjusted 11 basis points to 2.14% from the previous quarter. The share shrank to 0.73% for payments 60 days late, down 3 basis points. The 90-day delinquency rate similarly fell 2 basis points to 1.17%.Is the uptick in mortgage delinquencies the start of a trend?MBA's findings largely align to data regarding seriously distressed loans and foreclosures noted by the Federal Reserve Bank of New York in its first quarter report. New foreclosure filings leaped by almost 50% on a quarterly basis to approximately 61,660 from 41,220 in the fourth quarter, according to New York Fed's calculations.The number of mortgages flowing into the seriously delinquent stage of 90 days or more past due similarly accelerated 13 basis points to 1.22% from 1.09% of total loans outstanding in the prior quarter. On a year-over-year basis, the share rose from 0.92%.Meanwhile, the new seriously delinquent rate of home equity lines of credit accelerated to 0.88% from 0.56% three months earlier and 0.52% in the first quarter 2024.Delinquency upticks in recent months might serve as a flashing caution light for servicers in the months ahead if trends hold. While VA policy changes played a significant role in the foreclosure spike to start the year, New York Fed noted warning signs appearing across the board, with the latest activity catching up to quarterly delinquency growth rates . "It looks like it's a pattern of increasing delinquency leading to increasing foreclosure across all types of mortgages," researchers at the New York Fed said.